Food & Beverage Industry Update - Q3 2021

Subscribe to Industry UpdatesFood & Beverage Industry Update - Q3 2021

Subscribe to Industry UpdatesStrong Comeback Observed Through Q3 2021

The food & beverage industry has experienced a remarkable roller coaster of a ride in the past 18 months. Retail has seen (and is expected to see) a secular upward shift in consumer spend spent at grocery stores, whereas Foodservice has rebounded from levels once thought unimaginable. The increased availability of COVID-19 vaccinations, decreased infection rates, and the broader re-opening of the economy has overpowered concerns over the Delta variant. As uncertainty has started to subside, buyers have re-focused on strategic initiatives and sponsor-backed opportunities. Strong backlogs, sellers preparing for transactions, buyers (both strategic and financial) back open for business, and credit markets as accommodative as ever have resulted in a strong recovery in M&A markets.

The pause in activity at the outset of the second quarter of 2020 allowed sellers to prioritize both operational and cost efficiencies within their companies. As advisors, we were able to work with our clients to be ready to approach the market once the overall mood shifted. Since the 4Q2020 projects which were halted following the breakout of the pandemic have significantly progressed. It has become a sellers’ market once again. Demand for healthy, sustainable businesses positioned for growth outweighs the supply of such firms, resulting in strong valuations.

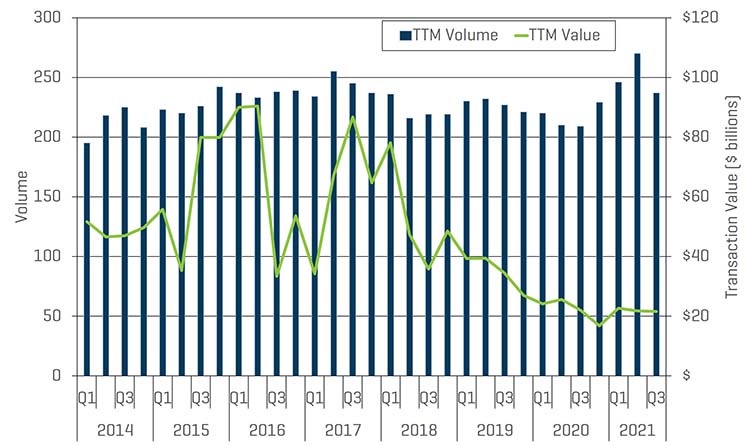

M&A activity in the Food & Beverage (F&B) industry through the first nine months of 2021 continued to post gains. Year to date (YTD) volume was up 5% year over year (YoY) with 161 completed transactions and YTD value was up 43% - quite impressive given what the global economy has experienced since the pandemic began.

Key Q3 Takeaways

- Clear momentum of COVID-19 recovery observed in M&A activity

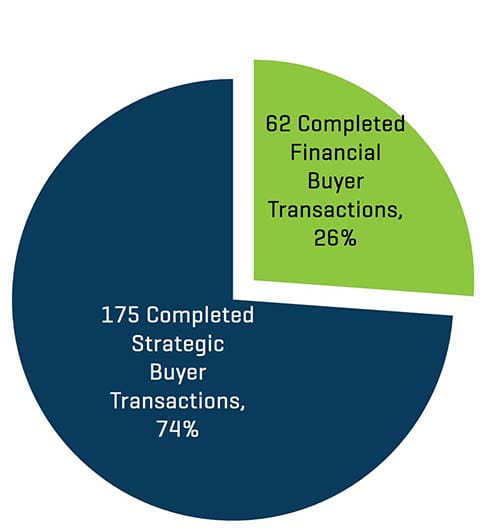

- Strategic buyers continue to dominate the overall F&B industry M&A activity, accounting for 3 out of every 4 completed transactions

- YTD Financial buyer activity increased almost 100% YoY with 47 transactions completed versus 24 transactions one year ago

- Forward EBITDA multiples nearing 10-year highs for many segments

- Key macroeconomic indicators seeing improved strength, apart from inflationary raw material and labor supply pressures (which will likely get worse before subsiding)

HISTORICAL M&A VOLUME AND VALUE

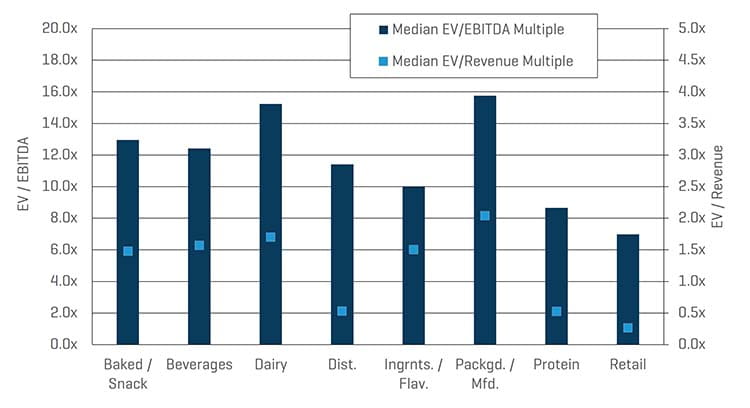

VALUATION BY CATEGORY

Through the third quarter of 2021, sponsor-backed transactions increased 96% YoY while strategic deals decreased slightly, down 12%. Private equity activity benefited from the ample supply of both debt (i.e. open credit markets) as well as equity (via new fund raises) capital. The potential for a significant increase in long term capital gains tax rates – from 23.8% to 31.8% including the 3% surcharge on individual income above $5 million – is clearly a motivating factor for private sellers.

TRANSACTIONS COMPLETED OVER LTM (BY BUYER TYPE)

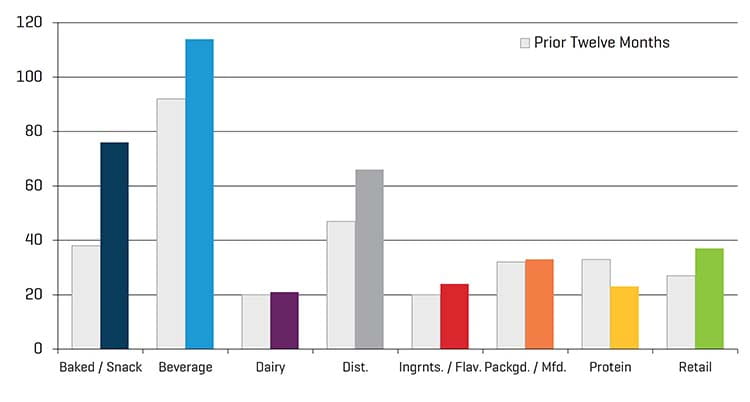

TRANSACTIONS BY CATEGORY, Trailing Twelve Months (TTM)

After an extended period of uncertainty, strategic and financial buyers have re-gained their appetite for M&A. Strong gains were seen in the Baked / Snack (up 100% TTM), Beverage (up 24%), and Distribution (up 40%). Retail transaction volume (up 37%) increased sharply, likely due to the fact that (i) the category has not seen much in the way of activity in the past few years, combined with (ii) industry players with ample cash on their balance sheets, and (iii) strong tailwinds in discretionary consumer behavior and government assistance (stimulus checks, recent increases to SNAP benefits). Furthermore, the swell in demand for healthy, natural products provided a myriad of opportunities for buyers to acquire strategic, high-growth assets in many segments. Sectors seeing YOY declines included Protein, which lagged primarily due to widespread uncertainty in the supply-chain.

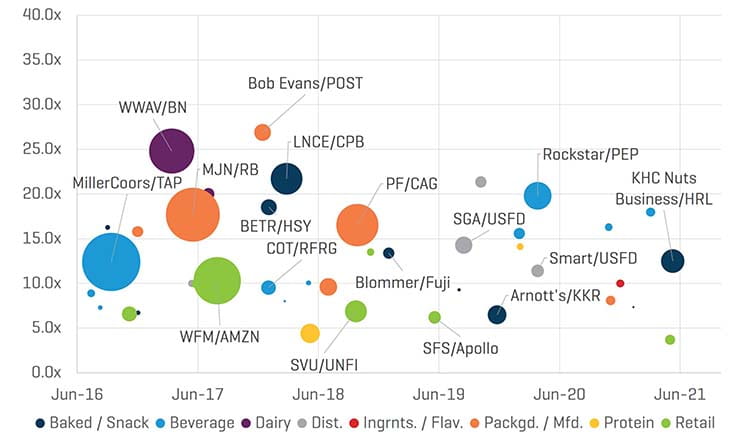

Overview of Recent Transactions

Significant transactions that occurred in 2020 and 2021 include:

- Baked / Snack: Hormel Foods Corporation acquired the Nuts Business of the Kraft Heinz Companies for $3.4 billion or 12.5x EBITDA in June 2021

- Packaged / Manufactured: Crisco Oils and Shortening acquired by B&G Foods North America for $550 million or 8.1x EBITDA in December 2020

- Ingredients / Flavorings: SunOpta's Global Ingredients Segment acquired by Amsterdam Commodities for $390 million or 10.0x EBITDA in December 2020

- Beverage: SweetWater Brewing Company acquired by Aphria for $366 million or 16.3x EBITDA in November 2020

- Beverage: Rockstar acquired by PepsiCo for $4.7 billion or 19.8x EBITDA in April 2020

- Distribution: Smart Foodservice Stores acquired by US Foods for $970 million or 11.4x EBITDA in April 2020

SELECT TRANSACTION EBITDA MULTIPLES

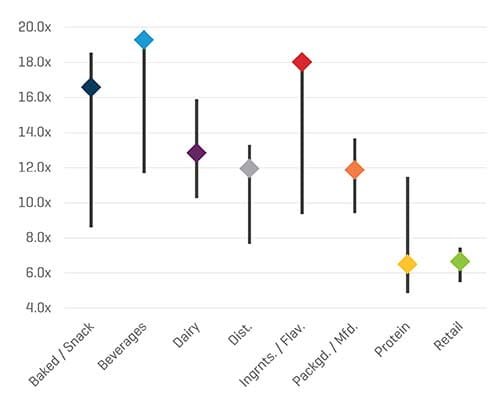

Market Multiples Demonstrate Strengths and Weaknesses Across Segments

The Food & Beverage industry has experienced strong forward market multiples in the third quarter of 2021. Beverages, Distribution, and Ingredients / Flavor segments have all approached or reached 10-year EV / Forward EBITDA highs. Within the Beverages, Ingredients / Flavor, and Baked / Snack segments, market sentiment has been buoyed by a broad increase in interest for healthy, natural products that provide significantly higher margin opportunities. The Distribution segment has been lifted by a considerable recovery in the foodservice following the effects on COVID-19 where revenues were down as much as 70% in the spring of 2020. Logistics issues still loom large for the Protein and Dairy segments, and these challenges have forced many executives to re-examine their supply chains to be more agile which may create long-term value for the future. Going forward, key players within the F&B industry that maintain strong balance sheets and have ample cash and equity currency are expected to pursue growth initiatives through acquisitions to diversify business lines and create new revenue streams that reflect current trends. Casualties of the current environment with less-than-stellar balance sheets may see benefits of considering all strategic options, including restructuring either in or out of court.

CURRENT FORWARD EBITDA MULTIPLES VS. 10-YEAR HISTORICAL RANGE

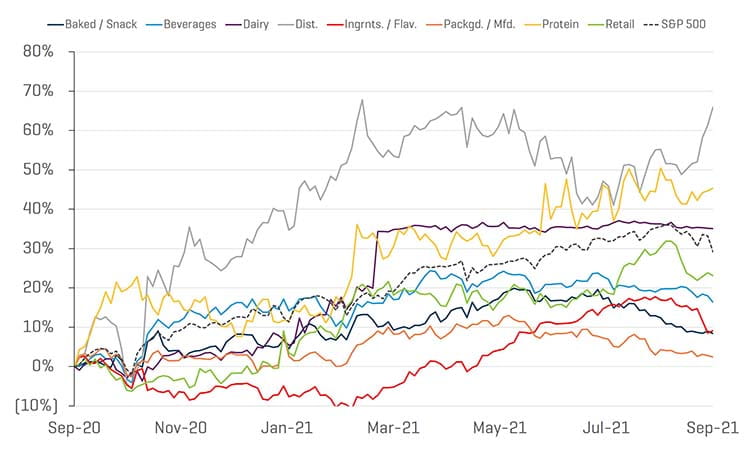

F&B Share Price Performance on Steady Increase

Following a large dip in all sectors of the economy at the start of the pandemic, F&B publicly traded company shares have performed exceptionally well in the last twelve months. Amongst the highest performers, Distribution and Protein posted share price performance increases of approximately 66% YoY and 45% YoY, respectively. While all segments experienced positive share price performance YoY, only the above two segments beat the S&P 500 index. Other trends to note include:

- Foodservice distributors benefitted from increased restaurant and away-from-home food demand as pandemic restrictions have eased

- Grocery store sales have continued to rise as the “pantry-loading” trend for American households has persisted past the peak of COVID-19

- Recent underperformance relative to the S&P likely indicative of the strong returns already booked in the 3Q of last year, rather than foreshadowing any structural impediments going forward

F&B SHARE PRICE PERFORMANCE BY SEGMENT