Deutsch

Deutsch

The U.S. IPO market regained footing in 2025, ending an extended period of sluggishness in the market with a controlled but meaningful recovery. Last year’s IPO surge reflected pent-up supply and growing investor confidence in public markets, driven by easing inflation and improving macro visibility. While global risks and policy uncertainties remain, the foundation for sustained IPO activity appears more durable than at any point since 2021.

This article discusses how the U.S. public markets performed in 2025 compared with prior periods and the trends that may shape the capital markets through the next year and beyond.

IPOs by Volume and Value

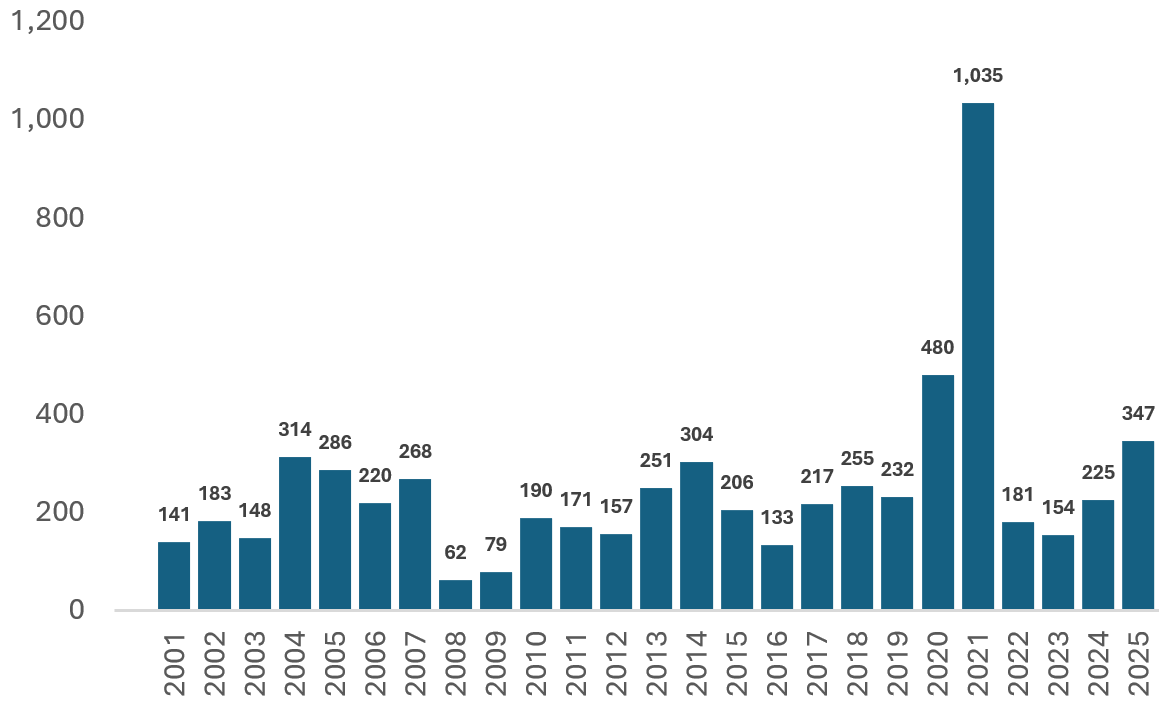

The U.S. IPO market delivered robust growth in 2025, with both issuance volume and capital raised rising despite policy and macroeconomic uncertainty, including the late-year U.S. government shutdown. There were 347 IPOs in the U.S. public markets in 2025, representing a 54% increase from the 225 IPOs completed in 2024. Issuance activity peaked mid-year, with July emerging as the most active month with 37 IPOs, while November saw the lowest activity with just 17 IPOs, reflecting the dampening effects of the government shutdown and year-end market caution. The year marked the second consecutive year of growth following the dip of 154 IPOs in 2023, when issuance declined amid elevated interest rates and subdued risk appetite.

Collectively, 2025 IPOs raised $66.8 billion in gross proceeds, up 153% year-on-year. Average offering size reached $198.7 million, exceeding the prior year’s average of $126.7 million, underscoring a shift toward larger, more established issuers coming to market.

Figure 1: No. of U.S. IPOs Since 2001

Source: Stock Analysis. 2026 data is as of February 2

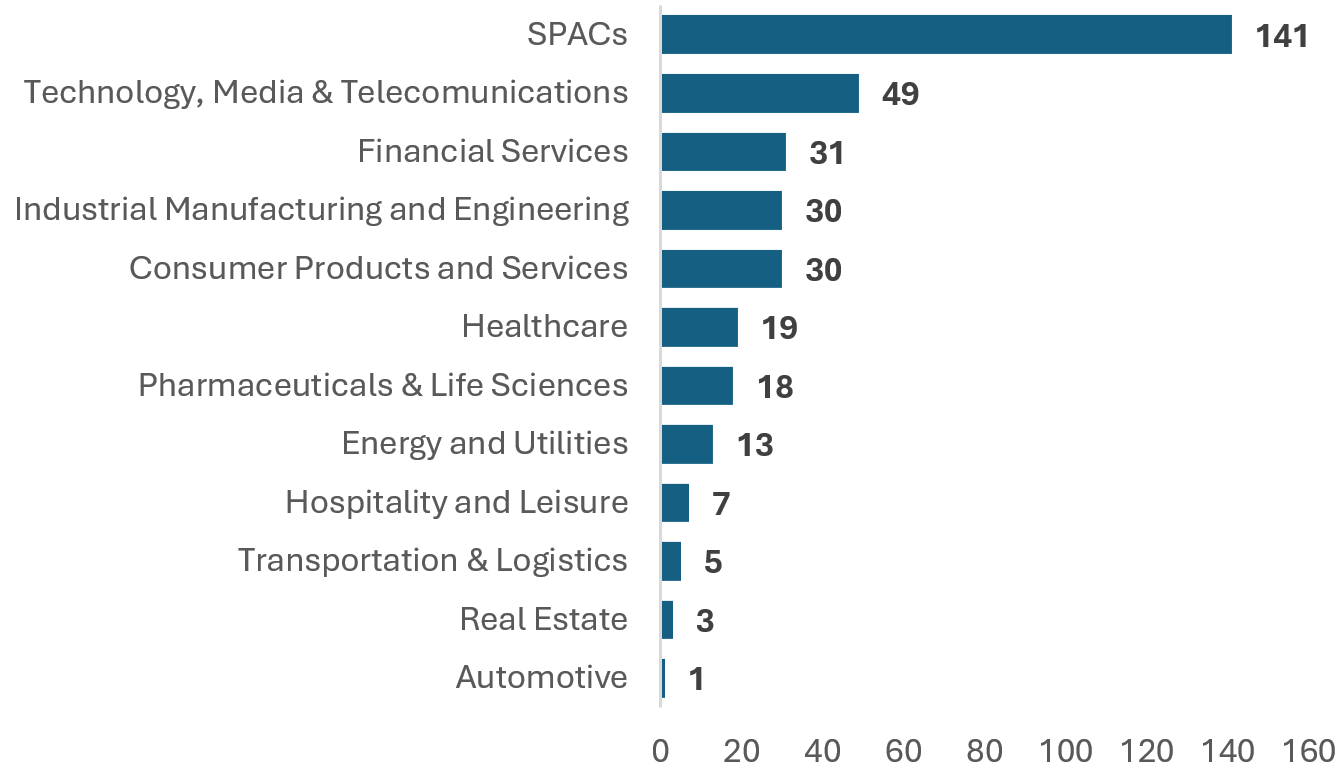

IPOs by Industry

The table below shows the IPOs in 2025 by industry.

Figure 2: No. of IPOs by Industry Classification

Source: Stock Analysis

SPACs

SPACs accounted for around 41% of all IPOs, up from 26% in 2024. By volume, 2025 ranked as the third most active year for SPAC listings with 141 listings since 2016, trailing only the boom years of 2020 (248 SPACs) and 2021 (613 SPACs), per SPAC Research.

This resurgence was different from prior cycles. Experienced sponsors with established track records drove issuance in 2025, rather than first-time sponsors and broad-based enthusiasm. Data from SPAC Insider shows that nearly 80% of SPAC IPOs in the first half of 2025 were launched by serial sponsors, reflecting a market increasingly dominated by institutional players.1 Although the sponsor base broadened toward year-end with new entrants, serial sponsors still accounted for more than 60% of new SPACs, reinforcing the more professionalized nature of the current SPAC landscape.

At the same time, SPAC issuance in 2025 became more thematically focused. Sponsors increasingly targeted sectors aligned with long-term structural trends, including AI, fintech, clean energy, infrastructure, space technology, and select areas of biotech.

Technology, Media, & Telecommunications (TMT)

TMT companies accounted for 14% of the total IPOs in the U.S. in 2025, in line with the activity seen in 2024. Software and IT services companies accounted for a major chunk of the total issuances, accounting for 32 of 49 total TMT IPOs. Public-market conditions were broadly supportive for technology companies with the “Magnificent Seven” technology stocks rising nearly 27% during 2025, improving sentiment toward technology IPOs, particularly those positioned as core infrastructure providers within the AI and data ecosystem.

Looking ahead to 2026, capital-markets sentiment toward TMT remains cautiously optimistic. AI infrastructure and software are likely to lead issuance, supported by continued investment in semiconductors, data centers, and AI-enabled enterprise platforms. This optimism is also reinforced by a sizable backlog of venture-backed technology companies that have remained private for a relatively long time. Several high-profile names including Anthropic, Databricks, SpaceX, and Canva are frequently cited as potential IPO candidates, underscoring the depth of the pipeline should market conditions remain constructive.

Financial Services

The financial services sector saw 31 IPOs in 2025, raising a combined $7.5 billion and accounting for nearly 9% of total U.S. IPO activity. Issuance was spread across multiple subsectors. Capital markets and consulting firms each recorded eight IPOs, reflecting steady demand for advisory and market infrastructure platforms. With six IPOs, insurance sector had its best year since 2005, benefiting from relative insulation from direct tariff exposure and the appeal of more stable earnings, cash flows.2

The broader financial services sector realized a robust index growth of nearly 17%, driven by regulatory clarity, resilient business performance, and optimism around a steeper yield curve as rate cuts take effect.3 Looking ahead, U.S. financial services IPOs appear positioned for selective, quality-driven growth. Potential release of pent-up supply from private equity-backed portfolios is further expected to support IPO activity.

Industrial, Manufacturing, & Engineering (IME)

IME companies saw 30 listings in 2025, representing roughly 9% of total IPO activity. Engineering and construction companies dominated with nine listings, followed by Aerospace and Defense companies, reflecting sustained demand for infrastructure and security-linked assets. Despite persistent challenges, including labor availability constraints, supply-chain volatility, and elevated input costs, investor sentiment toward IME issuers remained constructive where visibility was strong. Growth in AI data center construction and energy infrastructure emerged as a key offset, supporting demand across construction services, electrical systems, and precision manufacturing.

Consumer Products & Services (CPS)

CPS sector had a slow first half but picked up in the second half, reaching a total of 30 IPOs in 2025. That said, the sector has its own challenges, with companies navigating significant demographic, political, environmental, technological, and cultural shifts.

In 2025, CPS issuers spanned a wide range of subsectors, including packaged foods, beverages, education services, travel, specialty retail, household products, and consumer-facing industrial services, highlighting the sector’s breadth. Deal sizes were generally modest, with the majority of CPS IPOs raising sub-$25 million. Large offerings such as Smithfield Foods, Alliance Laundry Holdings, Titan America, and McGraw Hill accounted for a disproportionate share of total capital raised, reinforcing investor preference for mature, cash-flow-generative businesses. A defining feature of the 2025 CPS IPO cohort was its international composition. A substantial portion of issuers were headquartered outside the U.S., particularly in Asia.

Looking ahead, CPS firms will have to navigate diverging demand and shifting trade rules. Against that backdrop, investors are likely to favor consumer businesses that can credibly articulate margin expansion through automation, supply-chain optimization, or data-driven demand forecasting.

IPO Outlook

Looking ahead, the setup for the U.S. IPO market in 2026 appears constructive, with momentum building off the strong rebound seen in 2025. Investor appetite for new issuances has clearly returned, and the pipeline of IPO-ready companies is deeper than it has been in years. Hundreds of late-stage venture- and sponsor-backed firms, many of them unicorns, have been waiting for a more stable window after deferring listings through prior volatility. If even a portion of this backlog comes to market, issuance volumes could rise meaningfully.

The potential for several high-profile listings will also define sentiment. Names widely viewed as generational private-market leaders could draw outsized demand and set a new benchmark for deal scale, forcing investors worldwide to recalibrate exposure across public equities.

That said, the outlook remains cautiously optimistic rather than unambiguously bullish. Key macro variables will determine how wide the IPO window opens. Declining interest rates could support higher valuations, while sticky inflation or unexpected trade-policy shocks could quickly tighten financial conditions.

- Patrik Kohary, “The Resurgence of SPACS in 2025,” Arc Group, November 4, 2025.”

- Arasu Kannagi Basil and Ateev Bhandari, “Insurance IPOs hit 20-year high on Wall Street after tariff-driven chaos,” Reuters, November 20, 2025.

- Sean Dunlop, “Financial Services: US Firms Performed Well in 2025, but Valuations Are Starting to Look Stretched,” Morningstar, January 16, 2026.