Industrial Services Industry Update - Q2 2018

Subscribe to Industry UpdatesIndustrial Services Industry Update - Q2 2018

Subscribe to Industry UpdatesBroad Buyer Interest, Tax Reform, Strong Economic Conditions Underwrite Industrial Services M&A Activity

Industrial services M&A activity continued to bolster in the second quarter of 2018 and was fueled by strategic and private equity interest. An increasingly competitive market drove strategic buyer interest as they seek to expand market share, win larger projects, and diversify service offerings. Private equity has been on both sides of the transaction, as certain groups look to exit successful investments in a robust M&A environment, while others look to continue capitalizing on growth within niche service offerings. While share price performance came down from first-quarter highs, last-12-month (LTM) EBITDA margins and trading multiples remained constant. Industry growth remains optimistic as end markets, such as manufacturing, construction, and oil and gas, continue to recover, and in some cases thrive. Business investment and capital spending is expected to increase due to favorable financial conditions, recent tax reform, expanding global markets, and low capital costs. Additionally, economic pressures from regulatory organizations are placing increased emphasis on workplace safety and environmental violations, which will ultimately provide more opportunity for companies providing industrial services.

Key Takeaways

- Continued strong overall industrial services M&A activity

- Increased emphasis on safety and environmental concerns

- Recent tax reform likely to lead to higher capital spending

- Valuation multiples remain near all-time highs

- Cross-border M&A activity surged

- Continued low cost of capital and high capital availability

- Key macroeconomic indicators seeing coordinated strength

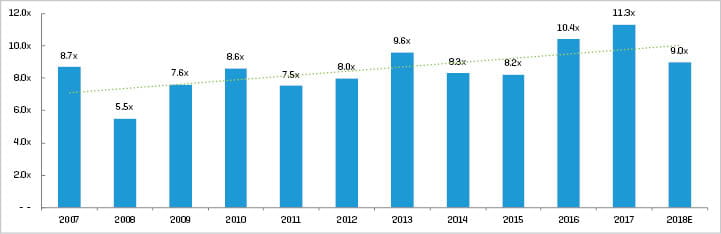

Historical Enterprise Value / EBITDA Multiples ¹

(1) Multiples above 20x are excluded from the mean/median calculation; data represents the overall median of all nine subsegment benchmarks presented in this report

Industry Statistics

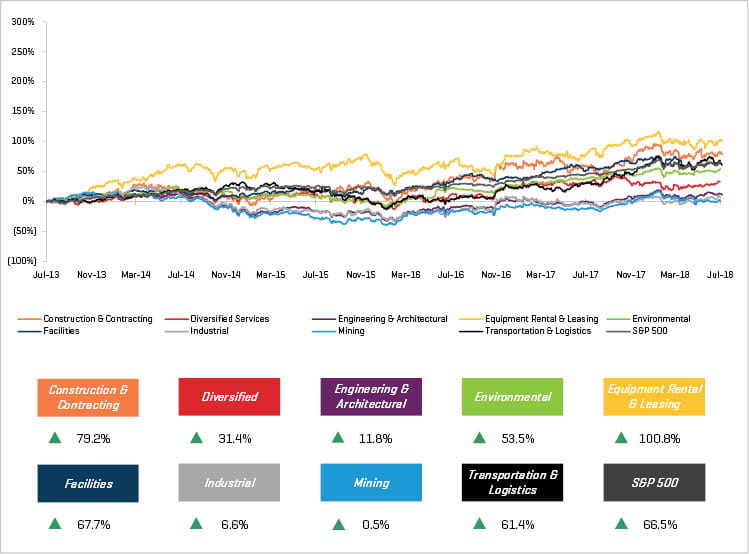

5 –Year Historical Share Price Performance

Operating and Market Performance

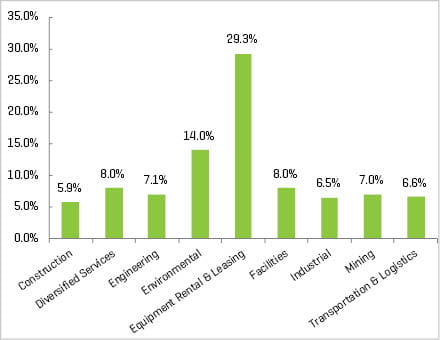

LTM EBITDA Margin

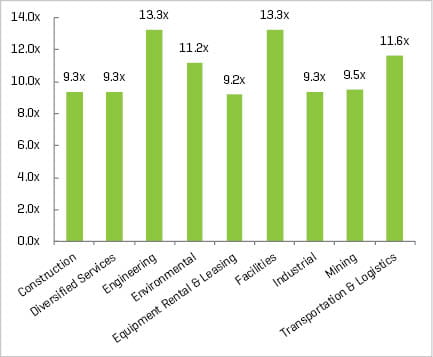

Enterprise Value / LTM EBITDA ¹, ²

(1) Multiples above 20x are excluded from the mean/median calculation

(2) Median from public comp sets featured in report

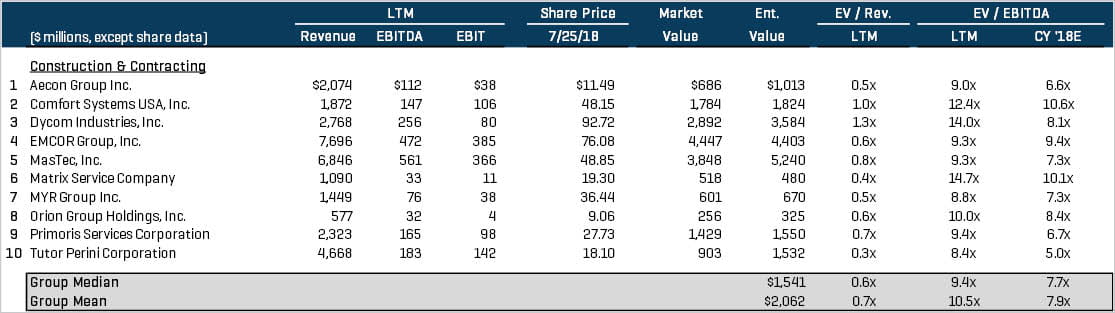

Construction & Contracting Services

The construction segment saw a handful of strategic transactions poised toward expanding scale and geographical reach and diversification, as businesses continue to adapt to changes in technology, automation, and federal policy. Notable transactions include:

- Ashford Holding Corp. announced the acquisition of Remington’s U.S.-based project management division (Project Management, LLC.) in an all convertible preferred stock transaction valued at $203 million, or $140 per share, representing a multiple of 12.4x LTM EBITDA

- Granite Construction Inc. (NYSE:GVA) acquired Canadian-based Liqui-Force Services (Ontario) Inc., expanding Granite’s CIPP lining technology and trenchless pipe rehabilitation capabilities

Public Comparables ¹

Select M&A Transactions

(1) Multiples above 20x are excluded from the mean/median calculation

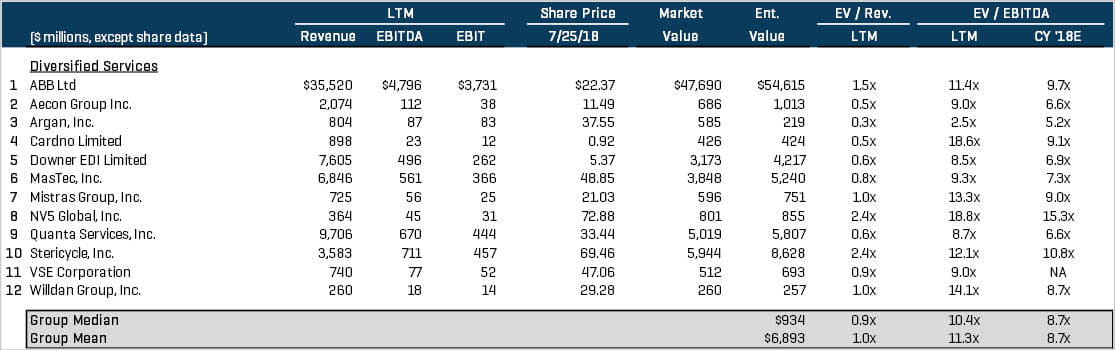

Diversified Services

Relatively larger acquisitions by public, international corporations fueled activity in the diversified services segment, indicative of strategic and financial buyers’ desire to further diversify capabilities and portfolios. Notable transactions include:

- Global Construction Services (ASX:GCS) announced the acquisition of SRG Limited (ASX:SRG), in an all-stock deal valued at $133 million, or 2.48 shares of GCS stock per share of SRG. The merger is expected to produce cost synergies between $3 million and $4 million per year, while increasing service offering and scale

- Cardno Limited’s (ASX:CDD) acquired of Australia-based SureSearch Pty. Ltd., which will strengthen Cardno’s utilities management, survey, infrastructure design, geospatial, and project management services

Public Comparables ¹

Select M&A Transactions

(1) Multiples above 20x are excluded from the mean/median calculation

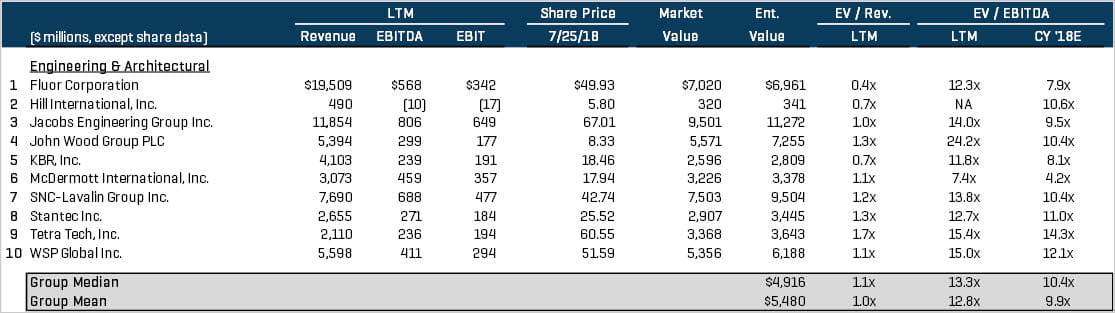

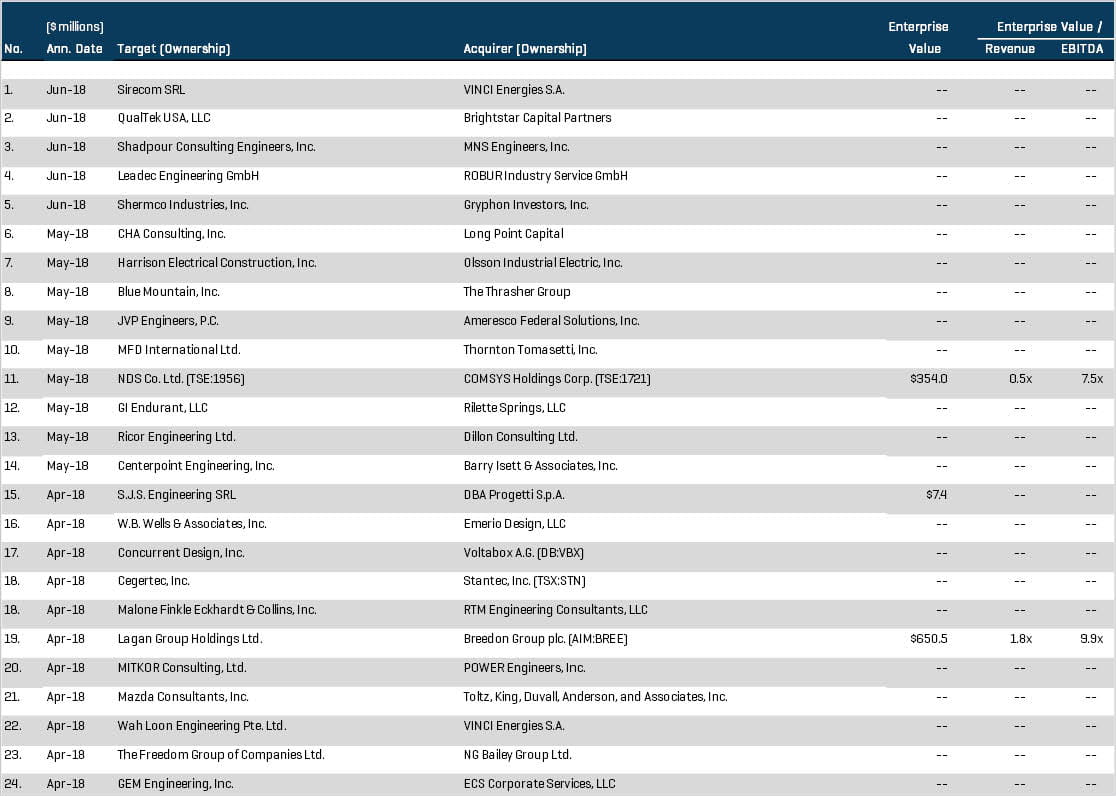

Engineering & Architectural Services

International strategic buyers headlined an active second quarter for the engineering and architectural services segment, as businesses anticipate that rising aggregate private investment will fuel industry growth moving forward. Notable transactions include:

- Stantec Inc. (TSX:STN) acquired Canada-based Cegertec Inc., which will strengthen the expertise and operational diversity of Stantec’s Canadian Consulting Services division, as well as adding over 250 new employees

- VINCI Energies SA (ENXTPA:DG) acquired Singapore-based Wah Loon Engineering Ltd. and announced acquisition of Italian-based Sirecom Srl, expands VINCI’s engineering services across Europe and South East Asia, marking the company’s 13th and 14th acquisitions since the start of 2016

Public Comparables ¹

Select M&A Transactions

(1) Multiples above 20x are excluded from the mean/median calculation

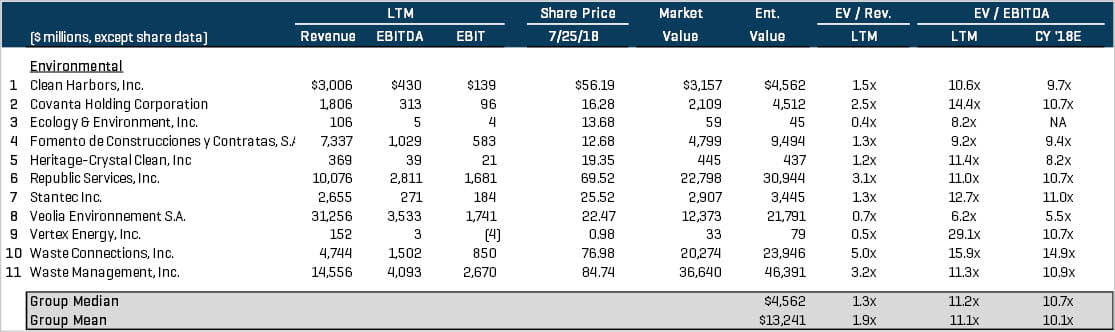

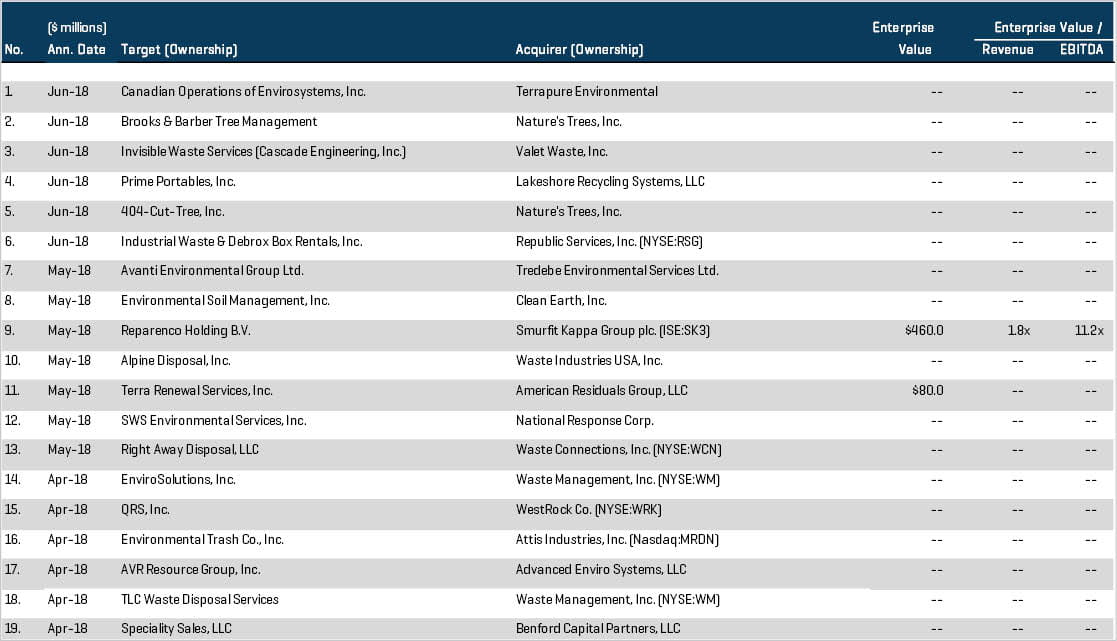

Environmental Services

The environmental services segment experienced heavy M&A activity among the leading strategic players, continuing the first quater’s significant acquisition movement. The acquisitive nature of environmental services companies is indicative of broader industry growth, driven by governmental regulation and technological advances. Notable transactions include:

- Waste Management, Inc. (NYSE:WM) acquired of U.S.-based EnviroSolutions, Inc. and announced the acquisition of U.S.-based TLC Waste Disposal Services, which further expands WM’s recycling capabilities and resources throughout the Detroit and Mid-Atlantic regions

- Waste Connections, Inc. (NYSE:WCN) continued its first-quarter M&A activity by acquiring U.S.-based Right Away Disposal, LLC, which includes four collection operations, one MRF, two transfer stations, and one MSW landfill

Public Comparables ¹

Select M&A Transactions

(1) Multiples above 20x are excluded from the mean/median calculation

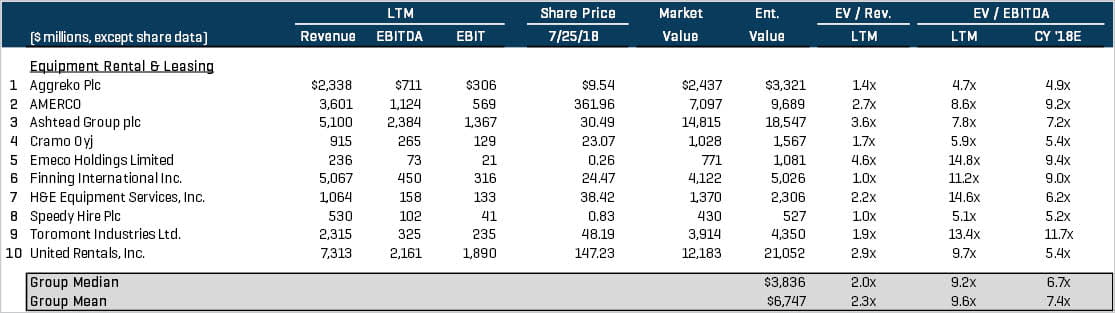

Equipment Rental & Leasing

The equipment rental and leasing segment experienced moderate activity in the second quarter of 2018, with the majority of transactions centered around North American and European market consolidation. Notable transactions include:

- Cramo Oyj (HLSE:CRA1V) acquired Sweden-based Nordic Modular Group AB for approximately $308 million or 17x LTM EBITDA, further expanding its market share throughout Northern Europe, while also gaining in-house modular solution development and production capabilities

- American Rentals Inc. acquired U.S.-based Highland Equipment Rental, which further consolidates the Southern California market, while providing American Rentals access to the Inland Empire region of Los Angeles

Public Comparables ¹

Select M&A Transactions

(1) Multiples above 20x are excluded from the mean/median calculation

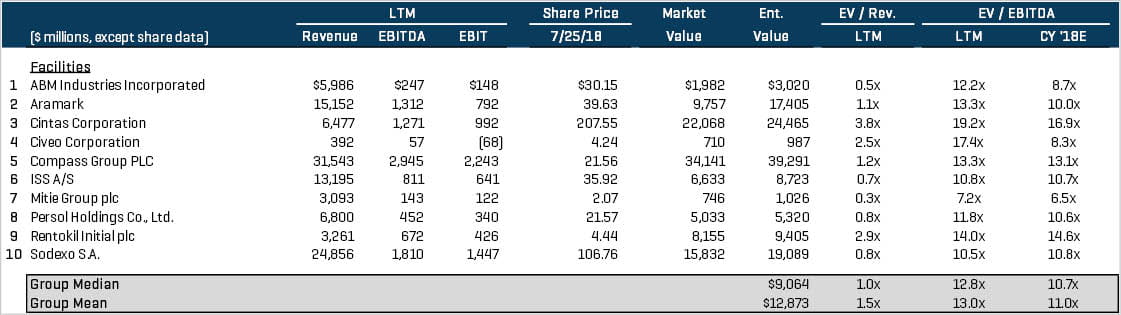

Facilities Services

M&A activity for the facilities services segment was led by the merging of Atalian Global Services and Servest Group Limited to create Atalian Servest, which will now be the fifth largest facility service company in the world. Notable transaction details include:

- The U.K.-based Servest Group and France-based Atalian Global merger results in a combined entity generating revenues of over $3.7 billion at the end of 2018. Additionally, it employs more than 125,000 people worldwide and operates in more than 30 countries across four continents

- The combined entity, Atalian Servest, acquired U.K.-based Unique Catering & Management Services Ltd. and U.K.-based Thermotech Solutions Limited, just one month after the merger, demonstrating its plan to grow its market share through acquisition

Public Comparables ¹

Select M&A Transactions

(1) Multiples above 20x are excluded from the mean/median calculation

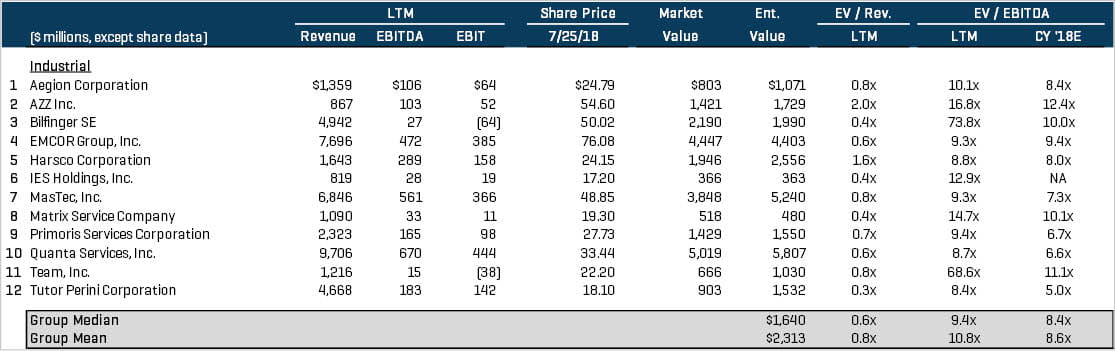

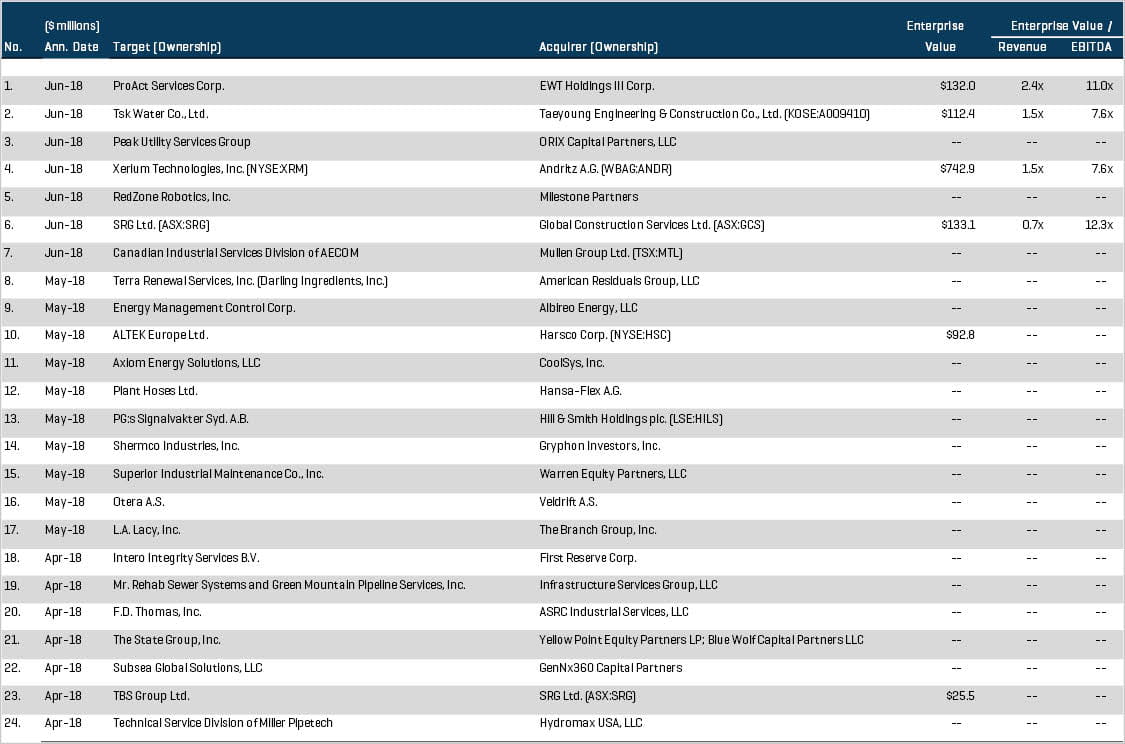

Industrial Services

Industrial services M&A activity continues to be very active from both strategic and financial buyers. Strategic buyers look to expand service offering and ability to serve as a “one-stop shop” for customers. Notable transactions include:

- Mullen Group Ltd. (TSX:MTL) acquired the Canadian Industrial Services Division of AECOM (NYSE:ACM), resulting in a perfect synergistic fit between the product services division of Mullen’s Oilfield Services segment. The transaction includes over 350 employees and over 250 pieces of specialized equipment which will better serve Mullen in a very competitive Canadian market

- Evoque Water Technologies (NYSE:AQUA) announced the acquisition of U.S.-based ProAct Services Corporation from HKW Capital Partners for $132 million or 11.0x LTM EBITDA. This will allow Evoque to expand its portfolio offering within water and wastewater treatment, hydrostatic water treatment, and coal ash pond remediation

Public Comparables ¹

Select M&A Transactions

(1) Multiples above 20x are excluded from the mean/median calculation

Mining Services

Although the mining services industry is beginning to see an uptick in activity, companies are still fiercely competing for major projects. As a result, M&A is being used as an alternative way to gain access to certain geographical regions and profitable mining projects. Notable transactions include:

- South32 Limited (ASX:S32) announced the acquisition of Canada-based Arizona Mining Inc. (TSX:AZ) for $1.3 billion, and announced the 50% stake of Australian-based Eagle Down Metallurgical Coal Project for $133 million. Both acquisition’s will allow South32 to develop high-quality, long-life projects that are expected to deliver significant value to shareholders

- Glencore Plc (LSE:GLEN) acquired a 49% stake in Australia-based Hunter Valley Operations (HVO) coal mine, which solidifies its position as the world’s biggest exporter of the fossil fuel

Public Comparables ¹

Select M&A Transactions

(1) Multiples above 20x are excluded from the mean/median calculation

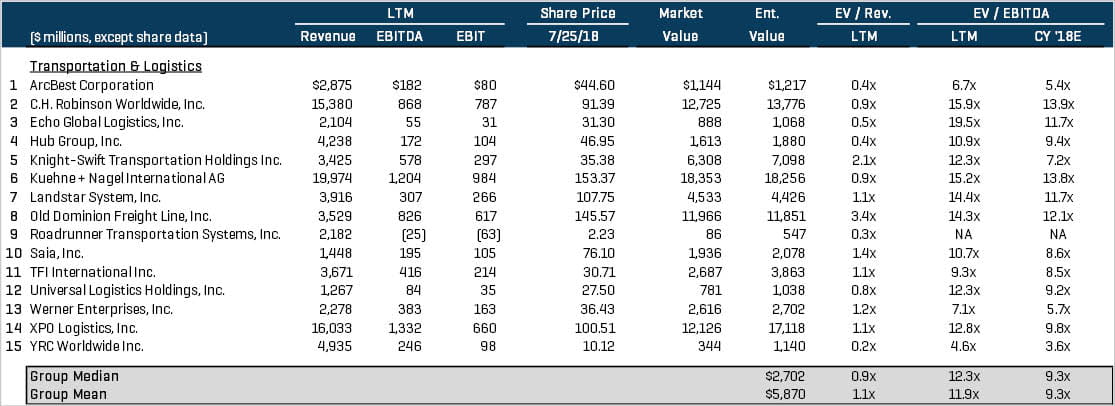

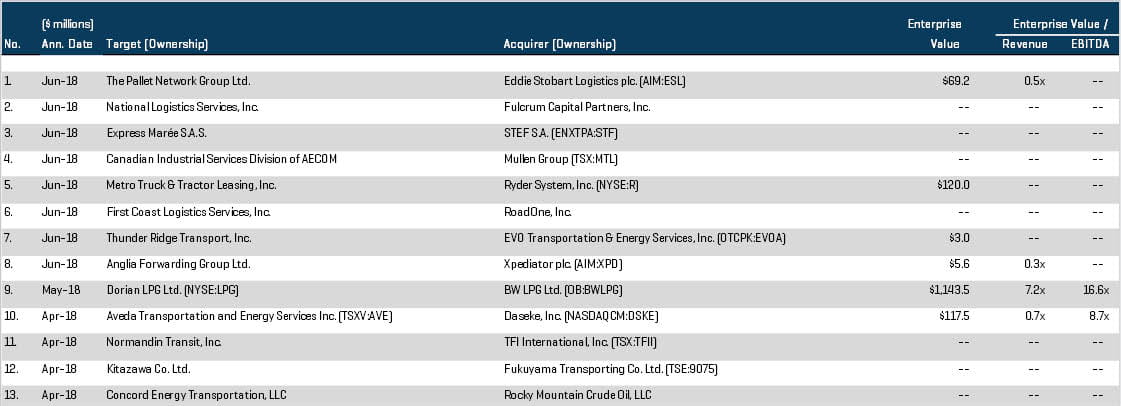

Transportation & Logistics

Transportation and logistics Q2 M&A activity was driven by a handful of cross-border transactions, with distinguished focus on Canadian-based companies. Notable transactions include:

- Daseke, Inc. (Nasdaq:DSKE) acquired Canada-based Aveda Transportation and Energy Services (TSX:AVE) for approximately $120 million, or 8.7x LTM EBITDA. Aveda’s revenue in 2017 was up 172% from 2016, representing a great opportunity for Daseke to grow its energy transportation services within Western Canada

- TFI International Inc. (TSX:TFII) acquired Canadia-based Normandin Transit Inc., which will add over 300 tractors and 1,000 trailers to TFI’s extensive fleet

Public Comparables ¹

Select M&A Transactions

(1) Multiples above 20x are excluded from the mean/median calculation

*Source for all charts: S&P Capital IQ