Food & Beverage Industry Update - Q3 2017

Food & Beverage Industry Update - Q3 2017

Strong M&A Activity Continues in Q3

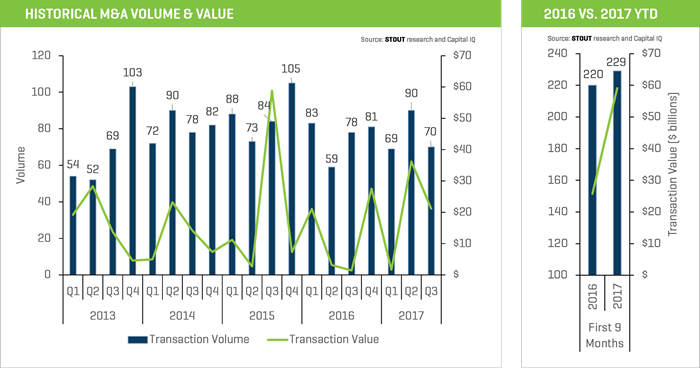

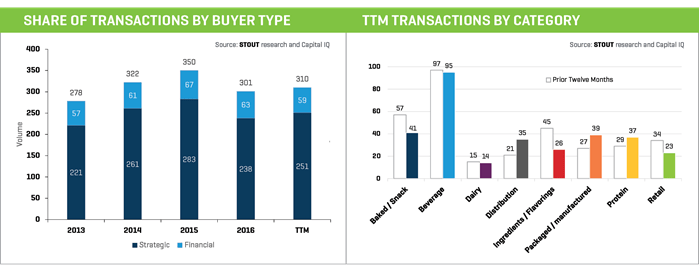

Strong food & beverage industry merger and acquisition (M&A) activity continued in the third quarter of 2017, with 70 completed transactions during the quarter; this represents a 10% decrease year over year (YOY). However, through the first nine months of the year there have been 229 closed transactions, which represents a 4% increase year to date (YTD) versus 2016. It should be noted that the second quarter of 2017 was particularly strong, which may explain the slight decrease YOY.

Barring an extraneous geopolitical event (e.g. North Korea), we expect the remainder of 2017 to be equally robust given 1) valuations remain at peak levels, 2) credit markets are still highly accommodative, 3) strategic buyers are still hoarding cash, 4) private equity’s capital overhang is at or near historical highs, and 5) large consumer packaged goods companies continue to seek accretive growth at all costs.

KEY Q3 TAKEAWAYS

- Continued strong overall food & beverage industry M&A activity

- Reported transaction value increased 129% YTD (driven in large part by Amazon’s $13.4 billion acquisition of Whole Foods and McCormick’s $4.2 billion acquisition of Reckitt’s food business)

- Strategic buyer activity increased 8% YTD

- Cross-border M&A activity remains strong

- Stock market and overall valuation levels at or near all-time highs

- Debt and equity financing remain in ample supply and at attractive rates

- Key macroeconomic indicators remain solid

Quantifying the Increase in Valuations

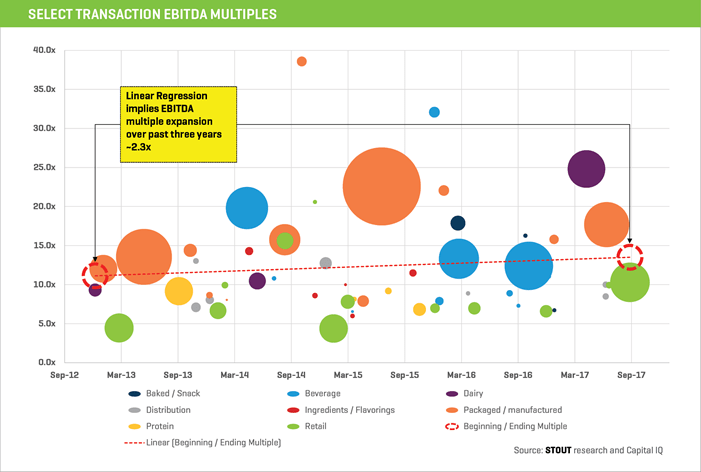

Across all sectors of the economy, we estimate that transaction valuations are one to two multiples of EBITDA higher than just a few years ago, with food & beverage at the upper end of that range.

We analyzed every food & beverage transaction with publicly available information over the past four years. We then ran a linear regression against all such data points. This analysis revealed that valuations in food & beverage have increased approximately 2.3x in the past few years. Valuations at these levels are unprecedented.

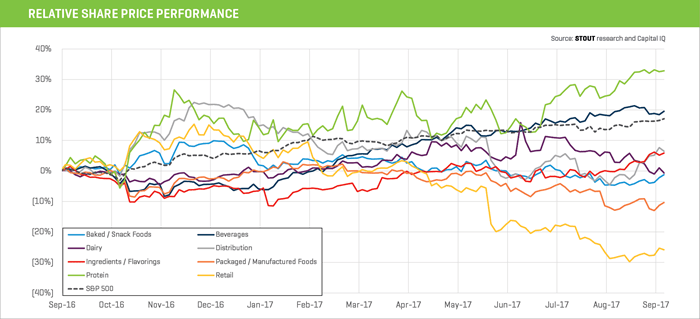

Public Pain of Retail, Large CPG

The past 12 months have been a mixed bag for large, publicly traded food & beverage company stock prices. Except for Protein (which was itself recovering from a severe dip mid-2016) and Beverages, all subsectors underperformed the S&P 500, while two subsectors – Retail and Packaged/Manufactured – are down 26% and 11%, respectively, YOY. Both Retail and large consumer packaged goods companies that sell into grocery are clearly feeling the effects of the recently announced Amazon/Whole Foods transaction as well as expected growth from German deep discounters such as Aldi/Lidl. Neither Amazon/Whole Foods nor Aldi/Lidl are shy about swapping branded products for private label; indeed, private label can compose up to 80% of Aldi/Lidl SKU count.

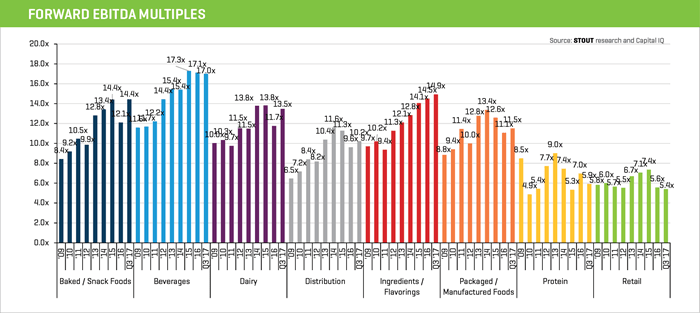

Ingredients, as a whole, have never traded higher and now average nearly 15x total enterprise value/forward EBITDA. Dairy appears to be benefiting from the relative stability (historically speaking) of raw material prices, while Baked/Snack Foods are also trading at peak levels.