中文

中文

Appraisal cases in Delaware are closely watched due to their significance and impact on M&A decisions in boardrooms across the U.S. Although few in number, Delaware appraisal cases often involve companies that are household names, and the ramifications of appraisal cases are widespread. Recent appraisal decisions from the Delaware Court have generally confirmed the Court’s deference to the third-party deal price as indicative of fair value, except with respect to transactions involving related parties.

Appraisal statutes defined

Under section 262 of the Delaware General Corporation Law, “An appraisal proceeding is a legislative remedy intended to provide shareholders dissenting from a merger on the grounds of inadequacy of the offering price with a judicial determination of the intrinsic worth (fair value) of their shareholdings.” Appraisal cases generally arise when shareholders believe a merger transaction price is too low. The basic concept of appraisal is that the shareholder should be compensated for “that which has been taken from him, his proportionate interest in a going concern.”

In appraisal cases, each side has the burden of proving its case through the preponderance of the evidence. If both sides fail to prove their respective cases, the judge will determine fair value.

A growing number of appraisal cases

Since 2010, 15 appraisal cases have reached a final decision in Delaware Court. Few appraisal cases rise to the level of a final decision because mergers require the approval of the acquired company’s Board and stockholders, except in the case of short-form mergers. Layer on the lengthy time — it can take over two years — and the considerable expense it takes to get to a final decision, and the result is only a few Delaware appraisal cases per year.

In recent years, however, dedicated capital has been raised specifically to pursue appraisal cases challenging merger consideration in hopes that the Delaware Court will award fair value in excess of the merger consideration (this strategy is often referred to in shorthand as “appraisal arbitrage”). Merion Capital, for example, raised $800 million in its first fund in 2010 to pursue excess returns resulting from appraisal actions. Merion Capital has been involved in recent high-profile cases, such as 3M Cogent, Ancestry.com and BMC. Hedge fund interest in appraisal arbitrage was originally sparked by the Transkaryotic decision in 2010 because the Court held that equity holders who acquired their shares after a transaction’s record date can still assert appraisal rights. This enables appraisal investors to review the proxy in detail in order to determine whether a case has merit. In addition, once fair value is determined, the Court awards damages and interest at the “prudent investor rate,” which is often the Federal Reserve discount rate plus 5%. Given our current low-interest-rate environment, 5% is an attractive rate of interest that improves the economics of pursuing appraisal cases.

Results of appraisal cases since 2010

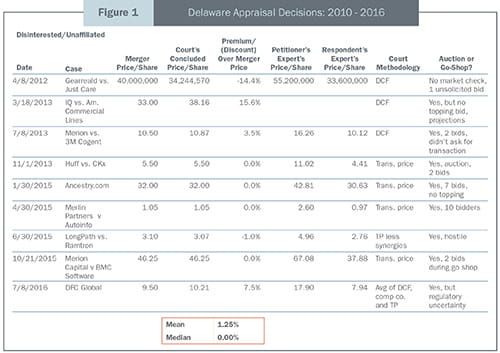

We reviewed 15 appraisal cases in Delaware and the results of the Court’s concluded price vs. the merger price (Figure 1). In the nine cases where there was a well-constructed sale process and a go-shop provision after a deal was struck, the Court awarded either no premium above the transaction price or a very small premium, which on average was 1.25%.

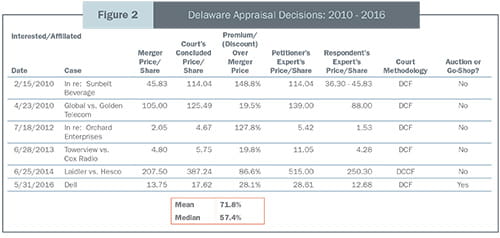

In contrast (Figure 2), the six related party sale transactions generally had weak or non-existent go shop processes, and resulted in substantial premiums awarded by the Court that ranged from 19.5% to 148.8% with a mean of 71.8% and a median of 57.4% over the transaction price. The data from the 15 cases reviewed suggests that related party transactions have a dramatically higher risk of a premium award in Delaware court, setting a high standard for constructing a merger process in related party transactions.

Dell decision: A new paradigm?

Delaware Court Vice Chancellor Laster found that Dell was sold for $6 billion too little in a going private, management buyout (“MBO”) transaction involving its founder, Michael Dell and financial sponsor, Silver Lake Partners. In arriving at this conclusion, Chancellor Laster dismissed the transaction price entirely as an indication of fair value. The Dell decision is a departure from the trend toward transaction prices as equivalent to fair value in Delaware appraisal cases. In five recent cases, the Delaware court has awarded no premium above the merger price. These five cases all involved transactions in which a merger process was considered to be arm’s length and conducted with sufficient depth.

Generally, Delaware courts have been reluctant to substitute their own fair value opinion if the merger consideration is derived from an arm’s-length sales process. In the Dell case, Dell argued they had run an arm’s length sale process and that the merger consideration was therefore the best evidence of the company’s fair value on the closing date. In fact, a special committee was formed and the special committee hired its own legal and financial advisors to conduct the sales process, which consisted of merger discussions with multiple bidders, including KKR and TPG. The merger agreement allowed for a 45 day go-shop period during which buyers were able to bring topping bids. During this period, 60 buyers were contacted and Blackstone and Carl Icahn brought bids, which ultimately pressured Silver Lake to increase its bid. The final bid accepted by the special committee represented a 38% premium over the 90 day public trading price.

Although traditionally the Delaware Court has focused more on stock market prices than on deal prices, deal prices have “long been considered in appraisal proceedings” and have been one of the “relevant factors” in determining fair value. If the merger giving rise to the appraisal case “resulted from an arm’s-length process between two independent parties, and if no structural impediments existed that might materially distort the crucible of objective market reality, then a reviewing court should give substantial evidentiary weight to the merger price as an indicator of fair value.”

The Court views public markets as liquid and efficient with “large numbers of identical shares traded by millions of participants,” and thus public markets are considered effective at determining value. In the sale of companies, however, “no two companies are exactly alike and the market for whole companies is unavoidably less efficient at valuing entire companies than the stock market.” The issue of efficient pricing is “especially pronounced in the context of MBOs.”

In the Dell case, the Court advanced three primary reasons to deviate from the transaction price in its award. First, the Court cited a lack of meaningful pre-signing competition as one of the reasons the deal price was not a reliable indicator of fair value. Specifically, the pre-signing merger process did not include any strategic buyers, which weakened the argument that the process was full.

In addition to a lack of pre-signing competition, the Court did not find the merger consideration to be a compelling argument for fair value because the financial advisors focused on an LBO model in determining the price they offered. LBO models are not necessarily known to be indicative of value, but rather are used to determine whether a potential investment meets an investor’s return hurdles. LBO models may, therefore, underestimate the true intrinsic value of a company in the Court’s opinion.

Lastly, the Court cited the compelling evidence of a significant valuation gap driven by the market’s short-term focus. Dell’s financial performance had been under pressure and the Company’s and the industry’s future was a matter of debate. Michael Dell, as founder and key shareholder, had an insider’s viewpoint on the future of the Company that was arguably asymmetric to other bidders. The Court had a difficult time reconciling Michael Dell’s plan to team with Silver Lake to pursue a growth strategy.

In the end, Chancellor Laster found that the merger consideration was inadequate and instead Laster used the petitioner’s DCF-concluded prices as the sole basis for determining fair value. In abandoning the arm’s-length, third-party price, the Court deviated from the recent trend of relying on the merger price in cases in which a sale process with multiple bidders is conducted. Whether this sets a new precedent for future appraisal cases remains to be seen, but is worth noting for Boards and their advisors to consider when conducting a sale process, particularly one involving a related party.

Source: Court of Chancery of the State of Delaware, various cases including, In Re: Appraisal of Dell, Inc.; Harvard Law School Forum.