中文

中文

On January 3, 2026, U.S. forces captured President Nicolás Maduro, ending his 2013–2026 tenure and triggering an externally managed transition centered on oil leverage.1 Venezuela’s political transition has reopened a familiar narrative in energy markets, considering factors such as:

- The world’s largest proven oil reserves

- Years of underinvestment

- The possibility of rapid production growth once politics get out of the way

For energy companies and investors, however, the more relevant question is not whether Venezuela could produce more oil, but under what economic conditions will meaningful U.S. capital will return?

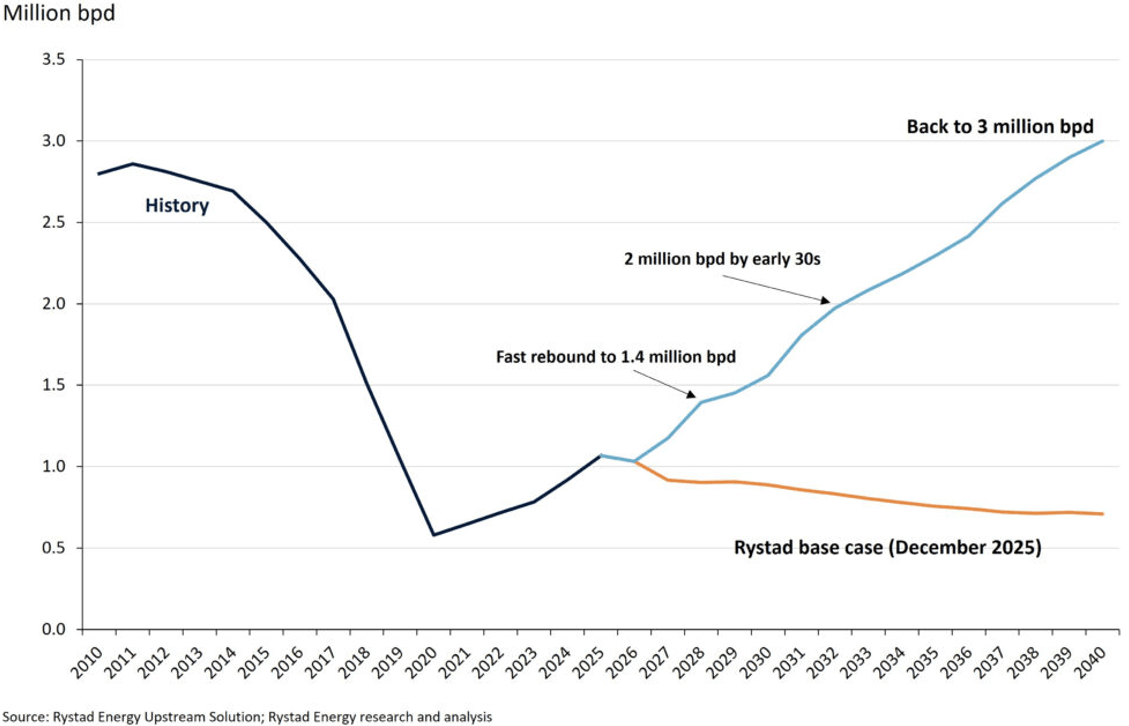

The Scale of the Reset

At its peak in the late 1990s to the early 2000s, Venezuela produced more than 3.4 million barrels per day.2 Today, output remains a fraction of that level,3 constrained by:

- Degraded infrastructure

- Workforce attrition

- Sanctions

- Years of capital flight

Reversing this decline will requires significant new investment across Venezuela’s energy value chain. Industry estimates consistently suggest that restoring production to levels that would materially affect global supply would require billions of dollars per year for a decade or more.

Rystad Energy, an independent energy research and business intelligence company headquartered in Oslo, Norway, recently modeled several scenarios4 for Venezuela and has estimated the capital costs required for each:

| Scenario | Production Level | Timeline | Estimated Capital Required |

|---|---|---|---|

| Maintain Current Output | ~1.1 million barrels/day | 2026–2040 | ~$53 billion |

| Moderate Recovery | ~2.0 million barrels/day | By ~2032 | Part of ~$183 billion total |

| Full Capacity Restoration | ~3.0 million barrels/day | By ~2040 | ~$183 billion |

The same article provided this graphic of the different expected outcomes for Venezuela with different levels of new capital investment.

However, echoing the sentiments of numerous oil company executives, the capital required to rebuild Venezuela’s oil infrastructure and increase its production will not arrive on political optimism alone.

Political Goals Meet Oil Pricing Reality

WTI prices are currently about $60 per barrel, Brent crude has a modest ~4.50 per barrel premium, and a relatively flat NYMEX futures curve all indicate that oil demand is being met with current production. The resulting lack of a clear business case supporting future investment in Venezuela is why ExxonMobil CEO Darren Woods said, “If we look at the legal and commercial constructs and frameworks in place in Venezuela today — today, it’s uninvestable.”5

This macro backdrop matters because Venezuela’s oil is harder to develop than other forms of crude oil, like from the Permian basin, which is some of the lightest and cleanest crude in the world. Venezuela’s resource base is dominated by heavy and extra-heavy crude, particularly in the Orinoco Belt.6 These projects are capital-intensive, operationally complex, and structurally discounted to benchmark prices due to blending requirements, transportation costs, and refining constraints.

Breakevens Drive Behavior, Not Rhetoric

For energy industry decision makers, breakeven economics are unforgiving. Consensus estimates place the breakeven price for drilling and completing a new well in the United States above $60 per barrel.7 Venezuelan projects, with higher political risk, infrastructure decay, and security costs, require even stronger economics to compete for capital.

The Trump Administration publicly has stated the President’s desire for:

- More oil production8

- Driving down oil prices

- Reducing gasoline prices

- Reducing inflation in almost every product sold

However, energy industry leaders are tasked with preserving capital and delivering risk-adjusted rates of return for their shareholders, not on advancing macro or geopolitical objectives.

Three Plausible Paths Forward

The U.S. has a three-step plan for Venezuela that will begin with stabilizing the country, ensuring U.S. oil companies have access to the country during a recovery phase, and finally overseeing a transition.9

Stabilization

The first phase focuses on stabilizing Venezuela’s political and economic situation to prevent chaos following Maduro’s removal. This includes securing essential functions of the state and ensuring order before deeper changes begin to avoid a collapse or power vacuum after the Maduro regime’s disruption.10

Recovery

The second phase aims at economic recovery and rebuilding institutions. This stage would facilitate access for U.S. companies and others to Venezuela’s oil and other markets in a fair, transparent way and begin reconciliation processes within the country. It also includes efforts to rebuild civil society and reintegrate political actors, including the release or amnesty of political prisoners.11

Transition

The final phase intends to oversee a political transition, ultimately returning governance to a legitimate Venezuelan authority through democratic processes. U.S. Secretary of State Marco Rubio described this as creating conditions for a long-term transition beyond emergency stabilization and recovery.12

Next Steps for Restoring Venezuela’s Production

Venezuelan Improvements to its Oil Regulations

Venezuela’s National Assembly has backed new hydrocarbons legislation to open the sector to foreign and private investment, reduce royalties in some cases, and introduce international arbitration, which is a major structural shift from decades of state control.13

Investor Interest / Adequate Returns?

Major oilfield services companies like SLB are positioning to expand operations in Venezuela, signaling some optimism about long-term reconstruction opportunities. The bottom line is that institutional legitimacy, legal guarantees for investors, and U.S. sanctions policy are considered necessary to support rebuilding, and stable governance of Venezuela needs to be evident before meaningful capital returns.14

Global Competition for New Capital

As noted above, the required investments to restore Venezuelan production levels is massive. At the same time, significant investments are being rationalized for AI data centers in the U.S., increased generating facilities and related electrical infrastructure buildout. Absent higher prices or lower costs, U.S. energy leaders will be hesitant to invest in Venezuela absent other incentives.

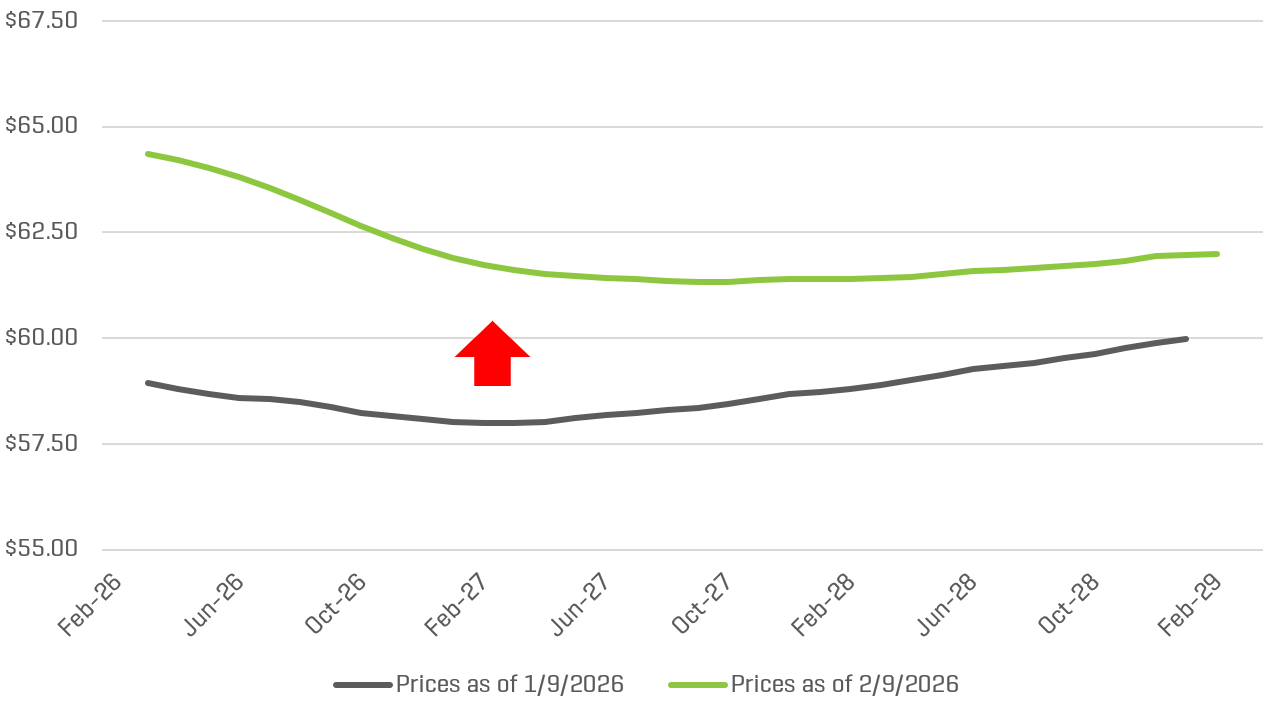

WTI Strip Prices Increase

In addition to the recent turmoil in Venezuela, tensions are escalating with Iran, and Russia‑Ukraine peace prospects have deteriorated again, creating a combination of global factors all driving oil prices up (or preventing them from falling further).

Spot prices and futures prices for the West Texas Intermediate (WTI) contract increased approximately $5.50 per barrel in the near term and increased approximately $2.00 over the longer term.

As shown, the oil price curve has shifted to a state of “backwardation,” reflecting the market’s expectation of lower future spot prices over the longer term.

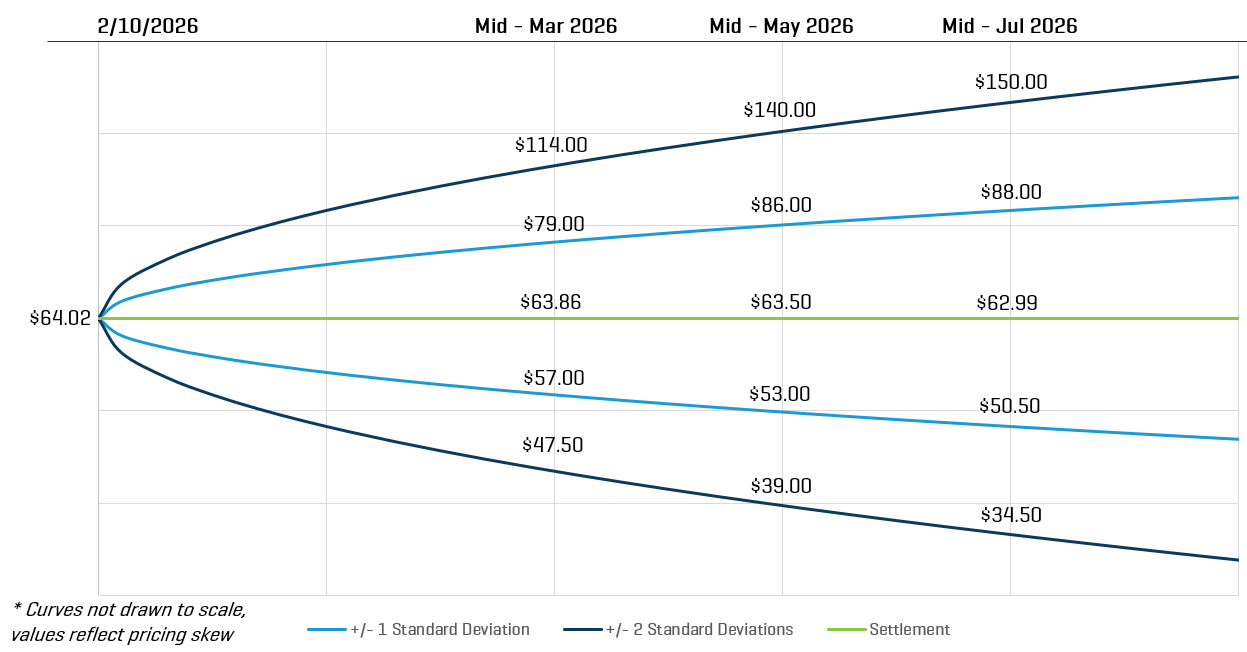

Oil Price Outlook

The price distribution below shows the crude oil spot price on February 10, 2026, as well as the predicted crude oil prices based on options and futures markets. Light blue lines are within one standard deviation (σ) of the mean, and dark blue lines are within two standard deviations.

WTI Crude Oil $/BBL

Based on these current prices, the markets indicate there is a 68% chance oil prices will range from $53.00 and $86.00 per barrel in mid-May 2026. Likewise, there is roughly a 95% chance that prices will be between $39.00 and $140.00. By mid-July 2026, the one-standard deviation (1σ) price range is $50.50 to $88.00 per barrel, and the two-standard deviation (2σ) range is $34.50 to $150.00 per barrel.

Insights

Remember that while option prices and models reflect expected probabilities rather than certain outcomes, they still remain a useful tool for assessing market expectations and risk. Throughout most of 2023 and 2024, crude oil spot prices generally fluctuated within the range of $70 to $90 per barrel. During that period, we observed general increases in futures price volatilities as prices approached the upper and lower bounds of that range. In 2025, crude oil spot prices generally decreased throughout the year. For mid-July 2026 pricing as of February 10, 2026, the 1σ range had a spread of $37.50 per barrel, and the 2σ range had a spread of $115.50 per barrel, indicating a general increase in spreads compared to recent months. This increase coincided with heightened geopolitical uncertainty, including the recent turmoil in Venezuela, escalating tensions with Iran, and the deterioration of Russia‑Ukraine peace prospects.

- Simon Lewis and Patricia Zengerle, “Rubio says US plan for Venezuela is stability, recovery, then transition,” Reuters, January 7, 2026.

- “Venezuela Oil Production,” YCharts, webpage.

- “Venezuela: Oil Production of 930,000 Barrels Per Day Despite 300 Billion in Reserves,” Energy News.

- Camille Rustici, “Venezuela Oil & Gas: Reserves, Infrastructure Challenges, and the Road to Recovery,” Direct Industry, January 12, 2026.

- “Our perspective regarding the situation in Venezuela as shared with President Trump,” ExxonMobil, news release, January 9, 2026.

- U.S. Energy Information Administration, Venezuela Country Analysis.

- Greg Scheig, “Oil Prices Hover Near Drilling Breakeven Price,” August 12, 2025.

- Christian K. Caruzo, “Trump Says U.S. Companies Will Start Drilling Venezuelan Oil ‘Very Soon,’” Breitbart, January 23, 2026.

- Simon Lewis and Patricia Zengerle, “Rubio says US plan for Venezuela is stability, recovery, then transition,” Reuters, January 7, 2026.

- “Stability, recovery and transition: US lays out three-phase plan for Venezuela after seizure of Maduro,” Firstpost, January 7, 2026.

- Ibid.

- Ibid.

- Joe Daniels, Jamie Smyth, and Ana Rodríguez Brazón, “Venezuela’s lawmakers back oil sector reforms,” Financial Times, January 22, 2026.

- Kit Norton, “S&P 500 Oilfield Service Giant SLB Beats Earnings. ‘We Are Ready’ For Venezuela,” Investor’s Business Daily, January 23, 2026.