中文

中文

Independent wealth management firms are gaining share in a market that is expanding despite already high adoption of advisor-led relationships. Wealth is concentrated in households that value ongoing advice, and assets are likely to change hands through inheritance and channel migration. That combination favors firms that can serve clients at scale and retain them through transition.

In this article, we make the case for sustained growth in the wealth management market as a whole and the expansion of independent wealth management within that market.

Wealth Management Remains an Attractive Market

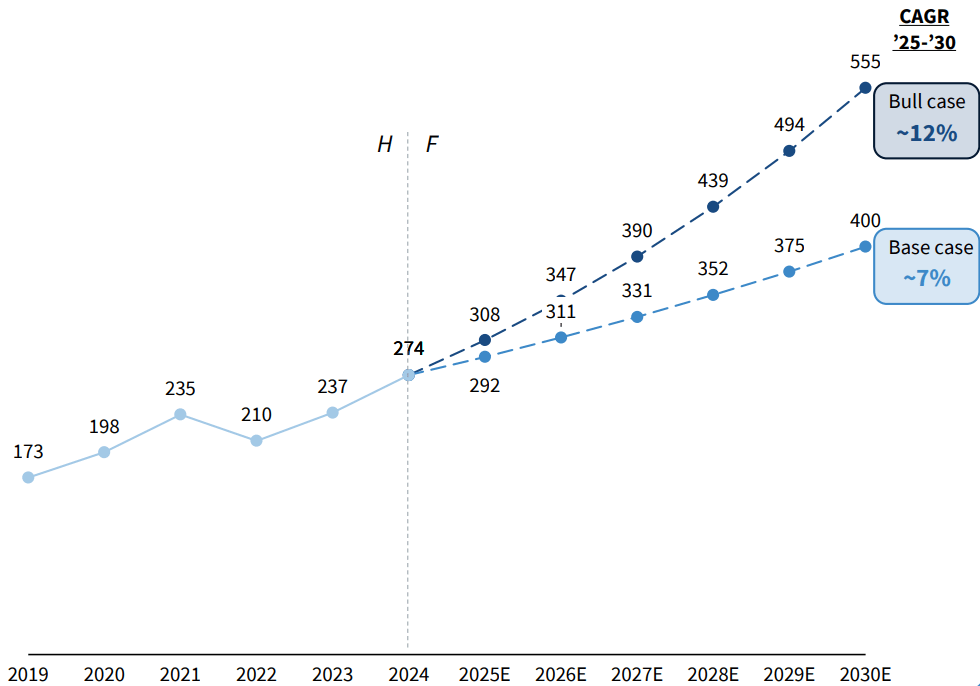

The U.S. wealth management industry generates roughly $274 billion in annual revenue and could grow at a 7% to 12% compound annual growth rate (CAGR) over the medium term. That range is plausible if several drivers hold at once: asset appreciation remains positive, advice penetration rises, affluent households continue to accumulate investable assets, and successful transitions as advisors retire. Figure 1 highlights the historical and expected revenue growth of the total U.S. wealth management industry.

U.S. Wealth Management Industry Revenue, ($B), 2019-2030E

Asset Appreciation

Because so much revenue is tied to asset values, nominal market returns still do more to expand the revenue base than any productivity tool or client-acquisition tactic. A balanced mix of equities and fixed income can, over time, support meaningful growth in managed balances.

“Assets often move when families do, and advisor relationships are vulnerable when wealth changes hands (roughly 70% of beneficiaries change advisors after an inheritance event).”

Assets in Motion

The U.S. is entering a period of intergenerational wealth transfer often estimated at $80 trillion to $100 trillion over the next two decades, with a substantial share expected in the next ten years. Gen X alone is projected in some analyses to receive roughly $1.4 trillion per year over the coming decade.

As ownership changes, advisory relevance likely will change with it. Assets often move when families do, and advisor relationships are vulnerable when wealth changes hands (roughly 70% of beneficiaries change advisors after an inheritance event).

Advisor Retirements

Estimates suggest 35% to 40% of advisors may retire over the next decade, representing more than 40% of industry assets by some measures. Some forecasts also point to an advisor shortfall of roughly 100,000 by 2034.

Retirements create retention risk, as advisor transitions typically result in ~10–20%+ asset attrition, depending on channel and transition structure. Firms with strong onboarding, modern tech stacks, and scalable operation models are best positioned to capture and retain assets through those disruptions.

The Revenue Pool Is Increasingly Concentrated in Affluent Households

Households with more than $1 million in investable assets account for roughly 66% of the revenue pool. High-net-worth (HNW) and ultra-high-net-worth (UHNW) investors are also said to represent about 57% of assets in the advisor-driven channel, up from roughly 33% in 2013.

There are two major implications. First, industry revenue can grow faster than the number of advised households because wealth is compounding faster among the most affluent investors. Second, firms positioned to serve complexity should have a structural advantage over firms built primarily for accumulation-stage clients. That advantage does not automatically accrue to independents since banks and wirehouses remain strong in this segment. But it does reward firms with planning depth, broad product access, and the ability to retain multi-generational relationships.

This is why headline fee pressure can be misleading. Affluent clients often pay lower stated basis-point rates, but they remain economically attractive because they bring larger balances, deeper planning needs, more cross-sell opportunities, and, in many cases, stronger retention. For many firms, the central economic challenge is winning and keeping affluent households at scale.

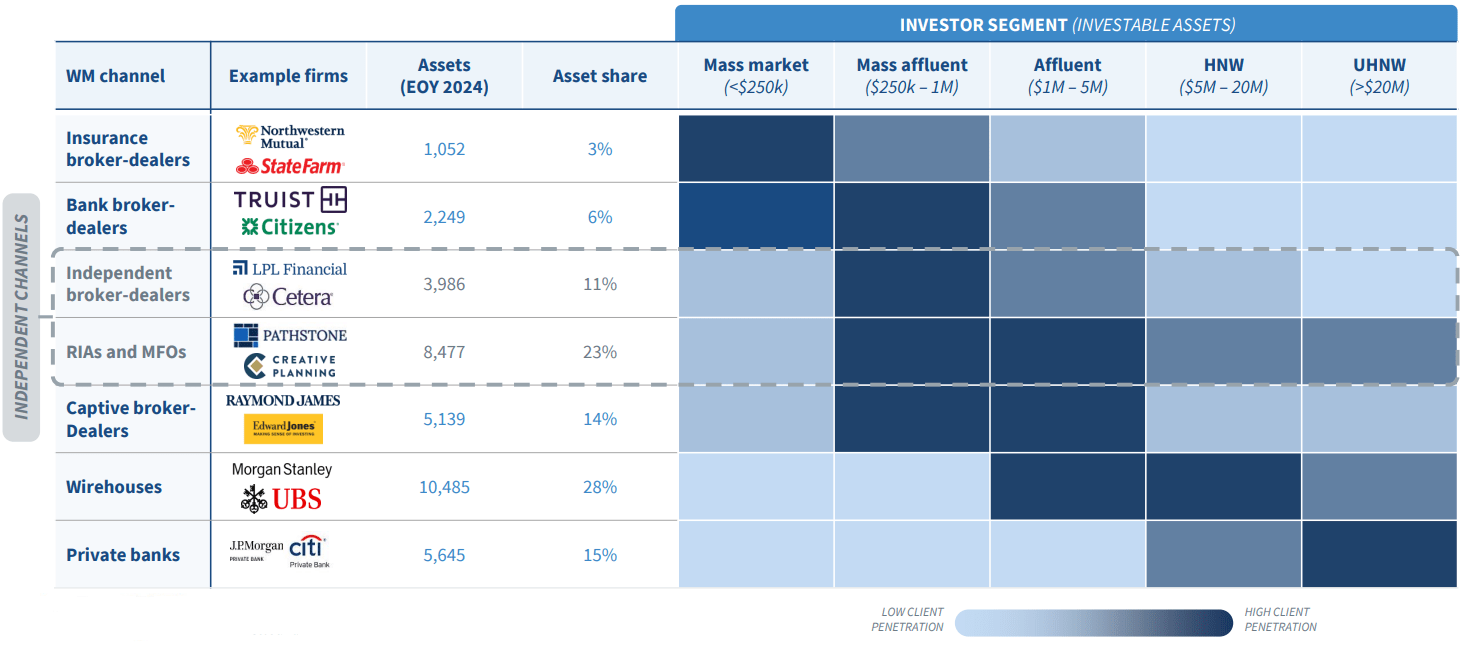

Existing clients also continue to add assets beyond market appreciation. Contributions from earned income, business distributions, retirement-plan rollovers, liquidity events, inheritances, and real-estate sales all expand managed balances. Firms with strong planning capabilities are best positioned to capture those flows. Figure 2 identifies the breakdown of assets between wealth management channels.

Independent Wealth Management Firms Are Gaining Ground

Independent firms, which are financial advisory businesses that operate outside of large wirehouses or bank-owned platforms, already control a meaningful portion of industry assets. Registered investment advisors (RIAs) and independent broker-dealers (IBDs) manage roughly 34% of industry assets. That presence is especially notable in the mass affluent and affluent markets: households with roughly $250,000 to $5 million in investable assets.

That segment in the market matters because it combines recurring advisory economics with genuine planning complexity. These households are more likely to need help with retirement income, tax planning, business liquidity, estate decisions, and intergenerational transfer than a purely mass-market client base, yet they remain far less centralized than the ultra-high-net-worth market.

“RIAs and IBDs manage roughly 34% of industry assets. That presence is especially notable in the mass affluent and affluent markets.”

Plus, many independent firms are built around advisor ownership, flexible service models, and modular technology stacks. Those characteristics matter more as clients grow less willing to accept product manufacturing and custody as a single bundled proposition.

Captive channels where advisors operate under a parent firm with limited independence like wirehouses and broker-dealers still control large parts of the market and will remain formidable competitors, particularly at the very top end. But the center of growth appears to be shifting toward independent firms.

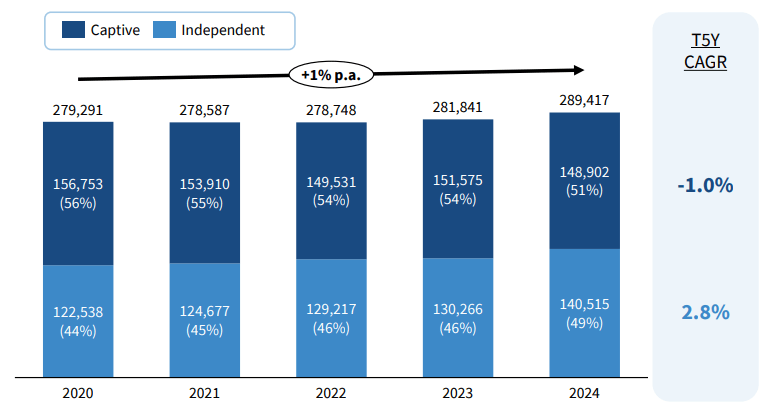

Independent Channels Have Grown at the Expense of Captive Channels

Advisor headcount overall has grown slowly at about 1% CAGR since 2020, but advisor distribution has continued to shift toward independence. Figure 3 identifies the shift toward independent advisors as a portion of the total financial advisor headcount.

Financial Advisor Headcount, by Captive/Independent channel, 2024

Advisors leaving wirehouses and traditional broker-dealers for RIAs and IBDs often want higher payout economics, fewer platform constraints, more control over staffing and branding, and a model less tied to product distribution. The appeal of fee-based or fee-only advice is economic and reputational.

Clients, meanwhile, are more accustomed to unbundled financial services than they were a decade ago. They are more open to separating custody, advice, lending, and planning, and technology has made that separation easier to implement. Leaving a large platform is still operationally difficult and organic growth remains a challenge, but the infrastructure required to go independent is far easier to assemble than it once was.

Transition and platform firms have helped reduce that friction, alongside a broader WealthTech ecosystem that now supports portfolio accounting, customer relationship management, reporting, onboarding, alternatives administration, and outsourced compliance.

Private Capital Has Made the Independent Channel More Formidable

Private capital has accelerated the institutionalization of the independent RIA market. Private equity firms and strategic consolidators now provide acquisition funding and operating infrastructure at a scale that would have been difficult to imagine a decade ago.

Seventy-two percent of the top 50 RIAs are private-equity-backed, and 2024 saw a 47% year-over-year increase in private equity deals in the space. Capital is now actively expanding the channel.

That capital is being deployed in predictable ways. It funds acquisitions in a still-fragmented market, supports recruiting and team lift-outs, and finances investments in data architecture, workflow automation, compliance, and centralized planning resources. Those upgrades do not guarantee better advice, but they can create the operating leverage and continuity that matter when assets are moving and client expectations are rising.

Who Will Win in the Independent Wealth Management Market?

Over the next decade, the firms most likely to take share in the wealth management market will not simply be the ones with more advisors or more acquisition capital. Instead, the winners will be the ones who can achieve both size and scale, improving outcomes for owners, management teams, financial advisors, their staff, and their clients.

Many firms are getting bigger. Fewer are building the businesses required to fully capitalize on that growth. That distinction between size and true scale will define the next phase of competition in the independent market.

In the next piece of “The Future of Wealth Management,” we’ll explore what it takes to bridge that gap and why so many firms fall short.