Italiano

Italiano

Oncology practice transaction activity has been robust, with consistent interest from publicly traded companies, privately held oncology networks, and health systems. Oncology practices have also been increasingly involved in various partnerships, such as those with academic institutions and Cancer Centers of Excellence. Oncology acquisitions and partnerships are largely driven by increasing pressures on community oncology practices and the potential to achieve economies of scale, improve efficiency, and increase access to resources. Acquisitions and partnerships have the potential to improve patient outcomes by offering a broader range of treatments, expanding access to providers and clinical trials, and otherwise improving care through leverage of resources.

This article presents our outlook for the oncology sector while examining industry trends, recent transactions, and the factors expected to drive interest in oncology practice acquisitions.

Industry Overview

The U.S. oncology market was valued at $85.6 billion in 2024 and is projected to expand up to $189.6 billion by 2033.1 Growth is expected to be driven by rising cancer incidence and the expanding population of long-term survivors requiring ongoing care. Advances in precision medicine, targeted therapies, and immunotherapies are transforming cancer care and driving higher spending due to the growing investment in cutting-edge treatments. At the same time, improved diagnostics, expanded outpatient infrastructure, and supportive regulatory and reimbursement policies are increasing patient access and accelerating adoption of new therapies.

Approximately two million people in the United States are expected to have been newly diagnosed with cancer in 2025.2 According to the National Cancer Institute, there are over an estimated 18.6 million cancer survivors in the United States, representing approximately 5.4 percent of the population. This number is expected to grow to 26.0 million by 2040, and 19.2 million of these are expected to have lived five or more years after initial diagnosis.3

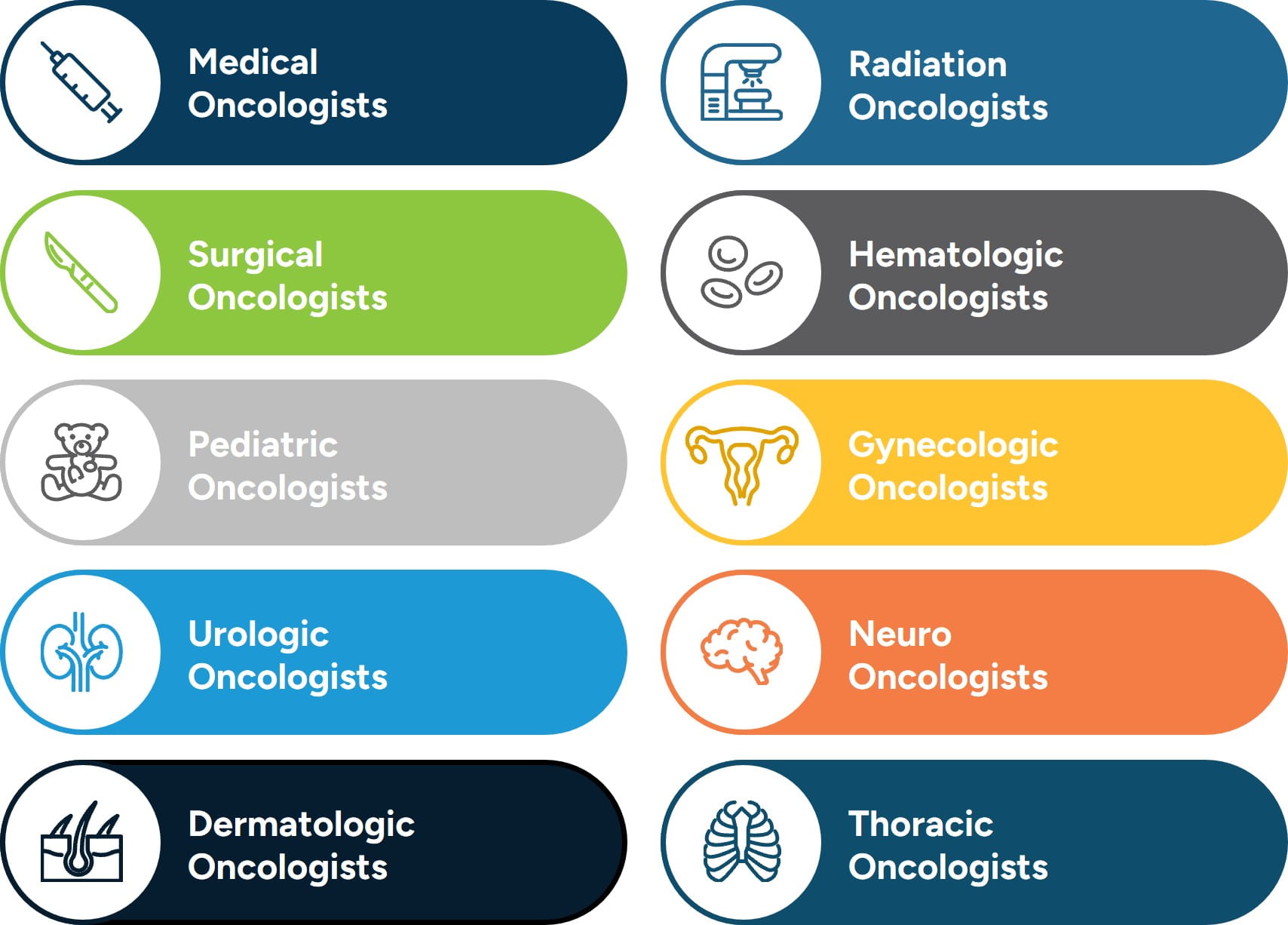

Oncology Specialties

Oncology encompasses a number of subspecialties, each focusing on different aspects of cancer care. These specialties often collaborate to provide comprehensive, multidisciplinary care tailored to each patient’s needs. Oncology is a highly specialized field, with different physicians focusing on distinct aspects of cancer care to provide comprehensive treatment. Medical oncologists focus on treating cancer with systemic therapies, including chemotherapy, biologics, hormone treatments, and targeted therapies, while radiation oncologists complement this approach by delivering precise, tumor-focused radiation. Surgical oncologists intervene directly, removing tumors, lymph nodes, and performing diagnostic biopsies, and hematologic oncologists concentrate on blood-related cancers such as leukemia and lymphoma. Pediatric oncologists, many trained in hematologic oncology, address the unique needs of children and adolescents, while gynecologic and urologic oncologists specialize in cancers of the female and male reproductive systems and urinary tract. Neuro-oncologists specialize in brain and nervous system malignancies, dermatologic oncologists treat a range of skin cancers, and thoracic oncologists focus on cancers within the chest, including lung and esophageal malignancies. Together, these specialists form a collaborative network, integrating their expertise to deliver patient-centered, multidisciplinary care across the cancer continuum.

Figure 1: Oncology Specialties

In addition to specialized medical care, oncology involves a range of diagnostic services and supportive care. Diagnostic tools, such as imaging, blood tests, biopsies, and genetic profiling, are essential for accurate staging and personalized treatment planning. Supportive care services, such as pain management, nutritional counseling, psychosocial support, palliative care, and survivorship care, play a critical role in maintaining quality of life throughout treatment and beyond. Many cancer centers also offer integrative or alternative therapies, including acupuncture, massage, and mindfulness-based practices, which can help manage symptoms and improve overall well-being.

Across the continuum of care, oncologists focus on delivering comprehensive and patient-centered care backed by the latest clinical evidence. When properly aligned, oncology subspecialties and support services can be joined together to create a multidisciplinary treatment experience that improves patient outcomes. Subspecialties that often require intensive collaboration, such as radiation, surgical, and thoracic oncology, can benefit from coordinated services when integrated. Other subspecialties, such as medical, gynecologic, urologic, and dermatologic oncology, may be better suited for structures that allow for greater autonomy, which enables providers to tailor care models more precisely to their patients.

Regardless of practice structure, operational and clinical success hinges on aligning strategic practice models, resource management, and care delivery with high-quality, evidence-based care, coordinated teamwork, and a strong focus on individualized care.

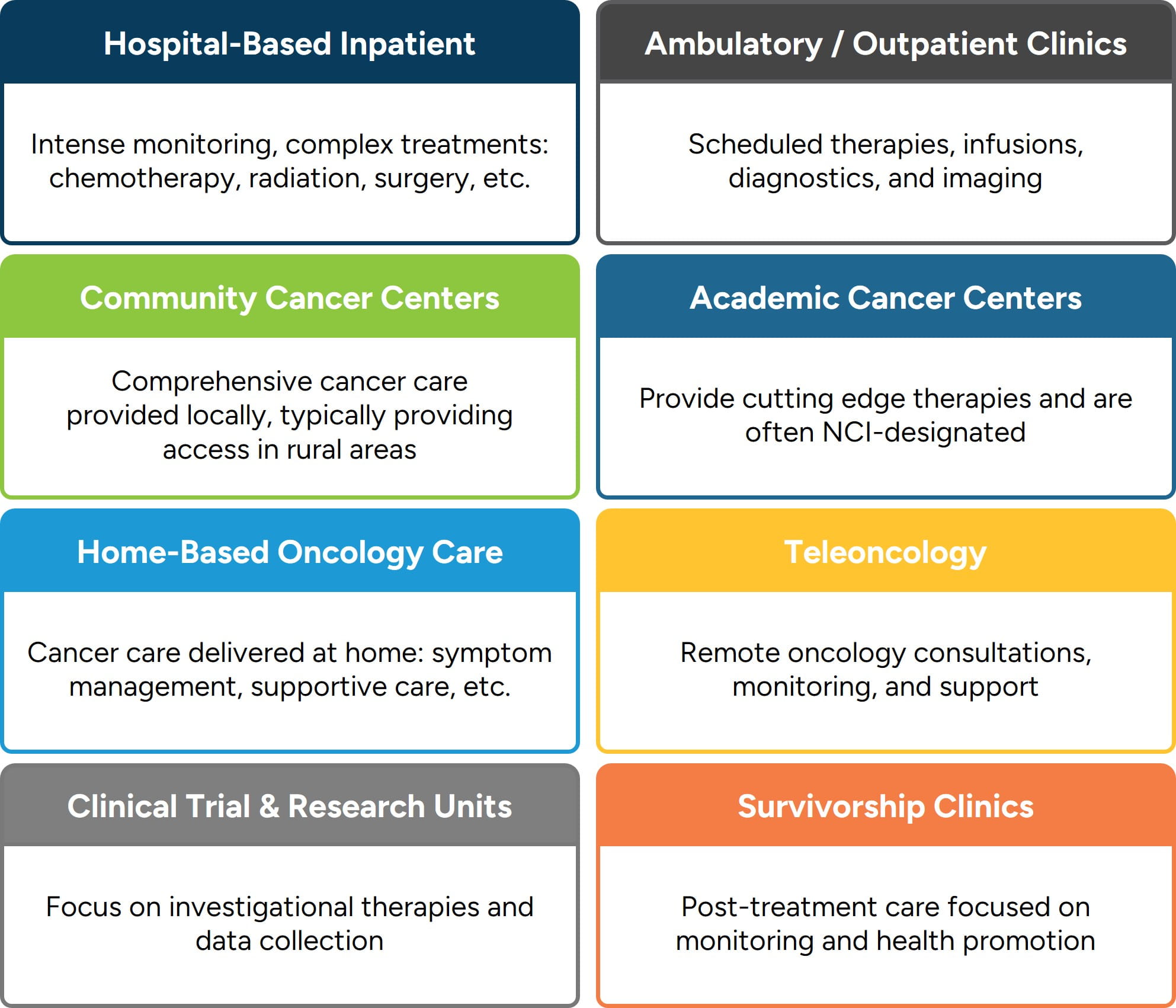

Care Settings

Oncology care is delivered across a variety of settings depending on the type and stage of cancer, treatment plan, patient needs, and available resources. Hospital-based inpatient oncology provides intensive monitoring and complex interventions, including chemotherapy, radiation, surgery, and palliative care for advanced cases. Outpatient and ambulatory clinics, the most common treatment settings, allow patients to receive scheduled therapies, infusions, labs, and imaging with convenience and continuity.

Community cancer centers bring comprehensive care closer to home, often in partnership with larger academic institutions, expanding access in rural and underserved regions. Academic and comprehensive cancer centers offer cutting-edge therapies, clinical trials, and multidisciplinary care, frequently earning recognition as Centers of Excellence, and many are officially recognized by the U.S. National Cancer Institute (NCI) with NCI designations.

Home-based oncology care supports patients with mobility limitations or those in palliative and hospice stages, providing monitoring, IV hydration, and symptom management in the comfort of their own homes. Tele-oncology extends the reach of care through virtual diagnostics, treatment guidance, and ongoing support, while clinical trial and research units give patients access to investigational therapies under close monitoring.

Survivorship clinics complete the continuum by focusing on long-term health, monitoring for recurrence, managing physical and psychosocial effects, and promoting wellness after a cancer diagnosis. These diverse care environments each carry implications, not only for clinical workflow, but also for the financial, operational, and strategic aspects of cancer care delivery.

Figure 2: Oncology Care Settings

Each treatment setting is designed to address distinct clinical needs, ensuring patients receive timely, appropriate, and effective care. These diverse settings also provide greater access, comfort, and continuity, ensuring support throughout the course of treatment. While enhancing the patient experience, they also present opportunities for operational efficiency, resource utilization, and long-term resilience. As oncology care continues to evolve, the integration and alignment of these settings will be essential to improving care quality while positioning organizations for continued strength within a challenging healthcare landscape.

The Pharmaceutical Industry's Role in Oncology

Pharmaceutical companies have been a driving force in oncology for decades. Initially, the emphasis lay on cytotoxic chemotherapies, which are agents that kill rapidly dividing cells but often injure healthy tissue as well. Over time, this evolved into more refined approaches: small-molecule targeted therapies that exploit specific molecular alterations in cancer cells, followed by the era of immunotherapies, such as checkpoint inhibitors. Those latter approaches — enabled by pharma R&D, scaled manufacturing, and global regulatory infrastructure — turned oncology from a largely palliative realm to one where durable remissions and improved survival are increasingly attainable.

In recent years, the scientific and commercial frontiers in oncology have shifted again. For example, antibody-drug conjugates (ADCs) are now a major modality: these therapies combine an antibody targeting a cancer cell antigen with a cytotoxic “payload,” offering enhanced specificity.4 The next generation of ADCs is pushing beyond current designs, incorporating bispecific antibodies, immune-stimulating payloads, pro-body formats (conditionally active in tumor micro-environment) and dual-drug conjugates.5 At the same time, major pharma companies are directing investment into cell- and gene-therapies, radiopharmaceuticals and bispecific approaches, all in the effort to overcome resistance and expand to new tumor types.

While the oncology-related pharmaceutical space has largely matured, transaction activity remains elevated. As one report notes, oncology was one of the most active therapeutic areas in 2024, reflecting an enduring commercial interest.6

At the same time, the nature of deals is shifting. Rather than mega-acquisitions of broad portfolios, the market is favoring bolt-on acquisitions and early-stage assets, with license, collaboration, and milestone-based structures.7 Valuation multiples for pharmaceutical oncology targets have also seen pressure with increased scrutiny of reimbursement, market access, and trial risk indicating that buyers are more conservative in pricing and structure.8 Overall, while oncology remains a top strategic priority in pharma, the dealmaking and valuation dynamics reflect a “next phase” of the industry which suggests high potential but higher expectations and more refined targeting.

340B Drug Discount Program

The 340B Drug Discount Program (“340B”) has had a particularly significant impact in the oncology industry due to the high cost of outpatient cancer drugs and the program’s pricing and reimbursement structure. The program, created in 1992, was designed to enable health care providers serving low-income and uninsured patients to purchase drugs at reduced prices by requiring drug manufacturers participating in Medicaid to offer certain drugs to eligible covered entities at discounted prices (known as the 340B ceiling price).9 Under 340B, eligible hospitals and cancer centers can purchase oncology drugs at discounted prices while generally receiving standard reimbursement for drug administration. Numerous entities are eligible to participate in the 340B program, including Federally Qualified Health Centers, Disproportionate Share Hospitals and Children’s Hospitals, Critical Access Hospitals and Rural Referral Centers, HIV/AIDS programs, and other specialized centers and clinics. Total 340B program spending in 2024 reached $81 billion, up 23% from the prior year.

These pricing and payment features have meaningful implications in oncology, where outpatient cancer drugs are among the most expensive and account for a substantial share of revenue for participating facilities. Recent analyses indicate that drug administration for oncology is increasingly shifting to 340B hospital outpatient departments, where both discounted drug acquisition costs and higher reimbursement rates apply.10 In addition, analysis by the Congressional Budget Office indicates that growth in 340B spending has exceeded market-wide spending growth for multiple drug classes, including cancer therapies.11 As a result, the combination of discounted acquisition costs and standard reimbursement in the program has created financial incentives that continue to reshape oncology site-of-care decisions.

Risk Factors and Demographics

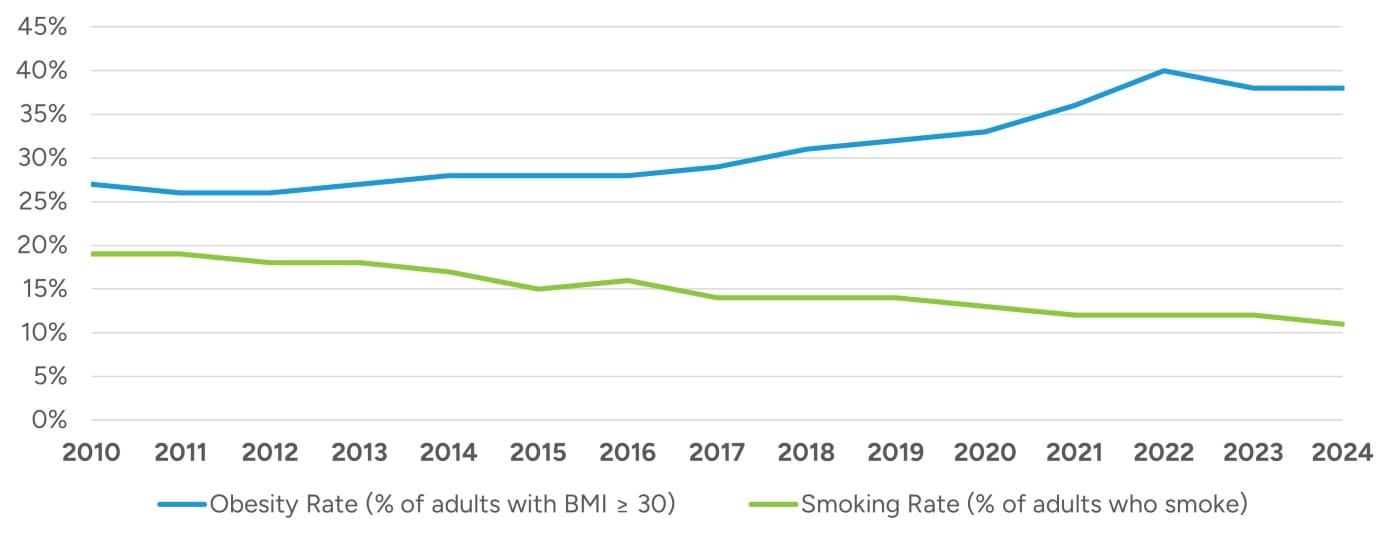

Approximately 40% of all cancer cases in the United States are associated with modifiable risk factors such as tobacco use, excess body weight, physical inactivity, excess exposure to ultraviolet radiation, alcohol consumption, environmental factors, and cancer-causing pathogenic infections.12 While tobacco use has continued to decrease, obesity rates have been increasing for a number of years as demonstrated in Figure 3.13,14 Additionally, obesity and metabolic risk factors, in particular, have been implicated in rising early-onset cancers which is driving demand for earlier screening, personalized treatment plans, and age-specific prevention strategies.15

A developing trend in the adoption of next-generation weight loss drugs, such as glucagon-like peptide-1 receptor agonists (GLP-1), has indicated significant promise in reducing obesity-related cancer (OCR), with one study indicating that a 10% GLP-1-related weight reduction could reduce over 1.2 million OCR cases by 2050.16

The United States population is projected to increase from 350 million in 2025 to 372 million in 2055 with the 65-and-older portion of the population projected to grow more quickly than younger groups.17 Cancer incidence is expected to increase as the population grows and ages, resulting in an increasing demand for treatments.

Figure 3: Notable Trends in Modifiable Risk Factors

Although cancer is often associated with older segments of the population, 14 types of cancer incidence have been increasing in adults under 50.18 Analysis of incidence patterns also shows that women under 50 now have substantially higher cancer rates than men in the same age group, with breast and thyroid cancers contributing to this shift.19 The market for consumer-facing health technologies tailored to younger demographics, such as risk assessment apps and digital monitoring tools, is expanding rapidly to address these trends.

Regional variations in cancer incidence influence how healthcare systems deliver and manage oncology services. For example, even though rural cancer mortality rates have been declining for some time, rates are still approximately one-fifth higher when compared with large metropolitan counties, with the most pronounced differences seen in lung and cervical cancer.20

Developing Trends in Patient Outcomes

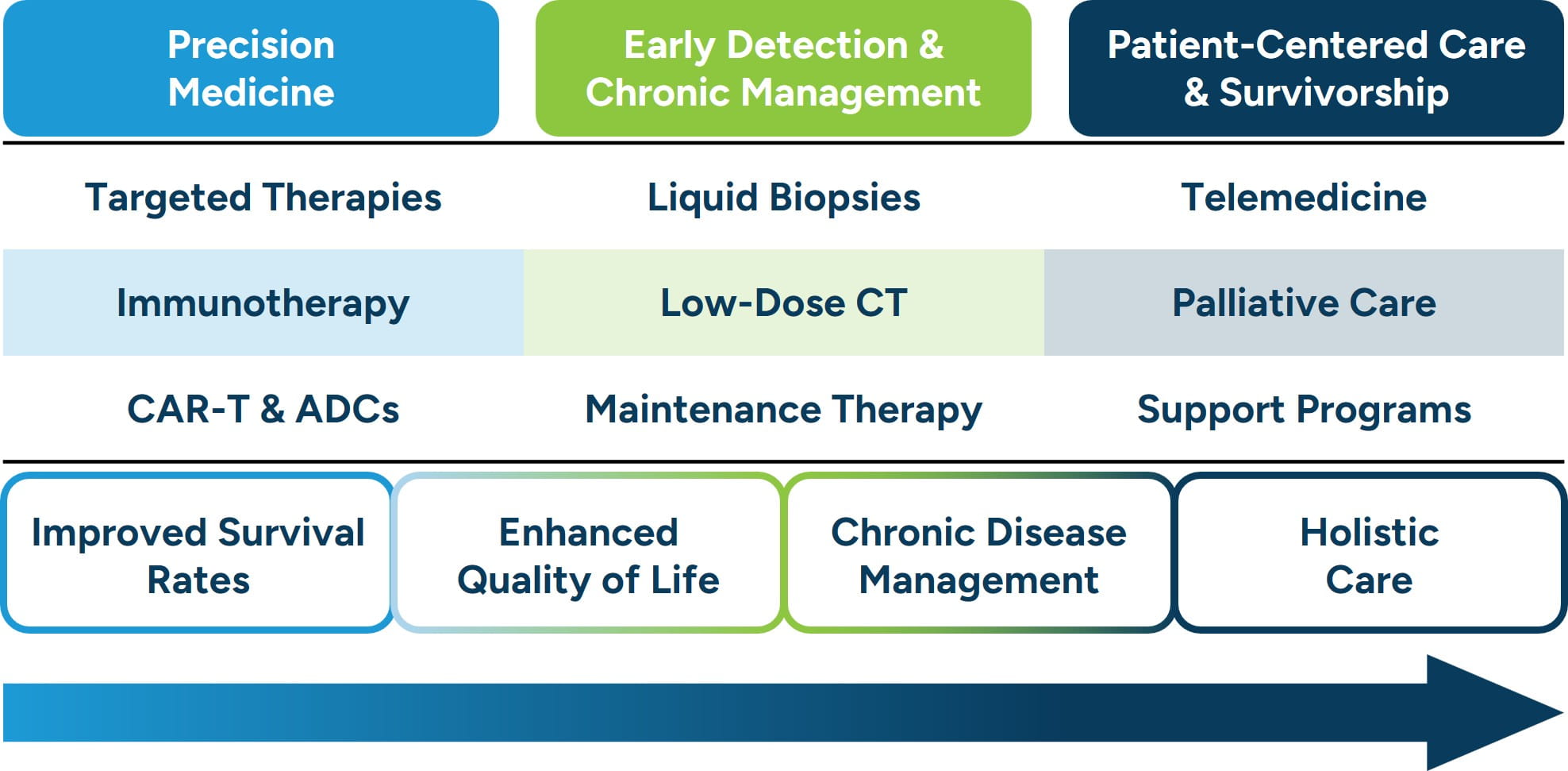

Over the past decade, oncology has undergone remarkable transformation, marked by measurable improvements in patient outcomes, survival rates, and quality of life. Driven by advancements in precision medicine, early detection, and evolving care delivery models, cancer treatment today is more personalized, accessible, and holistic than ever before. These developments have extended survival for many cancer types and redefined what it means to live with and beyond a cancer diagnosis. The three most significant trends contributing to this shift include the rise of biomarker-driven precision therapies, earlier detection combined with chronic disease management strategies, and a growing emphasis on care delivery innovation and survivorship.

Figure 4: Trends Contributing to Improved Patient Outcomes

One of the most transformative developments in oncology outcomes has been the evolution of precision medicine and biomarker-guided therapies. Instead of relying solely on tumor location and morphology, clinicians increasingly use genomic testing to identify mutations or molecular targets that drive cancer growth. This approach has given rise to targeted therapies, immunotherapies, and even cell- and gene-based treatments that specifically attack cancer cells while sparing healthy tissue. Recent data show that novel modalities such as PD-1/PD-L1 inhibitors, CAR-T therapies, and antibody-drug conjugates have dramatically improved progression-free and overall survival rates for patients with previously intractable cancers.21,22 Precision medicine has thus shifted cancer treatment from a standardized model to one that is deeply individualized, yielding both longer survival and improved quality of life.

A second major shift in oncology outcomes stems from improvements in early detection and the evolving management of advanced cancers as chronic conditions. The integration of advanced diagnostics, such as liquid biopsies and low-dose CT screenings, allows cancers to be identified at earlier, more treatable stages. Simultaneously, the use of maintenance therapies and long-term immunotherapy regimens has allowed patients with metastatic disease to experience extended survival. For example, in non-small cell lung cancer, the median duration of first-line treatment has quadrupled since 2011, reflecting the new paradigm of long-term disease management rather than acute end-of-life care.23 As more patients live longer with cancer, the field increasingly mirrors chronic disease models, focused on ongoing control, continuous monitoring, and sustained quality of life.24

The third emerging trend focuses on how care is delivered, emphasizing patient-centered models, quality of life, and survivorship. Health systems are investing in integrated care pathways that include telemedicine, palliative care, and community-based oncology programs to reduce disparities in access. These innovations expand reach and improve patient engagement and adherence. Moreover, survivorship programs now prioritize mental health, fatigue management, and long-term toxicity prevention, which are areas that were once overlooked in the acute treatment phase. Recent evaluations of oncology delivery models report that comprehensive and coordinated care improves the patient experience and can contribute to better overall outcomes by addressing the whole person rather than cancers alone.25 This trend underscores the growing recognition that how care is delivered is as vital as what therapies are used.

Oncology patient outcomes have improved dramatically over the past ten years, driven by interconnected advances in precision therapies, earlier detection, and patient-centered care models. Together, these trends have shifted the focus of oncology from solely prolonging life to enhancing quality-of-life and focusing on sustainability. As research and technology continue to evolve, the next decade promises even greater strides, potentially transforming cancer from a terminal diagnosis into a manageable condition for many.

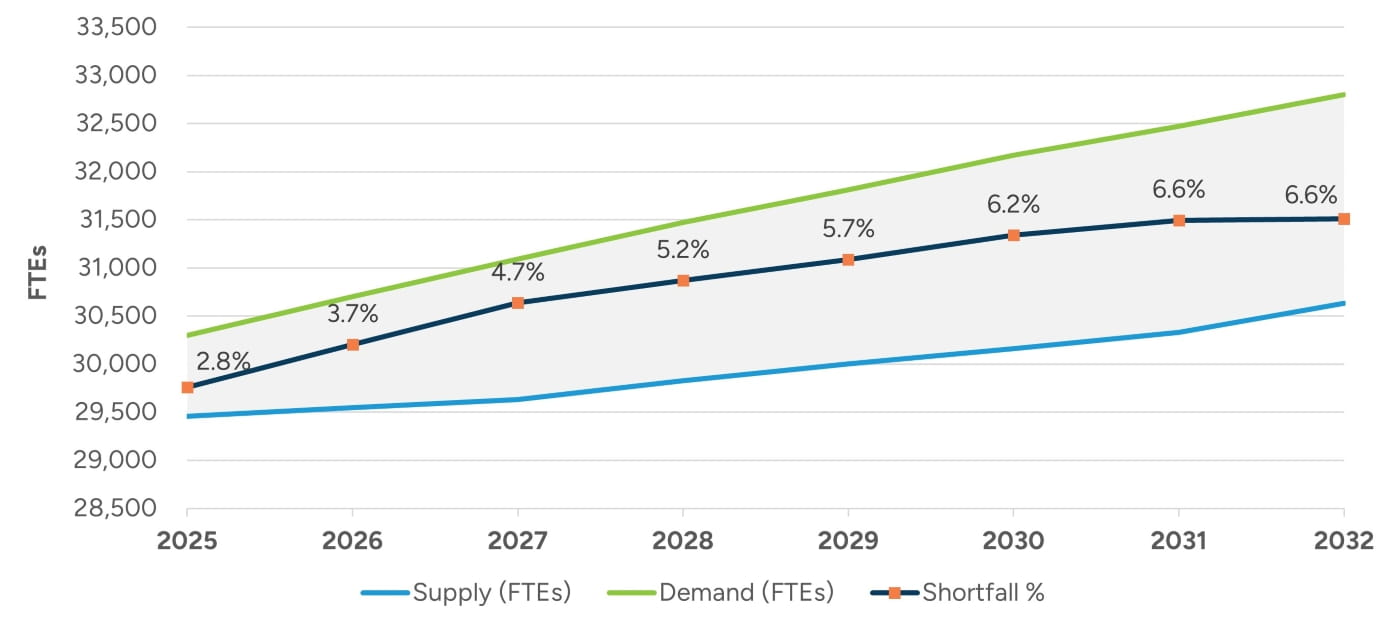

Figure 5: Oncologist Shortage Expected to Increase

Provider Shortages

Data from the Health Resources and Services Administration (HRSA) indicates that there are nearly 29,500 full-time equivalent (FTE) hematology, oncology, and radiation oncology physicians practicing in the United States; however, HRSA projections indicate that demand for these physicians will outpace supply over the coming years as illustrated in Figure 5.26 The anticipated shortage will likely be impacted by factors such as an aging patient population, an aging workforce, increasing cancer incidence, and growing survivor populations that will require long-term care. Further adding to the strain are limited training slots for new oncologists, rising burnout rates, and an uneven geographical distribution of specialists.

Provider Compensation

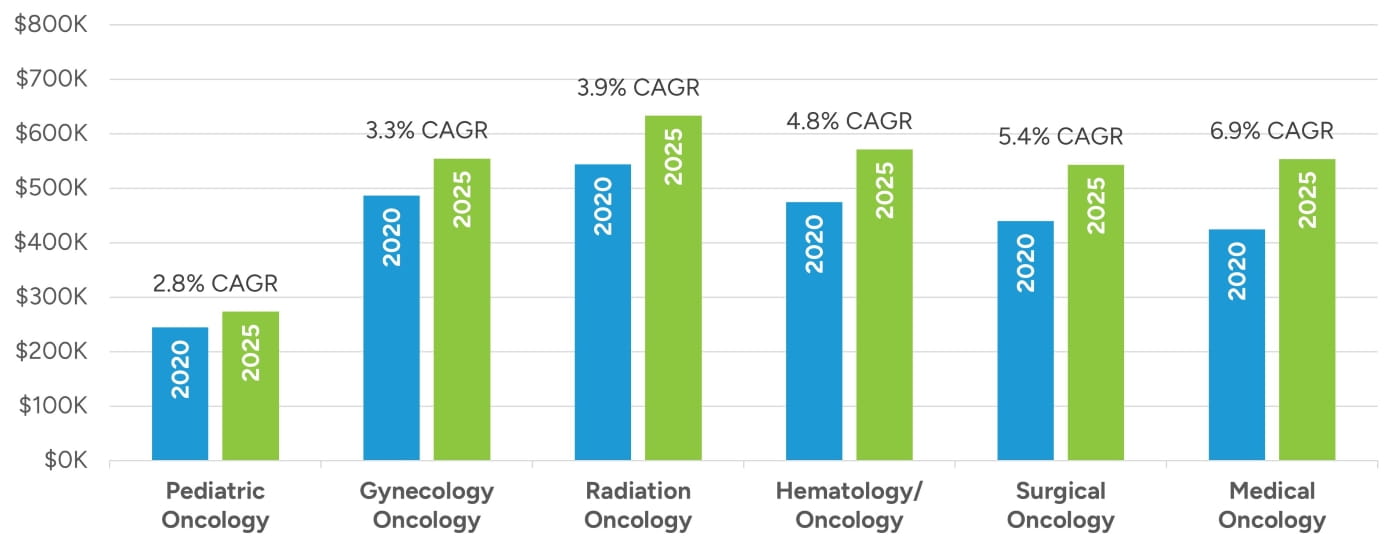

Compensation for oncology providers has increased at or above nominal rates in recent years based on our review of compensation data reported by MGMA and AMGA as depicted in Figure 6. Median compensation has increased most notably within the medical oncology specialty, increasing at a compound annual growth rate (CAGR) of nearly seven percent for the five-year period ending in 2025. Hematology/oncology and surgical oncology have also seen notable increases of around five percent CAGRs, and radiation oncology has also increased at a CAGR of nearly four percent. Pediatric and gynecologic oncology have grown at more moderate levels in the three percent CAGR range over the past five years.

Figure 6: Median Oncologist Compensation

Numerous factors have been contributing to upward pressure on oncology compensation. Demand for oncology services has been increasing largely due to the aging population. As people live longer, the incidence of cancer rises significantly, creating a larger patient base that requires specialized treatment. This surge in demand places pressure on a limited supply of oncology specialists, intensifying competition among employers. To maintain and attract top talent, healthcare organizations often redesign compensation and incentive structures in addition to other retention and talent acquisition strategies.27

Rising survival rates have also contributed to increasing oncologist compensation. As prevalence grows (i.e., the number of people alive with a history of cancer), more patients remain in active or follow-up care. Thus, oncologists are increasingly caring for patients beyond the initial treatment phase, resulting in increased patient volume. In a healthcare environment facing increasing provider shortages, oncology physicians in high-demand areas can often command higher compensation. Additionally, as the cumulative revenue opportunity per patient increases, so does the economic leverage of oncology providers.

Physician compensation models have also been evolving, shifting away from traditional salary-based structures to more performance- and productivity-driven models.28 Additionally, half of healthcare organizations now incorporate metrics, such as patient outcomes, quality of care, and value-based performance, into compensation packages.29 As a result of these evolving models, many physicians are experiencing increased compensation tied to their efficiency, patient outcomes, and contributions to value-based care.

Reimbursement

Reimbursement within the oncology segment of the healthcare industry has also undergone significant changes in recent years, driven by federal policy reforms, payor cost-containment efforts, and a gradual shift toward value-based care models. While advances in cancer treatment and diagnostics have improved outcomes, they have also increased the overall cost of oncology care, prompting both public and private payors to implement measures to manage expenditures. These efforts include expanded use of prior authorization, site-of-care redirection, and increased reliance on alternative payment models such as the Enhancing Oncology Model (EOM), which ties provider compensation to total cost and quality outcomes rather than service volume.

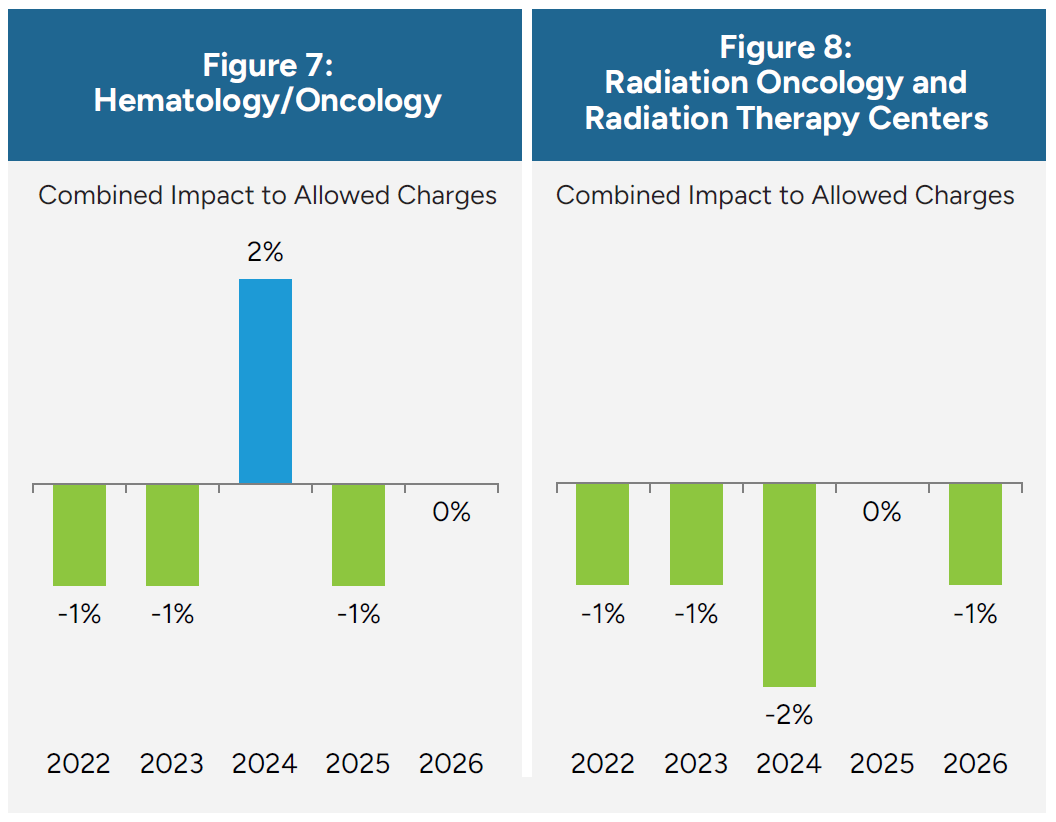

Medicare Physician Fee Schedule (MPFS) changes have generally reduced or constrained reimbursement within the oncology segment of the healthcare industry, as outlined for the observed subspecialties in Figure 7 and Figure 8. These reductions have particularly affected physician-administered drug margins, evaluation and management (E/M) services, and radiation oncology technical payments. For practices operating primarily under the fee-for-service (FFS) model, these adjustments have eroded traditional revenue streams, forcing oncologists to absorb rising practice costs while receiving lower reimbursement per encounter. Smaller independent practices in particular face growing financial strain as they struggle to balance staffing, compliance, and technology investments required to meet federal quality reporting and prior authorization demands.

As a result, the financial pressures stemming from MPFS updates and broader payor trends are accelerating structural changes across the oncology landscape. Many practices are responding by consolidating into larger networks, affiliating with hospital systems, or participating in value-based payment arrangements that reward cost efficiency and care coordination. Others are diversifying revenue by expanding infusion services, adopting oral oncolytic management programs, or partnering with specialty pharmacies and management services organizations (MSOs). Together, these dynamics illustrate how reimbursement policy continues to shape oncology economics and the organization and delivery of cancer care nationwide.

Support Staff and Practice Operations

Oncology practices rely on a multidisciplinary blend of advanced practice providers (APPs), clinical staff, administrative personnel, and specialized support roles to coordinate care across diagnostics, treatment, and follow-up phases while managing high patient volumes and complex regulatory requirements. Modern oncology staffing reflects a team-based care model that integrates medical, operational, financial, and psychosocial expertise. In addition to APPs and nurses, practices increasingly depend on oncology pharmacists, genetic counselors, financial navigators, social workers, research coordinators, tumor registrars, and data analysts to ensure safe, compliant, and patient-centered care.

Workforce pressures, such as rising patient demand, reimbursement constraints, and provider burnout, continue to drive structural change across oncology staffing models. Practices are increasingly turning to expanded APP utilization to offset physician shortages and maintain access to timely care, particularly in community oncology settings where the oncologist supply remains limited. APPs are now managing larger panels of established patients, conducting symptom management visits, and supporting survivorship programs to fulfill roles that were once the exclusive domain of physicians.30 This trend not only alleviates scheduling bottlenecks but can align with value-based care goals by enhancing continuity, patient education, and outcomes.

At the same time, oncology practices are restructuring clinical operations to enable greater flexibility across infusion services, patient triage, and care coordination in response to ongoing workforce constraints. Care teams are being designed to support broader role coverage, with nurses, medical assistants, and patient navigators assuming additional responsibilities related to documentation support, oral therapy monitoring, and digital care coordination. Such flexibility has become increasingly important as patient complexity grows and care delivery continues to extend beyond traditional clinic environments to include virtual care, multidisciplinary programs, and non-facility-based treatment settings.31

Another notable shift in oncology practice management has been the growing reliance on strong administrative and data infrastructure to sustain quality, compliance, and financial viability amid tightening reimbursement and reporting requirements. Practices are expanding teams of billing specialists, revenue cycle personnel, and clinical data professionals to support more granular documentation, prior authorization workflows, and quality reporting now expected by payors and regulators. In oncology programs accredited by the Commission on Cancer (CoC), detailed quality measures derived from cancer registry data, such as timely initiation of adjuvant therapies and documentation of key staging information, are centrally reported through platforms like the Rapid Cancer Reporting System.32 Additionally, Medicare reimbursement changes that introduce payment for services, such as patient navigation and social determinants of health assessments, have underscored the importance of compliance documentation, coding expertise, and trained support staff to both deliver and bill for these evolving care components.33

Looking ahead, oncology practices are increasingly moving toward integrated, data-driven care teams that combine clinical expertise with administrative and analytic capabilities. By redesigning workflows, empowering APPs and multidisciplinary staff, and leveraging data infrastructure, practices can optimize clinical capacity, maintain regulatory compliance, and sustain financial performance. This approach can position oncology organizations to deliver high-quality, patient-centered care while adapting to ongoing workforce pressures, evolving payor requirements, and the expanding complexity of modern cancer care delivery.

Equipment Requirements

Oncology practices depend on a wide range of specialized diagnostic, therapeutic, and supportive equipment. The specific mix varies by subspecialty focus and scope of services offered. Equipment investment is often among the largest capital costs for oncology providers, requiring strategic planning, financing, and utilization management to maintain financial viability.

Equipment requirements in oncology vary widely by subspecialty, reflecting the distinct clinical and technological demands of medical, radiation, and surgical oncology. Medical oncology practices rely on infusion chairs, pumps, biosafety hoods, compounding and storage equipment, and integrated electronic systems to manage chemotherapy administration and patient monitoring. Radiation oncology is among the most capital-intensive segments, requiring linear accelerators, CT simulators, treatment planning software, dosimetry systems, and specialized shielding infrastructure to deliver precise radiation therapy. Surgical oncology depends on hospital-based operating environments equipped with robotic and laparoscopic systems, intraoperative imaging, and advanced sterilization technology. Collectively, these subspecialties rely on a sophisticated and interdependent equipment ecosystem that enables accurate diagnosis, individualized treatment, and longitudinal cancer care.

Oncology practices employ a range of financing strategies to acquire and maintain essential equipment, balancing clinical capability with financial sustainability. The choice between purchasing, leasing, or entering shared or managed service arrangements depends on capital availability, technology lifecycle, and long-term operational goals. Figure 9 summarizes common acquisition models used in the oncology segment, outlining their key characteristics, advantages, and limitations in supporting practice growth and technological advancement.

Figure 9: Advantages and Disadvantages of Equipment Acquisition Models

|

Model |

Description |

Advantages |

Disadvantages |

|---|---|---|---|

| Outright Purchase | Full ownership of equipment, typically financed through capital budgets or loans | Long-term cost efficiency; asset control | High upfront cost; technological obsolescence risk |

| Leasing/Equipment Financing | Pay over time via lease or capital lease arrangements | Lower initial expense; potential tax advantages; access to newer tech | Higher total cost over life; dependency on lessor terms |

| Managed Equipment Services (“MES”) | Vendor provides equipment, maintenance, and upgrades for a bundled fee | Predictable costs; guaranteed uptime; vendor-managed upgrades | Less flexibility; long-term contract obligations |

| Shared Ownership / Joint Ventures | Multiple entities (e.g., hospital and practice) co-own or co-use equipment | Spreads cost burden; improves utilization | Complex governance; regulatory considerations |

Equipment strategies in oncology are closely tied to practice size, available capital, and patient volume. Smaller or independent practices typically limit in-house equipment to infusion and basic laboratory services, relying on hospitals or imaging centers for advanced diagnostics and radiation therapy; these groups often favor leasing, vendor financing, or shared-use agreements to manage costs. Mid-sized regional networks may invest selectively in imaging or pharmacy infrastructure and leverage group purchasing organizations (GPOs) to obtain better pricing and service contracts. Larger integrated systems and hospital-based programs, by contrast, tend to purchase high-cost equipment outright and maintain full-service capabilities across medical, radiation, and surgical oncology. To offset these significant investments, practices of all sizes use strategies such as vendor negotiations, GPO participation, shared ownership models, research partnerships, and value-based contracting, while some pursue technology refresh programs or diversified revenue streams to balance capital spending with long-term financial performance.

Ownership Structures

The oncology care landscape encompasses a range of ownership and organizational structures, each shaping how care is delivered and scaled. These include publicly traded companies that operate for-profit hospitals, outpatient centers, or national networks; integrated health systems that may be nonprofit or for-profit and combine hospitals, physician practices, and outpatient services; and private-equity-backed platforms that consolidate independent practices into larger organizations. Academic medical centers deliver oncology care through university-affiliated hospitals that integrate research, education, and clinical trials, while Centers of Excellence consist of specialized cancer programs recognized for advanced, multidisciplinary treatment models. Independent oncology practices remain physician-owned and community-based, typically operating outside of large hospital systems or corporate networks.

Figure 10: Ownership Structures

Each ownership structure offers distinct advantages that influence patient access, innovation, and care experience. Public companies and private equity platforms generally provide strong access to capital, enabling investment in technology, infrastructure, and geographic expansion. Health systems and academic centers excel in care coordination and clinical integration, often supporting complex cases and comprehensive treatment pathways. Academic centers and Centers of Excellence are key drivers of innovation through research, clinical trials, and early adoption of advanced therapies. Independent practices tend to offer greater physician autonomy, closer patient–provider relationships, and lower-cost community-based care, while larger organizations often improve access and scale but may involve higher costs or reduced physician independence. Together, these models create a diverse oncology ecosystem that balances innovation, efficiency, access, and personalized care.

License Agreements in Oncology

License agreements in oncology involve the granting of rights to use intellectual property, such as patents, proprietary technology, or clinical data, to another party under defined terms. These agreements facilitate collaboration between biotech companies, pharmaceutical firms, academic institutions, and healthcare providers, enabling commercialization of therapies and diagnostics without requiring the licensee to independently develop the underlying technology. Licensing can also mitigate financial risk, accelerate development timelines, and expand market access for innovative oncology treatments.

The value of an oncology licensing agreement depends on both the underlying intellectual property and the specific terms of the license. Factors that influence value include the scope and exclusivity of rights granted, the remaining patent life, geographic coverage, field-of-use limitations, and obligations for milestone or royalty payments. The stage of development of the licensed therapy, whether preclinical, clinical, or commercial, affects projections of future revenue and associated risk. Regulatory pathways, competitive dynamics, market size, and reimbursement potential in target jurisdictions also play key roles in shaping value. Strategic elements, such as opportunities for co-development, sublicensing, or integration into a broader portfolio, can further enhance the agreement’s worth.

Ultimately, the value of a licensing agreement reflects a balance between expected cash flows and the probability of clinical, regulatory, and commercial success, often requiring scenario analysis to capture the inherent uncertainty in oncology therapeutics. We observe a wide range of licensing agreement structures and fee types in the oncology space.

Data Sharing in Oncology

Data sharing refers to the exchange of patient data, clinical trial results, genomic information, and other real-world evidence among healthcare institutions, research organizations, and biotechnology or pharmaceutical companies. Project GENIE, a consortium led by the American Association for Cancer Research that aggregates clinical and genomic data shared among 20 cancer centers, is one notable example of data sharing in the industry.34 Data sharing enables improved clinical decision making, more personalized treatment approaches, and accelerated drug development. While the benefits can be substantial, data sharing is subject to strict regulatory oversight, including patient privacy protections under Health Insurance Portability and Accountability Act (HIPAA), as well as considerations related to data standardization and interoperability.

When valuing oncology-related data assets, key considerations include the uniqueness and quality of the data, regulatory compliance, access restrictions, and the potential for monetization through partnerships, licensing, or internal research and development efficiencies. High-quality, longitudinal datasets with genomic or biomarker information tend to be of higher value due to their scarcity and ability to support precision oncology research. Stout has extensive experience and proven valuation expertise in data sharing. See our article, “Mining for Healthcare Gold: The Value of Healthcare Data,” for further detail.

Transaction Activity

Industry consolidation in oncology patient services has increasingly been driven by a relatively concentrated group of scaled national platforms and strategic industry participants. Large networks such as City of Hope, OneOncology (Cencora), The US Oncology Network (McKesson), Florida Cancer Specialists & Research Institute, and American Oncology Network have led transaction activity through a mix of acquisitions, network affiliations, and strategic partnerships designed to build multi-state clinical density, expand research and clinical trial infrastructure, and enhance value-based and technology-enabled care capabilities.

Academic medical centers and NCI-designated cancer centers remain active participants but typically pursue transformative collaborations, joint ventures, and purpose-built facilities rather than serial practice acquisitions, reflecting their focus on mission alignment, research scale, and complex care delivery. Centers of Excellence and high-outcome platforms have become increasingly attractive as partners, and, in some cases, acquisition targets, particularly for organizations seeking payor alignment, employer engagement, and differentiated oncology delivery models. Transaction structures and implied valuations vary widely, influenced by provider scale, geographic reach, ancillary capabilities, research infrastructure, and perceived long-term strategic value, including clinical trial infrastructure, data assets, and other ancillary or platform capabilities.

Major Transactions

Major transactions have reshaped the oncology patient services landscape in the United States over the past several years. These transactions highlight increasing consolidation and strategic realignment across oncology care delivery, practice management, and supporting services.

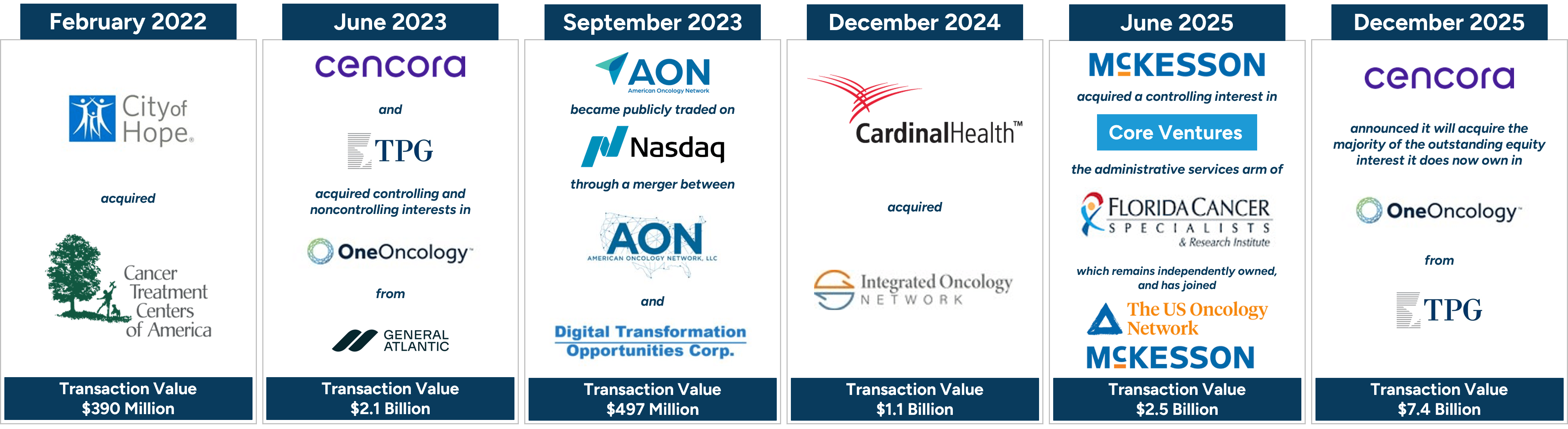

City of Hope, an NCI-designated comprehensive cancer center, completed the acquisition of Cancer Treatment Centers of America (CTCA) in February 2022, resulting in a combined organization of more than 575 physicians across California, Arizona, Illinois, and Georgia.35

Cencora (formerly Amerisource Bergen) and TPG completed the acquisition of One Oncology from General Atlantic at a valuation of $2.1 billion in June 2023.36 Cencora acquired a minority interest, and TPG acquired the remaining majority interest.37 In December 2025, Cencora announced that it will acquire the majority of the outstanding equity interest that it does not currently own in OneOncology from TPG; the transaction values OneOncology at $7.4 billion.38

In September 2023, American Oncology Network became a publicly listed company on Nasdaq through a business combination with a special purpose acquisition company in a transaction valuing the combined company at approximately $497 million.39

Cardinal Health acquired Integrated Oncology Network in December 2024, integrating over 100 providers at more than 50 practices across 10 states into Cardinal Health’s oncology practice alliance, Navista.40

In June 2025, McKesson Corporation acquired a controlling interest in Community Oncology Revitalization Enterprise Ventures, LLC (Core Ventures), a business and administrative services organization established by Florida Cancer Specialists & Research Institute, LLC (FCS). FCS remains independently owned although the company joined The US Oncology Network (McKesson’s oncology organization) following the transaction. FCS has more than 250 physicians and 280 advance practice providers with nearly 100 locations in Florida.41

McKesson, Cardinal Health, and Cencora have moved beyond pharmaceutical distribution to expand vertically across the oncology value chain. Each continues to anchor its strategy in specialty and oncology drug distribution while expanding downstream into community oncology networks and practice-enablement models that embed them more directly into provider economics and operations.

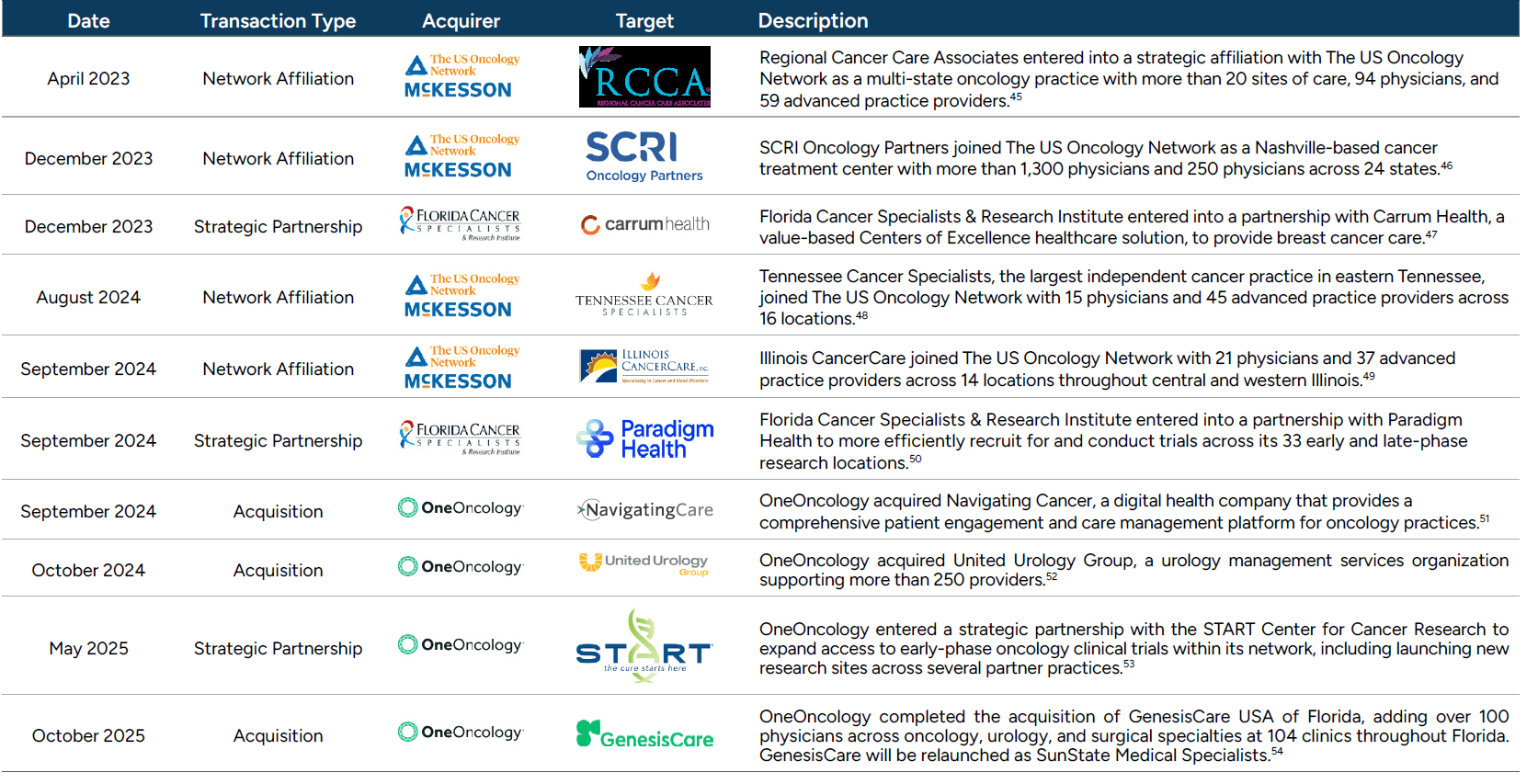

Figure 11: Notable Transactions

Transactions Involving Large Networks

Beyond major transactions, the U.S. oncology patient services market has been increasingly shaped by a broad set of strategic partnerships, affiliations, and acquisitions focused on building clinical density, expanding geographic reach, and enhancing research, technological, and value-based care capabilities. Many of these initiatives involve the largest national oncology platforms: City of Hope; The US Oncology Network (McKesson)42 ; OneOncology (Cencora); Florida Cancer Specialists & Research Institute; and American Oncology Network, highlighting the degree to which industry growth and innovation are being driven by a relatively concentrated group of scaled operators.

Collectively, these organizations have pursued strategies centered on multi-state integration, physician alignment, expanded access to clinical trials, and enhanced patient engagement infrastructure, reinforcing their positions as leading consolidators and strategic partners for independent oncology practices across the country, as illustrated in Figure 12. While no American Oncology Network acquisitions are displayed in Figure 12, the company has added dozens of new practices and providers in 2025, growing from over 220 providers in 2024 to over 300 across 20 states in 2025.43,44

Figure 12: Transactions Involving Large Networks

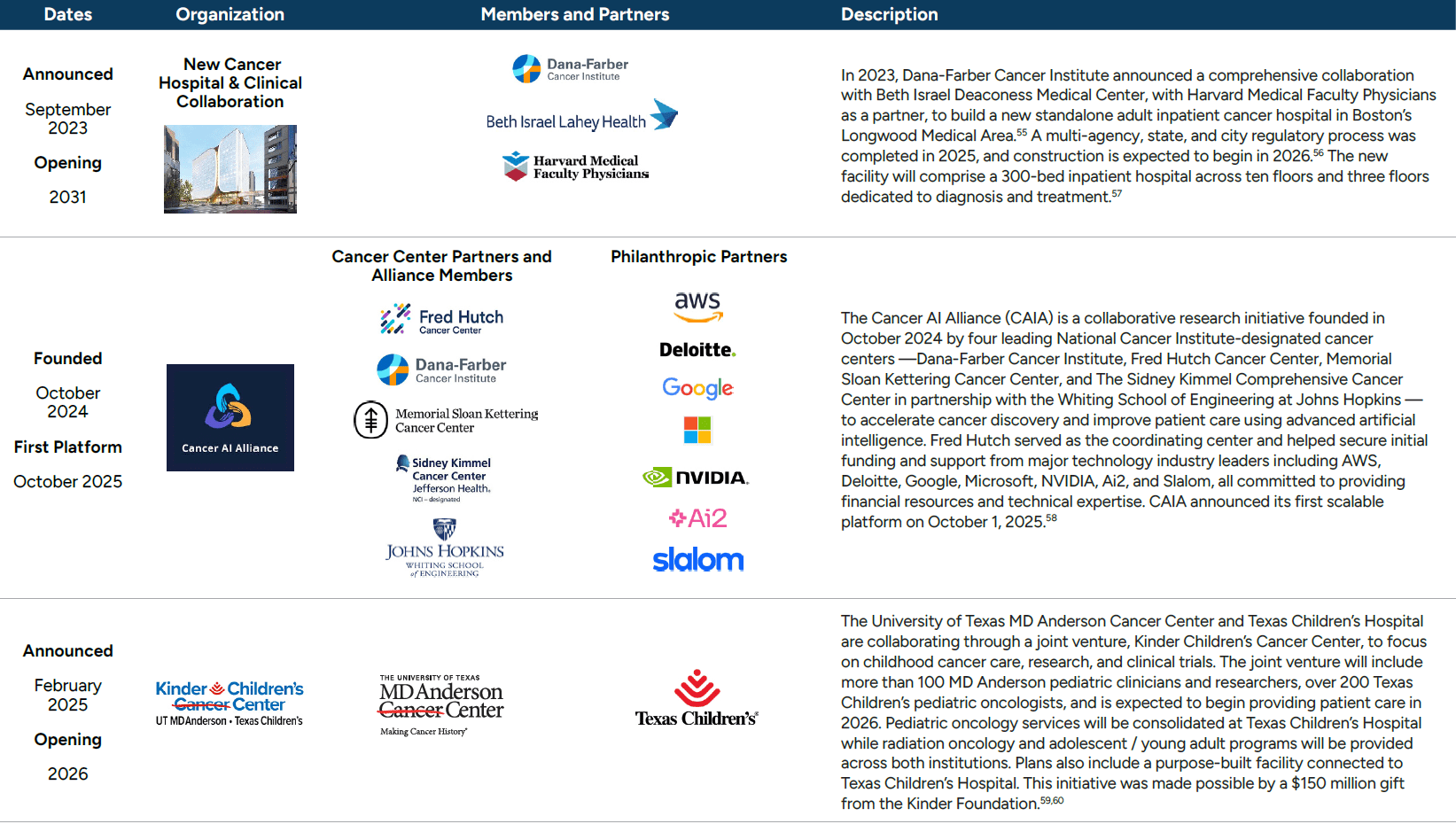

Figure 13: Recent Collaborations

Academic Centers and Centers of Excellence Collaborations

Leading academic institutions and NCI-designated cancer centers are increasingly pursuing large-scale collaborations, joint ventures, and research alliances to expand clinical capacity, accelerate discovery, and enhance specialized cancer care delivery. These initiatives reflect a growing emphasis on purpose-built facilities, cross-institutional integration, and advanced research and data infrastructure to support translational science, clinical trials, and complex patient populations. Recent examples illustrate how nationally-recognized cancer centers are leveraging partnerships across health systems, universities, philanthropic organizations, and the technology sector to advance their long-term clinical, research, and educational missions.

Looking forward, the industry is shifting toward integrated, technology-enabled oncology platforms, with AI-driven initiatives, such as the Cancer AI Alliance, enhancing clinical decision making, accelerating research, and improving patient outcomes, positioning the market for continued growth, innovation, and value-based care adoption.

Valuation Multiples

Acquisition multiples of oncology practices can vary greatly, with factors such as size and scale of group, location, site of care, mix of ancillary offerings in place, exposure to value-based payment models, referral management, and growth outlook being a few of the factors that can impact transaction consideration. Based on our experience observing closed transactions, small to midsize groups are likely to attract EBITDA multiples in the mid-to-high single digits, with large platform acquisitions commanding double-digit multiples as displayed via the examples in Figure 14.

Figure 14: Example EBITDA Multiples by Practice Size

Figure 15 outlines the range of observed EBITDA multiples across oncology transactions.61 The data indicates that transactions typically occur at high single to low double digits; however, higher multiple transactions may be achievable under certain circumstances.

Figure 15: Range of EBITDA Multiples

| 10th percentile | 3.4x |

| 25th percentile | 5.8x |

| Median | 9.3x |

| 75th Percentile | 13.6x |

| 90th Percentile | 19.0x |

The most notable and recent platform transaction was the Cencora acquisition of OneOncology in 2025. Cencora previously acquired a minority interest in OneOncology in 2023 in partnership with TPG which acquired a majority position. The 2023 transaction included call and put options: Cencora could purchase the remaining interest in OneOncology from TPG, or TPG could sell the remaining interest in OneOncology to Cencora. These options included in the 2023 transaction imply that the 2025 transaction occurred at a 19x EBITDA multiple before various other adjustments and qualifications.62

Industry Outlook

The U.S. oncology industry is positioned for continued growth driven by rising cancer incidence, expanding survivor populations, and ongoing innovation in precision medicine, immunotherapies, and targeted treatments. Over the next decade, we expect growth to accelerate as practices adopt advanced diagnostics, including liquid biopsies and AI-powered imaging, enabling earlier detection and more personalized treatment strategies. We also have a positive outlook for outpatient, community-based, and home care settings, supported by tele-oncology and remote monitoring, improving patient access, convenience, and continuity of care, particularly in underserved regions.

Workforce and reimbursement dynamics will continue to shape the oncology landscape. With a projected oncologist shortage and growing patient complexity, multidisciplinary teams will play an increasingly central role in care delivery. Practices that leverage robust data infrastructure, performance-based compensation, and value-based care models are likely to outperform, delivering both financial resilience and high-quality, patient-centered outcomes. Looking ahead, the convergence of innovative therapies, integrated care delivery, and technology-driven operational models positions the oncology sector for sustained growth, improved patient outcomes, and greater equity in access to advanced cancer care.

Transaction and partnership activity is likely to remain robust, as public companies, private equity platforms, and health systems pursue acquisitions, affiliations, and joint ventures to achieve scale, improve operational efficiency, and enhance access to clinical trials. Collaborations with academic centers and Centers of Excellence will increasingly support research integration, clinical innovation, and adoption of cutting-edge therapies. We anticipate the next wave of consolidation will prioritize technology-enabled platforms, integrated care delivery, and AI-driven solutions that optimize patient engagement, streamline workflows, and improve outcomes across multi-state networks.

Read our companion guide to this industry outlook here.

Landon Forsythe materially contributed to this report.

- “U.S. Oncology Market Size, Share, Trends & Growth Forecast Report Segmented by Therapy (Chemotherapy, Targeted Therapy, Immunotherapy), Indication, Distribution Channel and Country – Industry Analysis From 2025 to 2033,” Market Data Forecast, October 2025.

- American Cancer Society, “Cancer Facts & Figures 2025,” January 16, 2025.

- “Office of Cancer Survivorship, Statistics and Graphs,” National Cancer Institute.

- Kyoji Tsuchikama, Yasuaki Anami, et al., “Exploring the next generation of antibody–drug conjugates,” Nature Reviews Clinical Oncology, January 8, 2024.

- Ibid.

- Patricia Giglio & Amanda Micklus, “Biopharma dealmaking in 2024,” Nature Reviews Drug Discovery, January 15, 2025.

- J.P. Morgan, “2024 Biopharma Industry Insights: Investment Trends, M&A Activity, and Market Dynamics,” January 2025.

- Markus Gores, William Harries, “Biopharma M&A outlook for 2024,” IQVIA, January 12, 2024.

- “Overview of the 340B Drug Discount Program,” Congress.gov, January 27, 2026. https://www.congress.gov/crs-product/IF12232

- Jessica Chang and Yanya Natwick, “Drug administration shifted toward outpatient departments, especially to 340B hospitals,” Health Care Cost Institute, October 23, 2025.

- “Growth in the 340B Drug Pricing Program,” Congressional Budget Office, September 2025.

- American Association for Cancer Research, “Reducing the Risk of Cancer Development,” AACR Cancer Progress Report 2025.

- “Cigarette Smoking Rate in U.S. Ties 80-Year Low,” Gallup, August 13, 2024.

- “Obesity Rate Declining in U.S.,” Gallup, October 28, 2025.

- “Researchers describe cancer trends in people under 50,” NIH Research Matters, May 20, 2025.

- Brenner DR, Ruan Y, Carbonell C., “Potential Impact of Next-Generation Weight Loss Drugs on Cancer Incidence,” JAMA Network Open, September 8, 2025.

- “The Demographic Outlook: 2025 to 2055,” Congressional Budget Office, January 13, 2025.

- NCI Press Release, “Incidence rates of some cancer types have risen in people under age 50,” National Cancer Institute, May 8, 2025.

- William L. Dahut, MD, “What You Should Know About the Latest Cancer Trends and How to Reduce Your Risk,” American Cancer Society, January 30, 2025.

- Hannah Musick, “2025 US Cancer Disparities Report Highlights Education, Rural Gaps,” Journal of Clinical Pathways, January 12, 2026.

- “Global Oncology Trends 2025 Adopting new therapies as modalities shift and expenditures rise,” IQVIA, May 22, 2025.

- “Global Oncology Trends 2022 Outlook to 2026,” IQVIA, May 26, 2022.

- Ibid.

- Robin Mantell, “Reviewing the Past 5 Years in Oncology – What’s Next?,” Mantell Associates Market Insights, 2024.

- Rachel Henke, Juan Castro, et al., “The Enhancing Oncology Model: First Annual Evaluation Report,” August 2025.

- “Workforce Projections,” HRSA Data Warehouse.

- Laura Medford-Davis, Rupal Malani, et al., “How to attract and retain physicians in a challenging labor market,” McKinsey Healthcare Blog, September 10, 2024.

- Andis Robeznieks, “Single source of pay becoming less common for physicians,” AMA Research, October 17, 2022.

- Chris Harrop, “Half of medical groups tie physician compensation to quality measures in 2024,” MGMA Stat, April 17, 2024.

- Jessica MacIntyre, “As Advanced Practice Roles Expand in Oncology, Here’s How ONS Supports Their Significant Impact,” September 2, 2024.

- Ariana Pelosci, “How Can Oncology Staffing Shortages Be Remedied?” November 4, 2025.

- American College of Surgeons, “NCDB Quality Measure Improvements Announced,” July 17, 2025.

- Mandi L. Pratt-Chapman, PhD, MA, OPN-CG; Gabrielle Rocque, MD; et al., “The Centers for Medicare & Medicaid Services Will Pay for Patient Navigation—Now What?” February 2, 2024.

- American Association for Cancer Research, “AACR Project GENIE®: Powering Precision Medicine.”

- City of Hope, “City of Hope Completes Strategic Acquisition of Cancer Treatment Centers of America, Building a National, Integrated Cancer Research and Treatment System With a Singular Focus on Eradicating Cancer,” February 2, 2022.

- Cencora, “TPG and AmerisourceBergen to Acquire Leading Specialty Practice Network OneOncology From General Atlantic,” April 20, 2023.

- Cencora, “TPG and AmerisourceBergen Announce Completion of Acquisition of OneOncology,” June 9, 2023.

- Cencora, “Cencora Accelerates OneOncology Acquisition, Extending Solutions Offering for Community Oncology,” December 15, 2025.

- American Oncology Network, “American Oncology Network and Digital Transformation Opportunities Corp. Announce Completion of Business Combination,” September 20, 2023.

- Cardinal Health, “Cardinal Health completes acquisition of Integrated Oncology Network,” December 3, 2024.

- McKesson, “McKesson Corporation Completes Acquisition of Core Ventures,” June 3, 2025.

- Practices typically join The US Oncology Network through a variety of arrangements, including acquisitions, affiliation agreements, and management services agreements.

- American Oncology Network, “About AON,” 2024.

- American Oncology Network, “American Oncology Network Reports Strong Growth and Record Milestones in 2025,” August 12, 2025.

- The US Oncology Network, The US Oncology Network in The News, “Regional Cancer Care Associates Joins The US Oncology Network,” April 6, 2023.

- The US Oncology Network, The US Oncology Network in The News, “The US Oncology Network Further Expands Its Nashville, Tennessee Footprint and Research Expertise with the Addition of SCRI Oncology Partners,” December 2023.

- Florida Cancer Specialists & Research Institute, “Carrum Health and Florida Cancer Specialists & Research Institute Partner on Breast Cancer Treatment Model,” December 22, 2023.

- McKesson, “The US Oncology Network Expands its Tennessee Service Area as Tennessee Cancer Specialists Joins The Network,” August 2024.

- McKesson, “The US Oncology Network Extends its Reach in Illinois as Illinois CancerCare Joins The Network,” September 3, 2024.

- Florida Cancer Specialists & Research Institute, “Florida Cancer Specialists & Research Institute Launches Partnership with Paradigm Health, Inc. to Expand Patient Access to Lifesaving Clinical Trials,” September 3, 2024.

- OneOncology, “Navigating Cancer Accelerates Investments to Enhance Care Management Platform for Providers and Patients,” September 3, 2024.

- OneOncology, “OneOncology Closes Acquisition of United Urology Group,” October 14, 2024.

- OneOncology, “START and OneOncology Partner To Expand Access to Early Phase Oncology Trials,” May 27, 2025.

- OneOncology, “OneOncology Expands in Florida by Acquiring GenesisCare, Will Relaunch as SunState Medical Specialists,” October 8, 2025.

- Dana-Farber Cancer Institute, “About the Dana-Farber Beth Israel Deaconess Cancer Collaboration.”

- Harvard Medical Faculty Physicians, “Following state and city approvals, new cancer hospital and clinical collaboration enters next phase,” July 7, 2025.

- Dana-Farber Cancer Institute, “About Our Future Cancer Hospital,” 2025.

- Cancer AI Alliance, “Cancer AI Alliance unveils first collaborative AI platform for cancer research,” October 1, 2025.

- MD Anderson Newsroom, “UT MD Anderson and Texas Children’s Hospital Announce Joint Venture to End Childhood Cancer,” February 19, 2025.

- Kinder Children’s Cancer Center, “Kinder Children’s Cancer Center, a joint venture of UT MD Anderson and Texas Children’s, is a transformational alliance with one mission: to end childhood cancer,” 2025.

- Scope Research. We note that the data presented has been sourced from a single transaction database and is not meant to represent total oncology transaction volume but serve as a proxy for the distribution of EBITDA multiples. Many oncology transactions are private and may not be publicly disclosed.

- Cencora, “TPG and AmerisourceBergen to Acquire Leading Specialty Practice Network OneOncology From General Atlantic,” April 20, 2023.