The Tax Law’s Ripple Effect on M&A

The Tax Law’s Ripple Effect on M&A

The potential for increased business investment and economic prosperity is a positive sign for business owners and prospective buyers.

The Tax Cuts and Jobs Act (the “Act”),[1] which became law on December 22, 2017, represents a potential net positive for both prospective sellers and buyers of businesses. The ripple effect of the Act also could spur incremental deal activity.

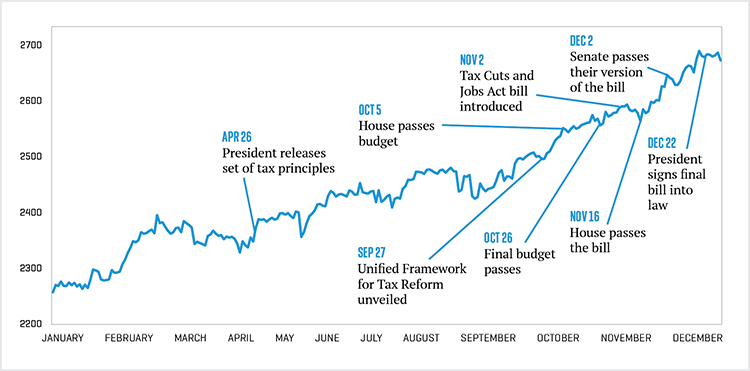

Overall, the decrease in the federal corporate income tax rate from 35% to 21% is generally expected to result in increased after-tax cash flows for companies that are performing well. All other factors being equal, higher future net cash flows for businesses could translate into higher theoretical valuations on a net present value basis, which is illustrated in the overall stock market increases after key events in the time preceding the passage of the Act (Figure 1). In addition to increased cash flows from lower taxes, there are other elements of the Act that could positively or negatively affect businesses and the overall merger and acquisition (M&A) environment.

Figure 1. S&P 500 Index Value (18.4% INCREASE FOR 2017, INCLUDING ANTICIPATION OF THE ACT)

Source: S&P Capital IQ

A Business Owner’s Perspective

As illustrated in Figure 1, the S&P 500 index rose 18.4% during 2017, with stock prices increasing in part due to higher expected company earnings in anticipation of the Act. Despite recent market volatility in early 2018, the general economic consensus is that the Act will have a favorable net impact on valuations.

In addition to lower taxes and higher cash flows, there are other elements of the Act that could indirectly impact business owners. For industrial businesses, increased cash flows combined with the Act’s changes in capital expenditure deductibility could result in more purchases of capital goods, such as machinery and trucks, which could benefit the manufacturers of such products. Industrial businesses could also raise wages or hire more employees in general. This, combined with lower personal tax rates from the Act, could result in higher personal discretionary income and an increase in the purchase of durable and other goods, such as automobiles and appliances, which could benefit the manufacturers of those products.

On the flip side, the Act could also lead to an increase in distressed situations and corporate divestitures. With interest deductibility limited to 30% of earnings before interest, taxes, depreciation, and amortization (EBITDA) through 2021 (and 30% of EBIT in 2022 and beyond), more companies may not be able to meet debt obligations, forcing owners to consider the sale of noncore assets or a potential bankruptcy filing.

Overall, the favorable business valuation implications of the Act, combined with an already robust M&A environment, could encourage owners to sell their businesses sooner rather than later. This includes many owners who were already near the tipping point of considering a sale prior to the Act. With a potentially significant number of incremental businesses being considered for market, M&A transaction activity could remain strong throughout 2018. At the same time, depending on the situation, higher cash flows and the potential for improved business performance could incentivize certain owners to continue holding their businesses in order to yield greater expected income.

A Buyer’s Perspective

Both strategic and financial buyers will have to weigh a number of factors as a result of the Act as they contemplate acquisitions going forward. First, potentially higher valuations in an already frothy M&A market could raise short-term hurdles for buyers who were already struggling to pay full valuations that have been prevalent in the marketplace. In addition, the Act’s change in interest deductibility could affect a buyer’s ability to finance a transaction in such a way as to meet value expectations while also meeting targeted return requirements.

The current M&A environment remains one of favorable financing, including excess capital and relatively low interest rates. Overall, the potential long-term benefit of a target’s incremental after-tax cash flow, as well as the aforementioned indirect benefits to businesses, could enable buyers to still generate a target return on investment. At the same time, there is potential for a differing view on valuation between buyer and seller expectations, especially if the tax benefits of a corporation structure are not realizable to a particular buyer.

Short- and Medium-Term View

For business owners/operators, higher cash flows are expected to drive increased investment into business operations, including in the form of increased capital spending and/or retention and attraction of human talent. Such investment is already beginning to occur at major corporations. For example, in January 2018, FedEx announced that it would commit more than $3.2 billion to wage increases, bonuses, pensions, and expanded capital investment in the U.S., including investing $1.5 billion to expand its hubs. Also, 3M recently announced that the company raised its outlook for 2018 in part due to the future direct savings that are expected from the new federal tax law. Such increased investment in capital and people has the potential to bolster a company’s valuation further from the impact of the previously mentioned lift in after-tax earnings and optimally position an owner for a favorable liquidity event during the next several years.

The Long-Term Ripple Effect

Regarding the long-term impact of the Act, all other factors being equal, businesses are expected to benefit from a broad ripple effect of greater economic prosperity, consumer confidence, and demand for products and services. As individuals and families begin to experience tax relief, consumer spending for products and services is expected to increase. Furthermore, as companies continue to invest in human capital and new jobs are created, an expected decrease in unemployment could lead to higher disposable income. Also, increased repatriation of capital from abroad has the potential to result in additional jobs across the U.S., including the opening of new industrial/manufacturing facilities as the ecosystem of product manufacturers and their suppliers begins to shift further inland.