Purchase Price Allocation Procedures: Financial Reporting, Tax Reporting, and Valuation Analyses, Oh My!

Purchase Price Allocation Procedures: Financial Reporting, Tax Reporting, and Valuation Analyses, Oh My!

An updated version of this article is available. Please see "Differences in PPA Procedures: Financial Reporting vs. Tax Reporting," published in the Spring 2017 Journal.

Purchase Price Allocations – Introduction

Mergers and acquisitions trigger many financial and tax reporting requirements. One common requirement for both purposes is acquisition accounting (i.e., a purchase price allocation or a “PPA”). A PPA is an allocation of the purchase price paid to the assets and liabilities included in a transaction. Although a PPA performed for financial versus tax purposes may be very similar, there are several key differences to understand and consider in a valuation analysis.

Financial Reporting Versus Tax Reporting

In the United States (“U.S.”), guidance pertaining to completing a PPA is contained in Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 805, Business Combinations (“FASB ASC 805”). Subsequent to all transactions that involve a change in control, companies are required to complete a PPA (regardless of whether the transaction is structured as an asset deal or a stock deal). Sections 1060 and 338 of the Internal Revenue Code (“IRC”) detail procedures for completing PPAs for U.S. tax reporting purposes. In contrast to financial reporting guidelines, U.S. tax regulations only include PPA requirements for transactions that are structured as an asset deal (or as a deemed asset sale in the instance in which a transaction is structured as a stock deal, but an election is taken under Section 338 of the IRC). However, it is important to note that even in the case of a pure stock deal, a separate PPA for tax reporting purposes may be required for transactions involving overseas operations/foreign legal entities given the tax reporting requirements of other countries.

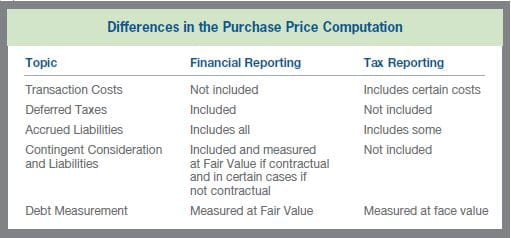

Key differences that may exist between financial reporting and tax reporting PPA valuations are differences in the computed purchase price, standard of value, and valuation methodology/analysis procedures. First, significant differences may arise in the computed purchase price paid in a transaction as a result of the inclusion or exclusion of certain transaction costs, deferred taxes, and accrued liabilities; the inclusion and measurement of contingent consideration and liabilities; and the measurement of assumed debt. These differences are summarized in the table below.

Second, the appropriate standard of value is different for PPA valuations performed for financial versus tax reporting purposes. For financial reporting purposes, the standard of value is “Fair Value,” which is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (FASB ASC 820-10-20). However, the appropriate standard of value from a U.S. tax law perspective is “Fair Market Value,” which is defined as the price at which property would exchange between a willing buyer and a willing seller, when the former is not under any compulsion to buy and the latter is not under any compulsion to sell, both having reasonable knowledge of the relevant facts (Treas. Regs. §20.2031-1(b) and §25.2512-1; Rev. Rul. 59-60, 1959-1 C.B. 237). Although there are specific (and often subtle) differences between the Fair Value and Fair Market Value standards, often the value of an asset valued under these premises of value are very similar (but in certain cases may differ materially).

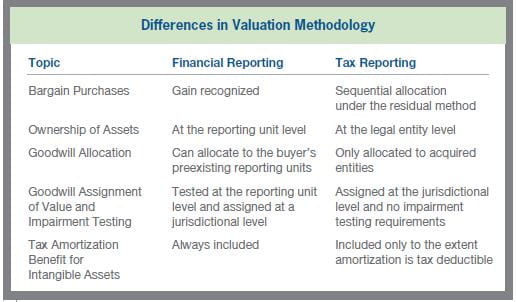

Finally, differences in the valuation methodology and procedures employed in a PPA may arise in valuation analyses performed for financial versus tax reporting purposes. Key differences include the treatment of bargain purchase transactions, the assignment of goodwill and other asset values (and subsequent impairment testing), and the consideration of the tax benefit of intangible asset amortization. These differences are summarized in the table below and detailed in the following paragraphs.

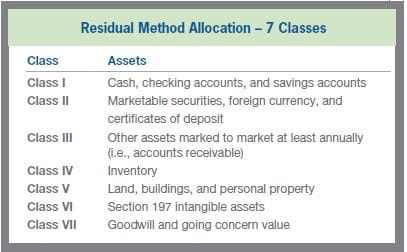

First, in a valuation analysis completed for financial reporting purposes, a gain on a bargain purchase is recorded in instances in which the Fair Value of the net assets acquired exceeds the consideration paid. (The gain is calculated by subtracting the consideration paid from the concluded Fair Value of the assets acquired.) In contrast, in a valuation analysis completed for tax reporting purposes, there are no bargain purchase procedures. Rather, the consideration paid is allocated amongst the net assets acquired based on a class system of asset categories in a process known as the residual method. If the aggregate purchase price allocable to a particular class of assets is less than the aggregate Fair Market Value of the assets within the class (which would occur in the case of a bargain purchase), each asset in such class is allocated an amount in proportion to its Fair Market Value, with nothing allocated to any junior class. See the chart below for further detail as relates to the different classes involved in the allocation of assets under the residual method for tax reporting purposes.

With respect to the assignment of goodwill and other asset values, valuations for financial reporting purposes involve the allocation of asset values at the reporting unit level, and the acquired assets can be added to an acquirer’s existing reporting units (as opposed to the creation of a new reporting unit(s)). In contrast, tax reporting requirements limit the allocation of asset values to the legal entities acquired in a transaction. Further, asset impairment tests are performed at the reporting unit level for financial reporting purposes, while there are no impairment testing requirements for U.S. tax purposes. Finally, the tax benefit of amortization is always included in the concluded Fair Value of an intangible asset for financial reporting purposes (regardless of the transaction structure). For tax reporting purposes, the tax benefit of amortization is only included in the Fair Market Value of an intangible asset to the extent that the amortization of the asset is in fact tax deductible for the acquirer.

Illustrative Example of a PPA for Financial Reporting and Tax Purposes

In the following example, assume that an acquirer (the “Acquirer”) consummated a business combination (the “Transaction”) under a Share Purchase Agreement (the “Agreement”) on December 30, 2011, acquiring the business and substantially all of the assets of ABC Company (“ABC” or the “Company”). The Transaction was structured as an asset purchase for tax purposes through a Section 338(h)(10) election and involved $300 million in purchase consideration. SRR has been engaged to estimate the Fair Value of certain tangible and intangible assets acquired in the Transaction for financial reporting purposes. In addition, ABC’s tax department intends to utilize the results of the valuation analysis to satisfy tax reporting requirements. For this hypothetical example, we assume that the purchase price is the same under each purpose (in reality, this is unlikely to be true given the differences in the purchase price computation noted previously).

Valuation of ABC for Financial Reporting Purposes

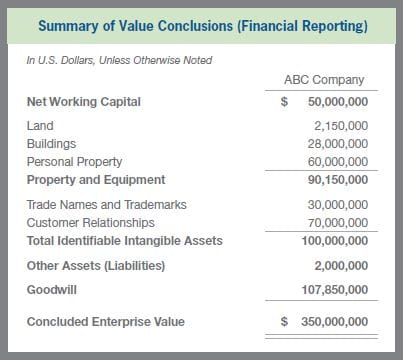

In regard to the financial reporting requirements, it is determined that ABC is to be accounted for by the Acquirer as a single reporting unit. As a result of the valuation procedures employed, SRR concludes that the consideration paid is not equivalent to Fair Value (i.e., the Transaction is a bargain purchase) and the Company’s intangible assets include trade names and trademarks as well as customer relationships. The table below presents the estimation of the Fair Values of the tangible and intangible assets acquired, as of December 30, 2011, pursuant to the guidelines set forth in FASB ASC 805.

Valuation of ABC for Tax Reporting Purposes

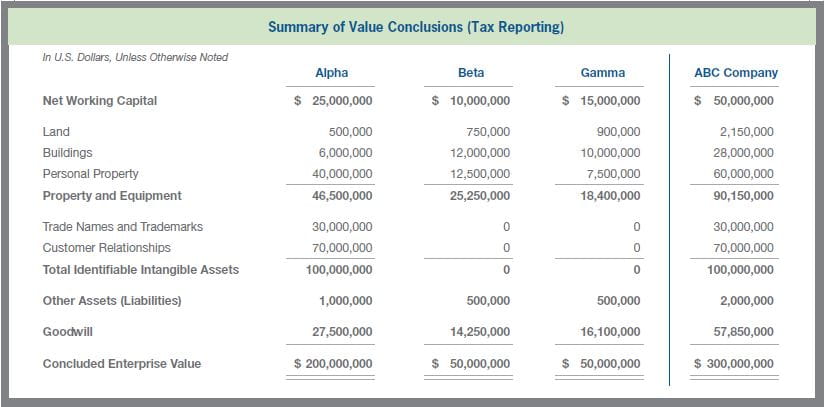

In regard to the tax reporting requirements, it is understood by SRR that ABC is comprised of three legal entities (i.e., Alpha, Beta, and Gamma). As a first step, the overall consideration paid in the Transaction is allocated to each legal entity based on SRR’s independent analysis of the enterprise value of each business. It should be noted that the sum of the enterprise values allocated to each legal entity must reconcile to the total consideration paid in every transaction. Although the Transaction was determined to be a bargain purchase for financial reporting purposes, there are no bargain purchase procedures under U.S. tax reporting guidelines. As such, the overall enterprise value of ABC is different for financial reporting versus tax reporting purposes. Next, net working capital and other assets (liabilities) are allocated to each legal entity based on the respective balance sheets of the legal entities, and property and equipment values are allocated to the legal entity that owns these assets. Next, with respect to intangible assets, Company management represents to SRR that the trade names and trademarks and customer relationships of ABC are legally owned by the Alpha legal entity. The Beta and Gamma legal entities compensate the Alpha legal entity for their use of these intangible assets through the payment of intercompany royalties (which are determined to represent arm’s length transfer pricing arrangements). As a result, the overall values of these intangible assets reside at the Alpha legal entity. Finally, goodwill is allocated to each legal entity based on the residual value remaining after deducting the values of the net working capital, property and equipment, identified intangible assets, and other assets (liabilities) from each legal entity’s enterprise value. Given the existence of a bargain purchase for financial reporting purposes, the goodwill of the consolidated company is different for financial reporting versus tax reporting purposes (as the goodwill allocated for tax reporting purposes is limited by the consideration paid for the Company). The table on the following page presents the estimation of the Fair Market Values of the tangible and intangible assets acquired by legal entity, as of December 30, 2011, pursuant to the guidelines set forth in IRS Sections 1060 and 338.

Conclusion

Despite numerous similarities, several key differences exist in valuation requirements for PPAs completed for financial versus tax reporting purposes. Given the differences described herein, involving members from both a company’s financial reporting group and its tax group in the valuation process can create synergistic savings for the company in relation to the scope of the valuation analyses required subsequent to a transaction. Without coordination amongst these groups, each group may end up completing separate valuation analyses (which could be costly and inefficient) or the same analysis might be used for each purpose (which could be flawed based on the differences noted). A coordinated effort between each group will help keep costs at a minimum, ensure consistency amongst the valuation analyses, and result in conclusions that are appropriate with the respective accounting and tax regulations.