Italiano

Italiano

Recently, the equity structures of public companies have become more complex with the prevalence of super-voting stock and other unbalanced class structures that allow for control to reside within certain investor groups, such as company founders or their families. In the latest wave of technology company IPOs, super-voting stock has been present in the equity class structures of Facebook, Groupon, LinkedIn, and Zynga.

In April 2012, Google announced a proposal to create a new class of nonvoting stock by affecting a stock split. This change would allow the company to manage the dilutive impact of additional equity issuances in financing stock-based acquisition transactions and to fund employee equity incentive programs. Furthermore, the proposed structure would allow the co-founders of the company the ability to maintain their current level of control. The proposed structure will result in three classes of stock: (i) Class A voting stock, which has one vote per share and will continue to trade under the “GOOG” symbol; (ii) Class B super-voting stock, which has ten votes per share and is currently controlled by Google’s co-founders; and (iii) Class C nonvoting stock, which will have similar rights as the Class A stockholders, but no right to vote and will be traded under a different ticker symbol. Not surprisingly, Google’s two co-founders had enough voting power to unilaterally approve the proposal without the affirmative vote of any other stockholder. In June 2012, the proposal was approved. However, the stock split and creation of the new class of nonvoting stock is not likely to be effectuated until later in the year due to shareholder lawsuits seeking to block the move.

Dual Class Structures

As valuation analysts, our assignments often require us to consider value differentials between voting and nonvoting stock of closely held companies when a dual class structure is present. Naturally, we look to market evidence to facilitate this analysis. Typically, voting and nonvoting stock have identical economic attributes, with the exception of the ability to vote. For public companies, the benefits of dual class voting structures allow founding shareholders and a company’s management team to maintain the freedom to focus on long-term goals and a company’s strategic direction, rather than contending with the threat of a hostile takeover, or influence exerted by shareholders that are more concerned with short-term goals, such as quarterly earnings targets. One detriment, however, is that some investors may not invest in companies with multiple vote share structures as a matter of preference or internal policy, thus diminishing the investor pool.

The Agency Problem

Various studies have been performed analyzing the economic impact associated with separation of ownership and control and the agency problem created between managers and shareholders. One such study analyzed publicly traded companies with dual class structures noting that when a significant divergence was present between insider voting rights and cash flow rights, agency conflicts were more prevalent.1 Insiders were more prone to waste corporate resources to pursue private benefits at the expense of shareholders through activities such as empire building, excessive compensation and perquisites, or subsidizing unprofitable projects or divisions.

Discount for Lack of Voting Rights

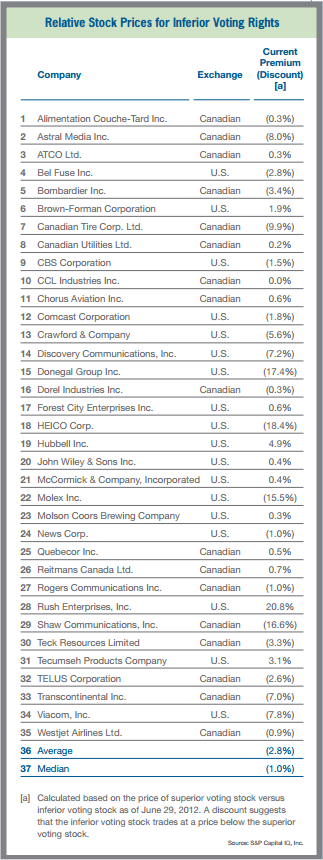

In addition, numerous studies have been performed to quantify the price differentials observed between voting and nonvoting stock of publicly traded companies. As outlined in the above table, the results indicate that the price differential is relatively minimal, with most observations falling in the 3% to 5% range.

Federal Tax Court Cases

Prior Tax Court cases whereby the issue of a voting premium or nonvoting discount was highlighted can also provide some insight. As indicated in the adjacent table, the courts generally have allowed discounts ranging from 0% to 5% for nonvoting stock, consistent with the market studies previously discussed.

The Simplot case is perhaps one of the most controversial cases on the subject of the valuation of voting versus nonvoting stock. This case offers a great example of the different methodology utilized by the opposing experts and the disparate values that resulted. Although the subject interest was a minority interest in the Class A voting shares, the IRS expert attributed control of the company to this block of stock. As a result, the Tax Court concluded that it was appropriate to allocate 3% of the value of the entire enterprise across a very small number of Class A shares. The result was that the Class A voting shares were valued at a 6,000% premium to the Class B nonvoting shares, well in excess of the value a controlling shareholder could possibly achieve in a sale of the company. This disparity resulted in an appeal.

The Ninth Circuit Court of Appeals reversed the Tax Court decision in favor of the taxpayer noting that “…the Tax Court valued an asset not before it – all the Class A stock representing complete control. There was no basis for supposing whatever value attached to complete control a proportionate share of that value attached to each fraction of the whole…”. Also noteworthy in the appellate court’s opinion was that a premium should be applied only if the economic advantage could be demonstrated. The IRS expert’s arguments were devoted to speculation as to what might happen after the valuation date to improve the value of the shares through the possibility of increased dividends or a potential liquidity event. In the end, the Appeals Court determined that a minority interest in voting shares was worth no more than a minority interest in nonvoting shares in the instant case.

As demonstrated in Simplot, the concept of estimating the value difference between a small block of voting stock and a small block of nonvoting stock is often confused with the value differential resulting from maintaining a controlling interest in a business relative to a minority interest. The following chart illustrates the levels of value framework often considered in the valuation of a closely held business interest.

When applying valuation discounts or premiums, it is important to have a thorough understanding of the base value to which the adjustment is being applied. For example, to the extent an analysis is performed utilizing the pricing metrics of comparable public companies, the indication of value can cover the spectrum between a marketable, minority-interest value, and a financial control level of value depending on the facts and circumstances surrounding each public company and/or depending on the manner in which the subject company earnings metrics are applied. That is, if controlling adjustments were made to the subject company’s earnings (e.g., add-back of excessive officers’ compensation), a financial control level of value may result. Conversely, if the “as-is” subject company earnings are applied, a marketable, minority-interest level of value may result. In estimating the value of nonvoting stock in a closely held company, several adjustments may be required. These adjustments may include a discount for ack of control, a discount for lack of marketability, and consideration of a discount for lack of voting rights.

The Value of Control

While numerous factors are present, the key factor that contributes to the value of control is the ability of a controlling owner to change the status quo to generate higher cash flows. For example, a financial buyer of a well-run, industry-leading public company may be unable to make significant changes to that public company from a financial control perspective to increase its cash flows relative to the cash flows that would be received by its shareholders on a status-quo basis. Moreover, the minority shareholders in that public company may not be disadvantaged in any respect relative to a controlling buyer since minority shareholders generally have equal access to information, have certain legal protections, and are equal beneficiaries of the cash flows (relative to their ownership interest). Because of this, financial control and “as-is” cash flows may converge for well-run, efficient companies, and no discount for lack of control may be warranted. However, to the extent a company is poorly managed, and if “optimal” management could result in greater returns, a significant discount for lack of control may be applicable.

Furthermore, a minority shareholder in a private company may be significantly disadvantaged relative to a minority shareholder in a public company due to lack of public scrutiny and lack of SEC oversight. Abusive behavior by management can manifest by executives consuming excessive corporate resources and making highly risky strategic decisions. Lack of shareholder oversight and a deeply entrenched management team can add to the problem. Often in closely held companies, the majority shareholder controls the board. Absent a breach of fiduciary duty, it can be difficult to remove the directors and management team.

With a private company, the lack of a public market and inability to get liquidity for a minority position exacerbates the risk profile associated with holding the interest, particularly in the presence of an ownership structure where unilateral control exists with one person or family members with potentially widely divergent views as to the strategic direction of the company. Other factors warranting large discounts for lack of control include the presence of the following attributes.

- Excessive officers’ compensation and perquisites

- The utilization of an inefficient capital structure

- Inability to control the timing of a sale, acquisition, or divestiture

- Inability to control the timing of dividends/distributions

- Inability to prevent irrational acts

To the extent these factors are present, and a discount for lack of control is applied to account for these detriments, the incremental discount for lack of voting rights applicable to nonvoting stock may be negligible.

Factors Impacting Discount for Lack of Voting Rights

Concentration of Voting Ownership

In situations where there is little chance of changing management/control, the difference between voting and nonvoting shares is likely de minimis. That is, if unilateral control is maintained by one shareholder, then owning a small block of voting stock provides virtually no benefit relative to owning a nonvoting block. However, if the voting shares are widely dispersed, the probability of management change may be higher and it may be appropriate to reflect a premium to the voting shares. To the extent the potential for a “swing vote” is present which could result in unlocking measurable value (e.g., sale of the company) and this event is not merely speculative, a greater price differential may be warranted.

Poor Management

All else held constant, voting shares should trade at a greater premium to nonvoting shares at poorly managed companies relative to optimally managed companies. Since the impact associated with control is minimal in efficiently managed companies, voting shares and nonvoting shares should trade at approximately the same price. In a poorly managed company, the impact associated with control is likely higher, warranting a greater voting share premium.

Other Factors

It is important to compare and contrast the attributes of the subjects of the empirical data (i.e., publicly traded stock) with those of closely held business interests. Shareholders dissatisfied with the management of a public company are typically able to sell their investment and reinvest quickly due to the liquidity of the public markets. An investor in a privately held company does not have this liquidity benefit. Accordingly, an upward adjustment to the price differentials indicated by the public markets for voting and nonvoting stock may be warranted.

Conclusion

As demonstrated by the public markets, when firms create dual class share structures, the potential benefits from “superior” management of founding shareholders may be perceived to be greater than the potential detriment created by weaker management oversight. Over time, however, the costs imposed by a dual class structure may outweigh the potential benefits. That is, the management team viewed as superior at the time the dual class shares were issued may not live up to expectations. It will be interesting to see how the market responds in pricing Google’s equity classes, as well as other technology companies’ dual class stocks as management styles fall in and out of favor.

With closely held businesses, unbalanced corporate governance structures can allow founding shareholders or family controlled businesses to perpetuate a philosophy that does not have shareholder return maximization as the top priority. Each valuation exercise has a unique set of facts and circumstances. The key factors contributing to greater price differentials between minority interests in voting and nonvoting stock lie in the ability to influence greater shareholder returns and the likelihood that these events will materialize.

1 Masulis, Ronald W., Wang, Cong and Xie, Fei, Agency Problems at Dual-Class Companies. Journal of Finance, Volume 64: Issue 4, 1697-1727, August 2009.