中文

中文

Overall M&A activity and private equity deal flow has continued to be relatively soft thus far in 2012, and the IPO market remains difficult as an exit vehicle for both PE portfolio companies and other private businesses. These factors, combined with the historically low interest rate environment and the return to life of the leveraged financing markets, have led to a recent surge in leveraged dividend recapitalization transactions – more commonly known as “dividend recaps”. Moreover, pending changes to the capital gains tax laws at the beginning of 2013 suggest that dividend recaps are likely to continue to be a popular means for companies to deliver returns to their shareholders in the latter half of 2012.

Overview

Dividend recaps result from using borrowed money to issue a special dividend to a company’s shareholders. In recent years, these transactions have been most often associated with private equity-backed companies, as PE funds have used the dividend recap as a way to extract capital from portfolio companies in lieu of more traditional exit scenarios such as an IPO or M&A transaction. PE funds benefit from dividend recaps in a number of ways, including an acceleration of the fund’s internal rate of return on an investment; as a means to achieve partial liquidity for the fund’s investment without losing control or the ability to capture the benefit of the company’s future sales and earnings growth; and the cash flow savings from the “tax shield” attributable to the tax deductibility of interest payments on the newly issued debt. However, dividend recap deals are not the exclusive domain of private equity sponsors, as well-capitalized publicly traded companies may also seek to exploit borrower-friendly capital markets for a leveraged, one-time dividend or stock buyback transaction. To wit, Domino’s Pizza, Inc. (NYSE:DPZ) declared a $3 special dividend earlier this year that was financed by a $1.675 billion asset-backed securitized debt facility.

As in the case of Domino’s, dividend recaps are often financed through leveraged loans, which are corporate debt instruments arranged by one or more investment banks and syndicated to a group of financial institutions that typically include commercial banks and other, non-bank investors. Starting with the leveraged buyout (“LBO”) boom of the 1980s, the leveraged/syndicated loan market has become the most prominent way for corporate borrowers (issuers) to tap banks and other institutional capital providers for debt financing. Although there is no commonly accepted definition in this market of what constitutes a “leveraged” loan, the most common description is that of a loan to a company whose credit rating – including the impact of the new borrowings – is speculative grade (i.e., rated BB or lower by the major debt rating agencies), and who is paying a spread (i.e., a premium above LIBOR or some other base rate such as U.S. Treasury yields) sufficient to attract the interest of non-bank term loan investors such as finance companies, CLOs, and mutual funds that may participate in the ultimate loan syndication.

Leveraged lending has surged thus far in 2012 for all types of debt issuances (M&A deals, LBOs, refinancings, capital projects, etc.), and has spurred a corresponding increase in dividend recap activity. Granted, the first half of 2011 saw similar activity in the leveraged lending market, only to see the bottom drop out of the market in the second half of the year. However, the increase in leveraged lending and dividend recap activity in 2012 is expected to be more enduring and is a function of a number of factors, discussed in greater detail below, that many observers believe will compel companies to return capital to their shareholders before the end of the year.

While dividend recaps do confer substantial benefits on shareholders and financial sponsors, they are certainly not without risk for the company, its shareholders, and its board of directors. At the extreme, debt-funded dividends that are too large relative to a company’s earnings and available capital (post-transaction) may leave it without the ability to adequately fund day-to-day working capital needs and may impair future growth opportunities or the ability to respond to and weather unanticipated business downturns. Moreover, the directors of a business that is found to have engaged in “constructive fraud” that left a business insolvent as a result of the recap transaction could face significant personal liability. The shareholders that benefited from the recap could also be forced to return their proceeds from the deal if it is ultimately unwound by the courts. One way in which board members (and, by proxy, the shareholders) can shield themselves from these risks is by engaging a qualified, independent financial advisor to provide a “solvency opinion” on a proposed recap transaction. These risks, and the use of a solvency opinion to help address them, are also discussed in further detail below.

Drivers of Dividend Recap Activity

Leveraged Loan Volume and Leverage Multiples

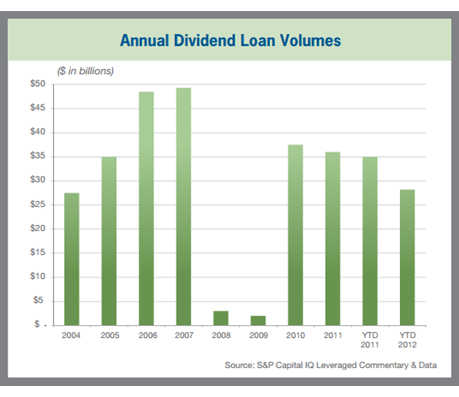

According to Standard & Poor’s Leveraged Commentary & Data, dividend-driven leveraged loan volume, which was virtually non-existent in the two years following the start of the financial crisis in early 2008, has exceeded $28 billion in the year-to-date period through July 2012. This amount is down from $35 billion in the same period of 2011, but is still on pace to exceed the all-time annual high of $49.3 billion set in 2007, before the onset of the financial crisis.

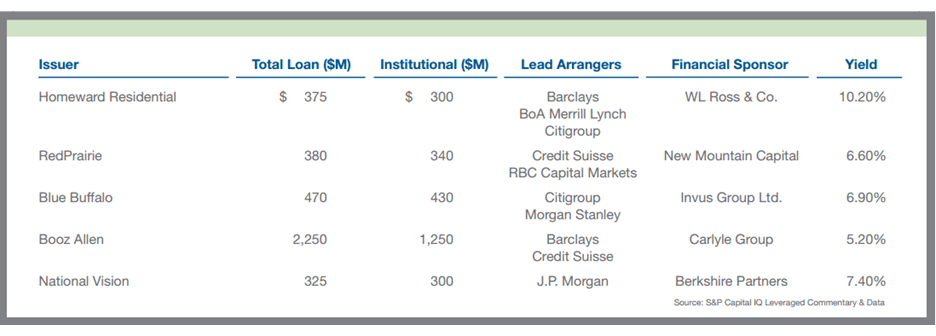

Moreover, 2012 has been the “year of the dividend” thus far for private equity firms. According to Standard & Poor’s, of the total amount raised so far this year in the leveraged loan market, approximately 48% has gone to finance dividends to shareholders of companies that are controlled by private equity firms, which is well above the historical average. Also, nearly 40% of the total private equity capital flows thus far in 2012 (both in and out of companies) has been out of issuers via dividends, which exceeds the previous high of 33% set in 2010. Below is a list of private-equity-sponsored dividend recap deals that were launched in the leveraged loan market in July of 2012, including a few pertinent details of each deal as of August 2012.

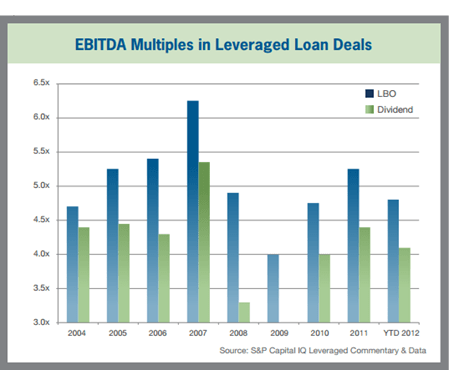

In addition, although they are down from the boom levels of 2006/2007, leverage multiples are up significantly from their nadir in 2008 and 2009. As shown on the following page, lenders typically take a more cautious approach to dividend recap deals than traditional LBO deals, as LBO deals are accompanied by an equity capital commitment from the sponsor, where recap deals extract equity from the portfolio company. As a result, the average pro forma debt multiple of 2012 dividend deals of approximately 4.0x earnings before interest, taxes, depreciation, and amortization (EBITDA) is below the average of 4.8x EBITDA for large corporate LBO deals. Nonetheless, there is a view among private equity firms that LBO transactions completed in the first few years after the financial crisis, when credit was constrained, required too much equity from the financial sponsor, and thus there is room to increase leverage in capital structures. For instance, as a result of dividend recaps, Getty Images, Inc., SeaWorld Parks & Entertainment, Inc., and Thermadyne Holdings Corporation, which were all acquired in LBO transactions from 2008-2011, were all able to increase financial leverage by at least one turn relative to the level of debt available when they were purchased.1

Moreover, corporate borrowers have become less risky in recent years as the economy has slowly recovered. According to Standard & Poor’s, the percentage of issuers in the high-yield corporate bond market (which is similar to but is separate and distinct from the leveraged loan market in that loans are not underwritten, arranged, and held by banks and other institutional capital providers, but rather borrowers go straight to the capital markets for funding) that have defaulted on their debt in the last year currently stands at around 3.0%, which is well below the historical average in this market of 4.5% to 5.0%. This decrease undoubtedly reflects, in part, an increase in the quality of the borrowers and a decline in average leverage ratios for new issuers (relative to the boom-period peak of 2006/2007), but it also is indicative of an overall improvement in corporate financial performance.

Interest Rates

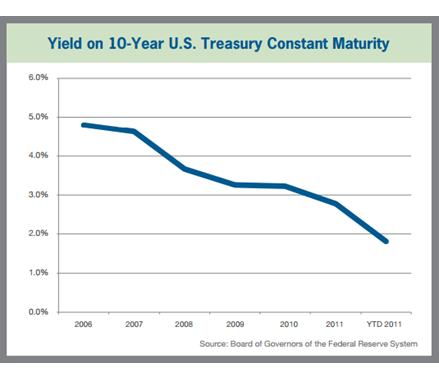

In addition, the recent surge in leveraged loan activity reflects the incredibly low interest-rate environment for corporate borrowers that has persisted since the financial crisis began in 2008. U.S. government Treasury bonds are the benchmark that financial institutions use for pricing leveraged loans to corporate borrowers. These institutions will, of course, receive a higher interest rate for underwriting these types of loans due to the higher default risk associated with leveraged loans. This premium is typically in the form of a “spread” (which often starts at 200 basis points) over the prevailing Treasury rate. However, since interest rates on government bonds are so low – the yield on the 10-year Treasury is currently less than 2.0% – companies do not have to pay nearly as much on these loans relative to other, higher-interest environments that have prevailed in the past.

In addition to the extremely low borrowing costs available in the leveraged loan market, the high-yield corporate bond market is currently being spurred by investors of all kinds – including mutual funds, pension plans, hedge funds, and wealthy individuals – that are desperately seeking yield for the fixed income portion of their portfolio. This creates additional demand for these types of assets, which has served to create a sort of “feedback loop” that continues to drive interest rates even lower for high-quality (and even some lower-quality) corporate bond issuers. As of August 17th, the average yield to maturity on the SPDR Barclays Capital High Yield Bond ETF, which tracks the performance of the Barclays Capital High Yield Very Liquid Index2, was just 7.3%. This fund’s top holdings include a number of financial-sponsor backed businesses, including HCA, Inc. and Caesars Entertainment. Moreover, with the Federal Reserve formally on record as saying that it intends to keep interest rates near zero through at least 2014, the demand for higher-yielding corporate bonds as an alternative to U.S. Treasury securities is unlikely to abate anytime soon. Of course, there is a limit to how far the high-yield bond market can be stretched – some analysts are beginning to warn that the market is becoming overheated and there may even be a bubble forming. In addition, financing for dividend recap transactions has skewed toward the leveraged loan market in recent months, as private equity firms seek to preserve the option of accessing the IPO or M&A markets for future portfolio company liquidity events (which can be more difficult for companies that are encumbered by the non-call periods and high prepayment fees associated with high-yield bonds).

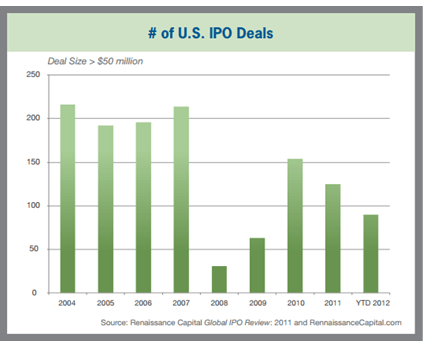

Lack of Alternative Exit Options

Private equity firms remain focused on generating liquidity for limited partners that have seen relatively few liquidity events since the beginning of the financial crisis. Both IPO markets and M&A markets remain relatively stagnant in the current, uncertain economic environment. According to Standard & Poor’s, there have been only 14 IPOs of PE-backed companies thus far in 2012, and 29 sponsor-to-sponsor M&A transactions. On the other hand, there have been 44 dividend recap deals through which the financial sponsors have recouped approximately two-thirds of their original capital commitment to the business, on average. In concert with the increased availability of financial leverage and the extremely low interest-rate environment, the lack of other exit alternatives suggests that dividend recaps remain a viable alternative for financial sponsors who may be seeking to take advantage of the favorable market conditions and return some, or all, of their investment in a business to their limited partners.

Tax Law Changes

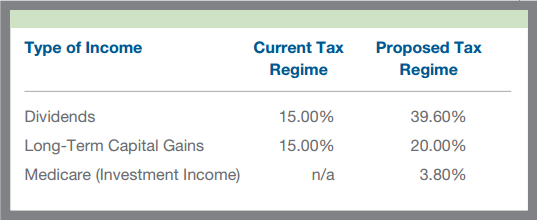

The “Bush-era” tax cuts are currently set to expire at the end of 2012. If Congress and the President take no prior action to extend the tax cuts (or make them permanent or replace them with an alternative tax regime), the marginal tax rate applicable to individual taxpayers on dividend income from corporations will increase from the current level of 15% to 39.6%. In addition, the tax rate that individuals pay on long-term capital gains income is set to rise from 15% to 20%. Finally, the already enacted tax increases under the 2010 healthcare reform act (the Affordable Care Act) are scheduled to come on line in 2013. One of the increases included in this Act is a new 3.8% additional Medicare tax imposed on the investment income of individuals earning more than $200,000, and couples earning more than $250,000. As a result, for these taxpayers, the effective capital gains tax rate will increase to nearly 24%.

These tax increases may motivate some financial sponsors, as well as certain publicly traded (and, theoretically, even some closely held) businesses to consider leveraging their balance sheets to pay a special or one-time dividend to shareholders (in addition to any regular dividends they may already be paying) before the end of the year. The purpose, of course, would be to both take advantage of the much lower dividend tax rate under the existing tax regime, as well as to decrease future capital gains that would be taxed at a higher rate under the pending regime.

Risks and Mitigating Factors

Corporate Insolvency Law

Corporate and bankruptcy law addresses in several ways the risk that a dividend recap transaction will leave a company insolvent. For instance, Delaware law addresses this risk by requiring that corporations only pay dividends to their shareholders from a capital “surplus,” which is defined as: 1) the fair value of a corporation’s total assets less its stated liabilities, less 2) the corporation’s stated capital (which is generally defined as the aggregate par value of the company’s stock). Under Delaware law, directors of companies that consent to a dividend recap without exercising due care to ensure that the dividend is being paid from the company’s surplus could be subject to breach of fiduciary duty and other legal claims arising from the transaction.

In addition, if a company’s financial performance deteriorates post-transaction to the point of insolvency, the dividend recap could be “set aside” under the fraudulent conveyance provisions of the Federal Bankruptcy Code as well as general state laws (e.g., the Uniform Fraudulent Conveyance Act). These laws cover not only intentional fraud by a borrower that is intended to financially benefit secured creditors or shareholders at the expense of unsecured creditors, but also “constructive” fraud. The Federal Bankruptcy Code defines constructive fraud as occurring when a debtor either: 1) was insolvent on the date the transfer was made or becomes insolvent as a result of the transfer; 2) was left with unreasonably small assets or capital as a result of the transfer; or 3) made the transfer with the intent to incur (or reasonably should have believed that it would incur) debts beyond its ability to repay them. As previously mentioned, the penalties and consequences for directors, secured creditors, and/or shareholders of companies that have been found to have engaged in fraudulent transactions, regardless of whether there was any actual mal intent on behalf of the parties to the transaction, can be severe, and can include judgments against a director’s personal assets, as well as the renunciation of transaction proceeds in favor of the unsecured creditors that were found to have been harmed by the deal.

Solvency Opinions

To address these risks, companies and their directors often choose to engage a financial advisor to prepare a solvency opinion, which is an analysis of whether a company will remain solvent in consideration of, and taking into account, the debt incurred to finance a leveraged transaction. Most solvency opinions apply three financial tests to assess a subject company’s solvency: 1) the Balance Sheet Test, 2) the Cash Flow Test, and 3) the Reasonable Capital Test. While an in-depth discussion of each of these tests is beyond the scope of this article, each of them is intended to address the following factors that affect solvency:

- Whether or not the fair value of a company’s assets exceeds its liabilities (including stated liabilities and identified contingent liabilities)

- Whether or not the company should be able to satisfy its debt obligations – related to existing debt as well as any new debt incurred as a result of the transaction – as those debts mature

- Whether or not the company should have a reasonable level of surplus capital following a leveraged transaction to provide downside protection in the case of deteriorating business conditions

Although a solvency opinion performed in connection with a highly leveraged transaction cannot in and of itself ensure that the business will not ultimately become financially distressed in the future, or even enter bankruptcy, it can assist corporate directors in carrying out their fiduciary duties to a company’s stakeholders in connection with the transaction (which, in the case of a dividend recapitalization or share buyback, can reasonably be interpreted to include a company’s unsecured creditors in addition to its shareholders). Moreover, a solvency opinion can help shift the burden of proof to the plaintiffs in any subsequent action alleging breach of fiduciary duty or fraudulent conveyance against the company, its management, or its directors.

Conclusion

Current market and regulatory conditions appear to be creating a “perfect storm” in the latter part of 2012 for highly leveraged dividend recapitalization and stock buyback transactions by both financial sponsors and well-capitalized publicly traded companies. Although the capital markets are difficult to predict with any certainty – take, for example, the experience of 2011, which saw record levels of leveraged loan activity in the first half of the year, followed by a precipitous drop-off in the second half of the year – all signs point to “go” for a surge in activity in these types of transactions toward the end of the year. Dividend recap transactions can have significant benefits for both companies and financial sponsors, but are not without their risks. However, a well-prepared solvency opinion performed by a qualified, independent financial advisor can help to mitigate these risks and ensure a successful transaction for all involved.

___

1 Source: Moody’s Investors’s Service

2 The Barclays Capital High Yield Very Liquid Index includes publicly issued U.S. dollar denominated, non-investment grade, fixed-rate, taxable corporate bonds that have a remaining maturity of at least one year, are rated high-yield (Ba1/BB+/BB+ or below) using the middle rating of Moody’s, S&P, and Fitch, respectively, and have $600 million or more of outstanding face value.