Food & Beverage Industry Update – Q1 2018

Food & Beverage Industry Update – Q1 2018

Valuations Remain at Elevated Levels Heading Into Q2

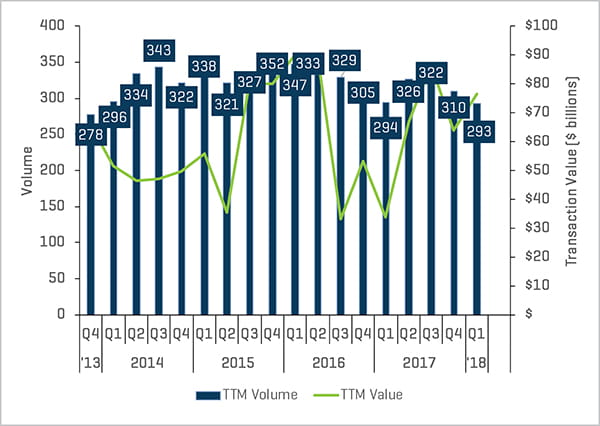

Strong food and beverage industry M&A activity continued through the first quarter of 2018. Trailing-12-month (TTM) value was up 20% at $76.4 billion (due to the recent rash of large deals), though TTM volume was down slightly with 293 transactions completed.

Barring an extraneous geopolitical event (e.g. crippling trade war with China), we expect the remainder of 2018 to be robust given numerous factors: 1) valuations remain at peak levels, 2) credit markets remain highly accommodative, 3) strategic buyers continue hoarding cash, 4) private equity’s capital overhang remains at or near historical highs, and 5) large consumer packaged goods companies continue to seek accretive growth at all costs.

Key Q1 Takeaways

- Overall M&A activity in the food and beverage industry remained strong.

- Reported TTM transaction value increased 20%

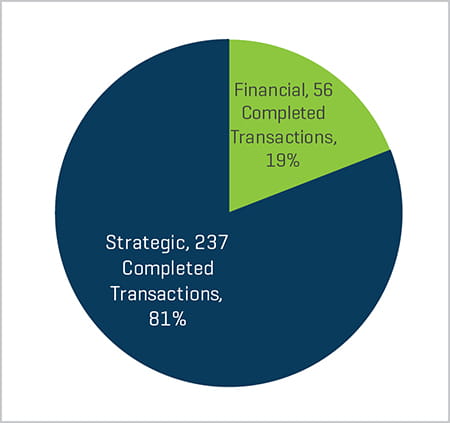

- Strategic buyer activity represented 81% of all transactions completed in the past 12 months

- Cross-border M&A activity remained strong

- Private market valuations remained strong despite the recent pullback in public market stock prices

- Debt and equity financing remained in ample supply and at attractive rates

- Key macroeconomic indicators remained solid

Historical M&A Volume and Value

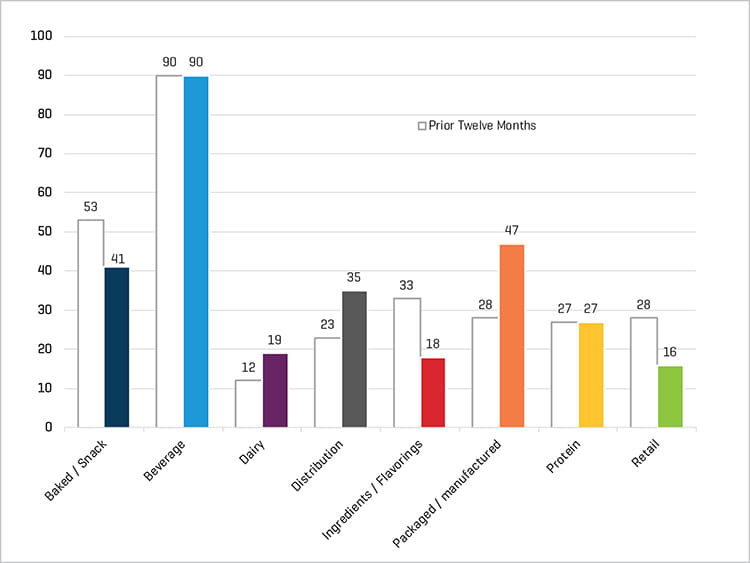

TTM Volume by Category

Transactions Completed Over the Past 12 Months, by Buyer Type

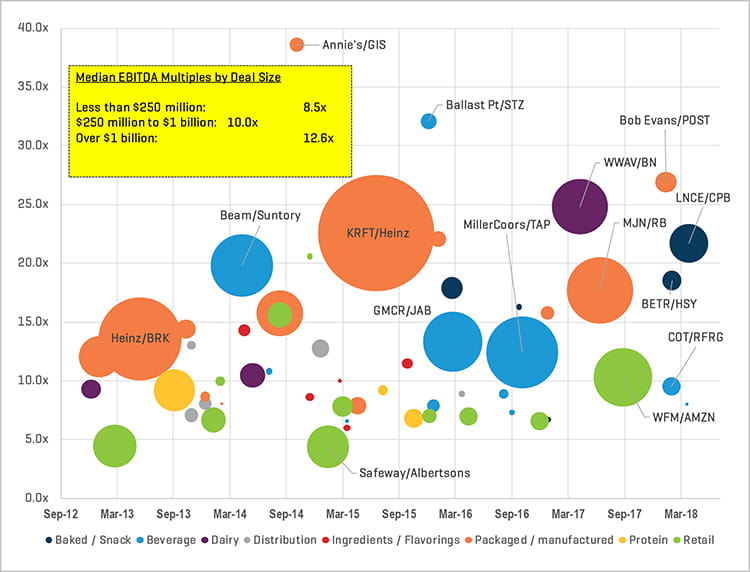

Overview of Recent Transactions; Valuation by Size

Across all sectors of the economy, we estimate that transaction valuations are two to four multiples of EBITDA higher than just a few years ago. Food and beverage is no exception. In fact, a linear regression of our proprietary data set indicates that such multiple expansion for food and beverage may be as high as 3.8x EBITDA. Valuations at these levels are unprecedented.

Larger deals still command size premiums, though even at the lower end of the market (i.e. transactions below $250 million) multiples have recently averaged 8.5x EBITDA.

Recent deals of note include:

- Snyder’s-Lance (LNCE) acquired by Campbell Soup (CPB) for $6.1 billion, or 21.7x EBITDA, in March 2018

- Bob Evans Farms acquired by Post for $1.7 billion, or 26.9x EBITDA, in January 2018

- Cott’s (COT) bottling activities acquired by Refresco (RFRG) for $1.3 billion, or 9.5x EBITDA, in January 2018

- Amplify (BETR) acquired by Hershey (HSY) for $1.5 billion, or 18.5x EBITDA, in January 2018

Select Transaction EBITDA Multiples

Public Pain of Retail, Large CPG

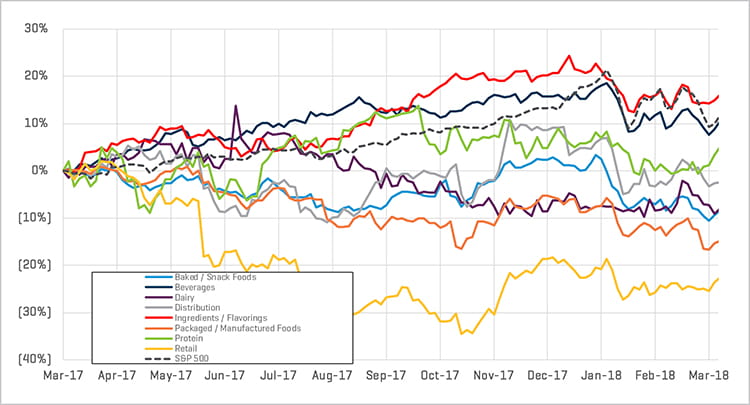

The past 12 months have been a mixed bag for large, publicly traded food and beverage company stock prices. All subsectors except for ingredients/flavorings underperformed the S&P 500 while two subsectors – retail and packaged/manufactured – are down 23% and 15%, respectively, YOY. Both retail and large consumer packaged goods companies that sell into grocery are clearly feeling the effects of the Amazon/Whole Foods transaction as well as expected growth from German deep discounters such as Aldi/Lidl. Neither Amazon/Whole Foods nor Aldi/Lidl are shy about swapping branded products for private label; indeed, private label can constitute up to 80% of the Aldi/Lidl SKU count. This obviously would hurt any branded product currently fighting for ever-shrinking shelf space in the center of the store.

Relative Share Price Performance

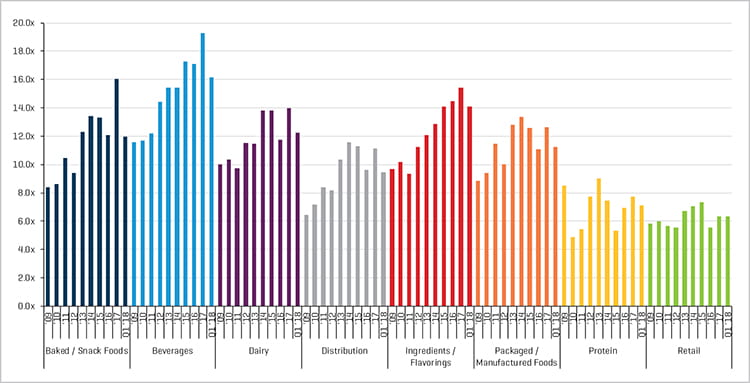

Every subsector except protein and retail are currently trading above 10x total enterprise value (TEV)/forward EBITDA, with beverages and ingredients/flavorings commanding the highest valuations in the public markets.

Forward EBITDA Multiples

Source for charts: S&P Capital IQ and Stout research.