Separation Anxiety Valuing Convertible Bonds

Separation Anxiety Valuing Convertible Bonds

As hybrid instruments, convertibles have unique benefits, but assessing the fair value of a convertible’s debt and equity components is a complex task.

When raising capital, many early-stage or credit-starved firms turn to convertibles — bonds and preferred stock with conversion features or attached warrants. For these firms, the motivation is generally to entice investors while simultaneously limiting the near-term cash flow burden of interest payments. For investors, on the other hand, convertible bonds not only offer some level of protection on the downside, as convertibles have seniority over common equity, but also allow for upside potential if the issuer’s underlying equity appreciates in value.

Convertibles often have two key features that deviate from plain-vanilla financing. First, the interest rate on the convertible tends to be lower than the rate for a comparable instrument with no conversion feature. Second, investors in convertibles gain equity exposure via the conversion feature or warrant. These two features are intimately related at issuance, as the lower interest rate on the convertible is seen as a tradeoff for gaining equity exposure.

While convertibles can provide the issuer with operational flexibility by limiting interest or dividend payments, they can also produce accounting and valuation challenges for the reporting entity, both at issuance and in subsequent reporting periods. For instance, convertibles may contain features such as contingent interest, make-whole provisions, and call and put features that may be classified as embedded derivatives and may require bifurcation for accounting purposes. Furthermore, even if the conversion option does not require bifurcation under Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) Topic 815, Derivatives and Hedging (ASC 815), the issuer must evaluate the instrument to determine if ASC Topic 470-20, Debt with Conversion and Other Options (ASC 470-20, formerly FASB Staff Position APB 14-1) is applicable. This requires the issuer to separately account for the liability and equity components of an instrument in a manner that reflects the issuer‘s nonconvertible debt borrowing rate.

Overview of Convertibles

Convertibles are hybrid securities that exhibit characteristics of both debt and equity. On one hand, convertibles are debt-like in that investors earn periodic coupon or dividend payments, maintain liquidation preference over common stock, and may have a defined maturity date (provided the security is not converted or otherwise called earlier) at which time the investor receives the full principal amount plus accrued but unpaid interest. On the other hand, convertibles are equity-like in that the investor has the option to convert the security into common equity, at a contractual conversion price and during a predefined time period, and typically has voting rights on an “as if” converted basis throughout the life of the convertible.

Plain-vanilla convertibles can be seen as a straight bond with an equity call option attached.

Given their hybrid nature, convertibles are often viewed as a straight bond with an equity call option. A company issuing a convertible is effectively exchanging call options on its equity for lower borrowing costs.

Convertibles often have additional call and put provisions. For example, a convertible can include a covenant allowing the issuer to call the bond before maturity at a predefined price (usually at a premium). In this case, the issuer might find it economical to exercise such an option when interest rates have decreased and the issuer can borrow at a lower cost. Or, if the underlying equity crosses a given threshold, the issuer might be able to force conversion, in which case the investor loses some of the equity upside. Conversely, the investor might enjoy a protective provision under certain conditions (e.g., a change of control) that provides the ability to return the bond to the issuer at a predefined price (usually at par value), allowing for further downside protection.

Issuers use convertible financing for several reasons:

- The company can lower the cash flow burden of its debt financing rather than issue straight debt or preferred stock alone. In periods of rising stock prices or high volatility, the reduction in coupon or dividend payments can be substantial.

- Lower-credit companies that may not be able to access the traditional debt or preferred stock markets can more readily find financing via convertibles.

- Companies that anticipate equity appreciation can use convertibles to defer equity financing to a time when growth has been achieved, thus lowering interim dilution.

Convertibles allow an issuer to pay lower interest rates in exchange for a share of the upside in its equity, and generally increase flexibility for the issuer.

Applicable Accounting Guidance

Given that convertibles often have distinctive attributes that are specific to each security, it’s no wonder the accounting literature pertaining to these instruments is complex. In general, ASC 815 governs the treatment of derivatives embedded in convertibles. In addition, the accounting considerations for convertible debt often go beyond ASC 815 and require consideration of other literature such as ASC 470-20. Furthermore, any aspect of the convertible that is measured at fair value must adhere to ASC Topic 820, Fair Value Measurement (ASC 820).

The FASB views convertibles as “hybrid instruments,” or contracts that embody both a host contract and an embedded derivative. The straight bond component of a convertible is viewed as the host contract; the equity call option and any other call and put options are together viewed as the embedded derivatives.

Separately identified embedded derivatives must be measured at fair value on each balance sheet date, with changes in fair value flowing through earnings.

When evaluating the appropriate way to treat the accounting for convertibles, the principal issue (addressed herein) is whether the embedded derivative requires separate recognition from the host contract. Separately identified derivatives must be measured at fair value on each balance sheet date, with changes in fair value flowing through earnings. The host contract (i.e., the straight debt component) may not require fair value measurement in subsequent reporting periods. Thus, due to the potential impact on earnings volatility, the accounting treatment can be particularly critical for reporting entities that issue convertibles.

ASC 815-15-25 outlines three primary criteria that must be met if derivatives embedded in a convertible are to be accounted for as a separate liability:

- The economic characteristics and risks of the embedded derivative are not clearly and closely related to the economic characteristics and risks of the host contract. That is, if the two components of a convertible exhibit similar economic characteristics and risks, the embedded derivative does not require separate recognition.

- The hybrid instrument is not remeasured at fair value under otherwise applicable generally accepted accounting principles (GAAP), with changes in fair value reported in earnings as they occur. If the hybrid instrument is already reported at fair value under other applicable GAAP, there is no need to separately recognize the embedded derivative, because changes in the derivative’s fair value would already be incorporated in the fair value measurement of the security as a whole.

- A separate instrument with the same terms as the embedded derivative would, pursuant to ASC 815-10-15, be considered a derivative instrument subject to the requirements of ASC 815. If the embedded derivative would not necessitate fair value measurement on a stand-alone basis, there is no need to separate the derivative from the host contract.

In addition to these three criteria, the approach to accounting for these convertibles, particularly in the case of convertible preferred stock, may differ based on the settlement alternatives for the instrument. Convertible preferred stock may be classified on the balance sheet as equity or as a liability, depending on whether the security may ultimately be settled in cash or in shares of common stock. While all convertibles must initially be measured at fair value, those classified as equity may not require subsequent measurement whereas those classified as liabilities must be remeasured, with changes in fair value being reported in earnings.

In general, unless the economic substance of the instrument indicates otherwise, a convertible is initially classified as a liability if it:

- requires net cash settlement upon conversion or maturity; or

- gives the counterparty (i.e., the investor) the choice of a settlement in net cash or in shares.

The balance sheet classification for convertibles generally depends on whether the instrument is assumed to be settled in cash (liability) or shares (equity).

Conversely, a convertible is initially classified as equity if it:

- requires physical or net share settlement upon conversion or maturity; or

- gives the reporting entity (i.e., the issuer) the choice of a settlement in net cash or in shares. (This is not the case under International Financial Reporting Standards (IFRS), where net settled contracts are classified as liabilities even if the settlement method is at the issuer’s discretion.)

Valuation Methodology

When a reporting entity determines that an embedded derivative requires separate recognition, the derivative’s fair value must be determined as of each reporting period. As described earlier, the value of the convertible is essentially that of a straight bond plus a plain-vanilla call option. A back-of-the-envelope approximation might include valuing the straight bond discretely through an income approach, and then using a closed-form option pricing model (e.g., the Black-Scholes model) for the derivative

However, a lattice or binomial option pricing model is widely preferred over a closed-form option pricing model (e.g., the Black-Scholes model) because it can capture all features of the instrument and allows for greater analytical flexibility, including accounting for the relationship between the straight bond and the derivative from a default risk perspective. As such, for any issuer (aside from the theoretical riskless one that does not face the prospect of default), using the closed-form call option value as proxy for the conversion feature value in fact undervalues both the convertible and the conversion feature of the embedded derivative.

When valuing convertibles, the lattice or binomial option pricing model is the preferred approach.

The valuation of the convertible relies on a “decision tree” that compares an equity lattice and a valuation lattice, from the perspectives of both issuer and holder, to seek an optimal decision at every node.

The equity lattice represents the potential evolution of the underlying stock price during the life of the convertible. Starting from the current price, the stock moves up or down at every node on the lattice, consistent with a given equity volatility; once the issuer defaults, the underlying stock is worthless. The probabilities for up, down, and default movements are such that in the risk-neutral framework, the expected discounted value of the stock matches the current stock price.

The valuation lattice has the same number of nodes as the equity lattice, but the construction starts at maturity, where the payoff of the convertible is known. At maturity, the investor in the convertible will choose as follows:

MaturityValue = Max[Principal + Coupon, ConversionValue]

In this equation, ConversionValue is the value of the security as converted into equity, when compared with the corresponding node in the equity lattice, and Principal and Coupon have the same meaning as in a pure debt instrument.

As the decision tree works its way back toward issuance, both issuer and investor enjoy optionality. At any point before maturity, for example, the issuer will want the following:

IssuerValue = Min[CallValue, ForcedConversion, ContinuationValue]

Here, CallValue refers to whether the issuer can call the convertible at the predetermined price, ForcedConversion refers to the potential optionality the issuer might have to force conversion on the holder, and ContinuationValue is the value of the convertible should the issuer decide not to call, nor to force conversion for one more time period. The value reflected in the latter captures an unwelcome possibility: If the issuer defaults, the holder will receive only a portion of the total principal, referred to as the “recovery rate.” Also, the probability of a default, captured by the “default intensity,” is a measure of the credit risk of the issuer.

From the investor’s perspective, the optimal decision at every node in the lattice is described as follows:

HolderValue = Max[IssuerValue, ConversionValue, PutValue]

Once again, ConversionValue is derived from the stock price at the corresponding node of the equity lattice. PutValue refers to any optionality the investor might have in terms of putting the bond back to the issuer at a predefined price. Thus, the HolderValue at the first node of the valuation lattice captures the optimal decisions from both holder and issuer and is a fair representation of the value of the convertible.

In the absence of a) forced conversion, b) the issuer’s call, or c) the holder’s put, the value of the conversion feature is equal to the difference between the value of the convertible when the conversion feature is allowed versus when it is removed. Also, by construction, the convertible’s value absent the conversion feature is the value of a straight bond, which, in this context, is the host instrument for accounting purposes.

Case Study

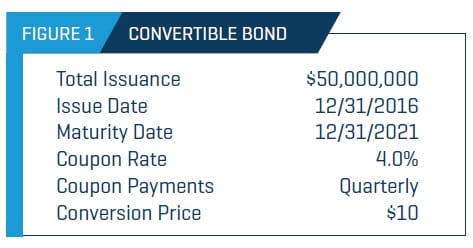

To illustrate the potential impact of embedded derivatives on a reporting entity’s financial statements, let’s expand on the example above. Assume that XYZ Company issued a $50 million convertible bond on December 31, 2016, with a maturity date of December 31, 2021. The convertible bond has a stated coupon rate of 4.0% per annum, paid quarterly, and a conversion price of $10 per share of XYZ’s common stock. This means that a holder of the convertible bond would find it economically advantageous to exercise conversion if and when the common price of XYZ is above $10 per share (Figure 1).

XYZ’s management and its auditors have determined that the conversion feature embedded in the convertible bond must be accounted for separately as a derivative liability because a redemption feature provides the holders with a mechanism to “net settle” the conversion feature into cash at the investor’s election. Furthermore, the embedded conversion feature’s economic characteristics are more akin to an equity instrument, whereas the convertible bond is more clearly and closely related to a debt instrument with its scheduled coupon payments and maturity date. Therefore, XYZ must record an embedded derivative liability representing the fair value of the conversion option, measure the liability to fair value at each subsequent reporting date, and record changes in fair value on the income statement.

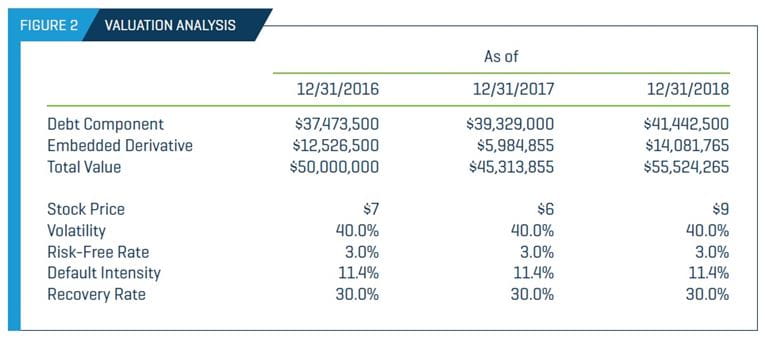

Figure 2 outlines the inputs and outputs of a lattice model analysis for the convertible bond as of the issuance date and the subsequent two fiscal year-ends. For simplicity, assume that XYZ’s volatility remains constant at 40.0%. Likewise, assume that the 3.0% risk-free rate and XYZ’s creditworthiness remain constant. Only the common stock price of XYZ changes from date to date, starting at $7 as of issuance. We have assumed that a 30.0% recovery rate is appropriate for this convertible bond, and the default intensity (which reflects the implied credit risk of the issuer) has been calibrated such that the lattice price matches the issuance price as of December 31, 2016, since we assume this is a market-based convertible issuance.

Based on the inputs summarized in Figure 2, the fair value of the embedded derivative is slightly more than $12.5 million on the issuance date, whereas the debt component of the convertible bond has a fair value of just under $37.5 million, for a total fair value of $50 million (equal to the issuance price, as an arm’s length transaction requires).

Moving forward one year, assume that XYZ’s common stock price is trading at $6 per share. Recalculating the fair values results in a roughly $6.5 million decrease in the value of the embedded derivative and a $1.9 million increase in the value of the debt component. Most of the loss in the value of the convertible bond, fair valued now at $45.3 million, comes from the reduced value of the conversion feature. In the absence of default, and with creditworthiness and discount rates constant, the value of the debt component will increase as maturity approaches.

One year later, assume that XYZ’s common stock price is trading at $9 per share. Recalculating the fair values this time results in an $8.1 million increase in the embedded derivative and a $2.1 million increase in the debt component. At this point, the note is trading at $55.5 million (roughly 11% above par). Of this, about $1.5 million is due to the increase in value of the embedded derivative because of stock appreciation, while the rest is due simply to the passage of time from issuance.

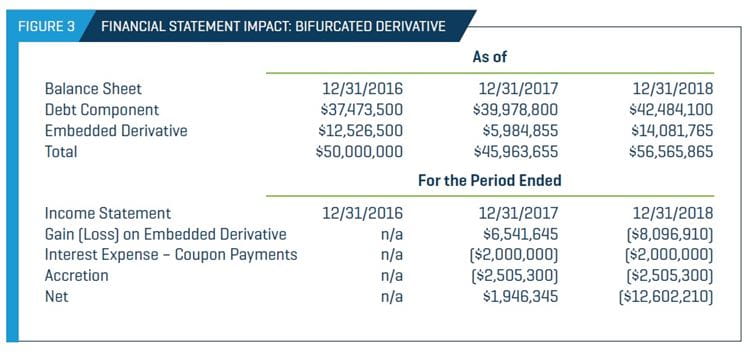

Figure 3 outlines the impact of this valuation analysis from a financial statement perspective. The embedded derivative is stated at fair value on each balance sheet date, with changes in the fair value flowing through earnings as a gain or a loss. While the debt component of the convertible bond is initially measured at fair value, it is not remeasured on subsequent balance sheets. Rather, the bond accretes to face value (i.e., $50 million) as its maturity date draws near. The income statement is affected by the gain or loss of the embedded derivative, by coupon payments in cash, and by any implied interest expense associated with accretion.

Communicate, Coordinate, and Contemplate

Convertible securities are complex financial instruments with equally complex accounting and valuation challenges, particularly given that changes in value may have a significant impact on earnings per share and other financial metrics deemed important by investors. Each instrument is unique, requiring a sound understanding of both accounting regulations and the assumptions employed in valuing these securities.

These challenges underscore the importance of clear communication, coordination, and thoughtful contemplation between financial statement preparers, auditors, and valuation experts.

This is an updated version of an article that appeared in the Fall 2010 issue of The Journal.