Valuation Techniques for Bank Loan Portfolios

Valuation Techniques for Bank Loan Portfolios

Banks are well-served to invest in the development of enhanced loan valuation models to thrive in an increasingly competitive, technology-driven lending market.

A confluence of factors has led to increased focus on the measurement and analysis of bank loan portfolios. Commercial and consumer loans represent the largest asset on bank balance sheets, and the application of fair value accounting to bank loan assets has been a continuing trend in the industry. Several events and regulatory changes have highlighted the need for more robust loan level modeling for bank financial assets. Following the financial crisis, accounting standard setters and bank regulators have introduced changes to bank reporting that require fair value disclosures of financial instruments, including loans. While many commercial banks have not traditionally devoted considerable resources to fair value measurement for balance sheet loans, we propose that in today’s lending market, banks that invest in the infrastructure and resources to conduct a comprehensive valuation analysis will be at a competitive advantage.

Reporting Requirements for Bank Loan Valuations

Pursuant to Accounting Standards Update 2016-01,[1] banks must now disclose the values of their financial instruments under the “exit price” notion of value. This represents a shift from the “entry price” construct in the prior disclosure guidance that represented a peculiar and bank-specific standard of value. With this change, loan fair value disclosures are now consistent with the fair value definition promulgated in ASC 820.[2] Although loan fair value information remains relegated to the financial statement footnotes, and the research analyst community and bank auditors have not appeared to dwell on the change in methodology as a matter of enhanced scrutiny, we suggest that the application of enhanced techniques to the valuation of loan portfolios is an important step in the evolution of the financial services sector. The disclosure of fair value estimates, as well as accompanying descriptions of the underlying methods, assumptions, and models used to derive the values, allows for greater transparency for market participants, which in turn can lead to greater liquidity for bank loan assets. We also note that the industry has not faced a serious credit downturn since the initial requirement to provide financial instrument valuation disclosures was made effective in 2013, and we expect that these estimates of loan values would attract a high level of attention when the credit environment begins to deteriorate.

The call for enhanced transparency for bank asset values is related to other significant trends for financial institutions. In recent years, non-bank lenders, sometimes referred to as “shadow banks” or direct lenders, have engaged in lending activities that have traditionally been under the purview of commercial banks. Notable examples include business development companies, private equity and hedge funds, large family offices, and financial- and technology-focused loan originators. As shown below, these competitors for bank assets share a few common characteristics of note:

- Many entities operate as investment companies or via fund structures that report net asset value at fair value; these companies are typically not buy-and-hold operators, choosing instead to transact on loan pools with more frequency than traditional banks.

- Many technology-focused loan origination platforms have developed sophisticated systems and models for loan sourcing, underwriting, credit modeling. and managing risk.

In the context of mergers and acquisitions (“M&A”), fair value (as defined in ASC 820) is the required measurement method for recording loans acquired as part of a business combination. Commercial bank M&A activity remains on a strong pace with 120 deals announced resulting in $302 billion of assets sold in the first half of 2019.[3] In any bank acquisition, the valuation of the acquired loan portfolio is one of the most significant aspects of the M&A process, from the pre-deal due diligence of the loan files and data tapes to the post-transaction purchase accounting as per ASC 805.[4] Financial institutions that have invested in the infrastructure that facilitates a robust valuation process will be able to more effectively and profitably participate in M&A – by either leveraging financial tools to make acquisitions or by maintaining a loan reporting and analysis system that is accessible to third-party buyers. Conversely, financial institutions with outdated and incongruous loan accounting, credit modeling, and interest rate modeling systems will increasingly find M&A transactions to be cumbersome and expensive. In this manner, enhancing systems for loan valuation modeling facilitates whole bank acquisitions as well as other asset acquisitions or risk transfer transactions, such as whole loan sales or purchases and securitizations of balance sheet loans.

Finally, the models used for loan valuation are closely related to two other significant developments for commercial banks. The first, the current expected credit loss ("CECL") framework,[5] represents a significant change in the recognition of reserves for credit losses for loans and related financial instruments. The CECL standard represents a wholesale shift from an incurred loss or retrospective assessment of credit risks to an expected loss framework. The expected loss framework is, therefore, a prospective approach that requires an estimate of losses over the remaining life of the loan. As we will show in this article, a key component of loan valuation is the assessment of credit loss, as well as the decomposition of the loan coupon or stated interest rate into subcomponents to account for: the base market interest rate, expected loan credit losses, and the applicable loss-adjusted spread. The second pending market development for banks involves the transition from LIBOR-indexed loans to an alternative floating rate. According to a recent study, an estimated $5.2 trillion in outstanding commercial bank debt, and $10.3 trillion in mortgage loans were indexed to LIBOR at the end of 2016.[6] By investing in the infrastructure required for the detailed loan level cash flow models required for best-in-class loan valuations, banks will be able to leverage these tools and resources to prepare for the transition from LIBOR by modeling the financial impact of the proposed changes that are fundamental to the spread lending (net interest margin) business model of commercial banks.

In the remainder of this article, we demonstrate the mechanics of the valuation of consumer and commercial bank loan portfolios. Loan portfolios are almost always valued using a discounted cash flow model under the income approach. Our approach is founded on a few key tenets. The first involves leveraging enhanced datasets and flexible programming languages to model cash flows and calculate values at the individual loan level. This provides maximum flexibility to parse portfolio values at the most granular level and to generate customized reports for interested parties. Second, the approach is focused on the explicit modeling of each loan’s future cash flows to account for how the contractual payments are impacted by defaults and prepayments. Finally, our approach is consistent with the guidance in the fair value accounting standard that prescribes maximizing the use of observable market information. In this example, we focus on using market data to derive one significant credit model input that is often not directly observable: the loss-adjusted discount rate. Specifically, we employ benchmarking and calibration techniques that are used to value other illiquid financial instruments. For example, the AICPA’s recently issued valuation guide for private equity and venture capital[7] investments emphasizes the usefulness of calibration to determine the discount rate to be used in the valuation of non-traded debt instruments held by private equity funds and other alternative asset managers.

Sample Analysis – Applying Loan Valuation Techniques

Overview

In this section, we describe the general process and methodologies we employ to value portfolios of bank loans. Herein, we consider a stylized sample portfolio of performing consumer and commercial loans as context for presentation purposes. Consistent with the standard valuation method for debt instruments, we employ a form of an income approach. Specifically, we develop expected future cash flows on a loan-by-loan basis and discount the expected cash flows to present value at an appropriate risk-adjusted rate of return. The procedures performed in valuing bank asset portfolios generally follow these steps:

- Information gathering

- Asset data tapes

- Originator data

- Market data

- Development of asset level cash flow assumptions

- Development of expected cash flows

- Development of discount rate assumptions

- Presentation of conclusions

Information Gathering

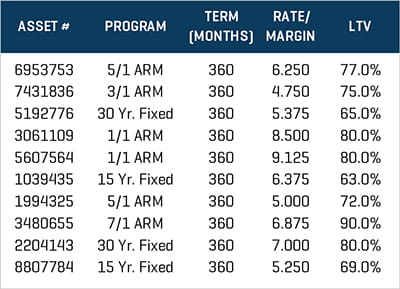

The first step in the process relates to assembling the information required for the analysis, as shown in Figure 1. We start with a data tape of the assets that presents fields such as contractual loan terms (origination date, fixed interest rate or spread, base rate, maturity, payment frequency, etc.) and borrower credit data (loan-to-value (LTV)), debt service coverage ratio (DSCR; defined as monthly income/monthly debt service), credit score (FICO), and the originator’s internal risk rating. Asset-by-asset credit data are particularly important, given that these variables allow us to make inferences about expected losses on a loan-by-loan basis, as discussed later in this section.

Figure 1. Loan Type Illustration

In addition to the loan tape data fields, we also examine the bank’s historical experience of loan prepayments, losses, and recovery rates. This data will be relevant as we develop asset level cash flow assumptions.

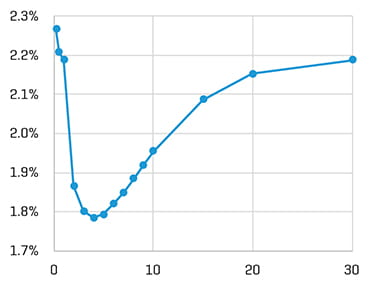

Finally, we obtain market data relevant to the analysis. This might include yield curves for base rates (U.S. Treasury yields and LIBOR rates, as shown in Figure 2), historical and expected prepayment rates on broader loan pools, and expected default rates by credit metric (LTV, FICO, and DSCR). Interest rate data will be relevant to analyzing contractual cash flows (if the instrument has a floating rate) and in assessing discount rates.

Figure 2. Base Rates by Maturity

Source: ICE LIBOR as of July 31, 2019

Asset Level Cash Flow Assumptions

In the next step in the process, we develop assumptions that will drive the cash flow projections for each of the assets in the portfolio. For these types of assets, we perform the income approach on a “loss-adjusted basis,” meaning we adjust the cash flows for expected losses, prepayments, and recoveries prior to discounting them to present value. The three key assumptions required are as follows.

- Prepayment Rates: We typically express prepayment rates as a constant prepayment rate (CPR) on a monthly basis, which represents the percentage of outstanding principal balance prepaid in each period. In a case where we vary CPR monthly based on seasonality and other factors, we would refer to this vector as a “CPR curve.” CPR curve assumptions can be extracted from multiple sources, including (i) historical originator experience (taken in the context of the historical interest rate environment) and (ii) historical market data, as previously presented. Importantly, we also incorporate market participants’ forward-looking expectations that capture the prevailing interest rate environment and seasonality, which is particularly relevant in the case of residential mortgage loans.

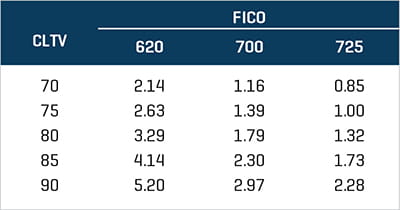

- Default Rates: Similar to above, we express default rates as a constant default rate (CDR), which is developed by examining the originator’s historical default experience, the credit metrics of each asset in the portfolio, and market data related to expected default rates by certain credit metrics. Refer to the sample data published by S&P in this regard, where default rates are a two-dimensional function of LTV and FICO score, as shown in Figure 3. The data points in this table represent factors, or multiples, to be applied to a given base case default rate (where a higher loan specific factor results in a higher expected default rate).

- Recovery Rates: Along with modeling default rates, we also model recovery rates, which represent the amount expected to be recovered by the bank on a loan in the event of a default (alternatively expressed as a rate of “loss given default”). As with the prior assumptions, these rates are a function of both originator and market data and the credit metrics of a given loan.

Figure 3. CLTV/FICO Adjustment Factors

Expected Cash Flows

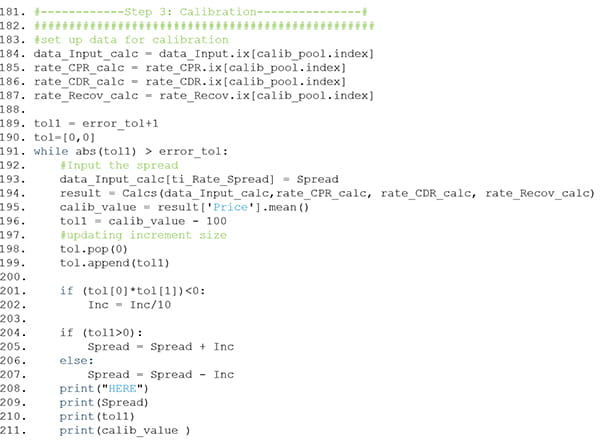

Next, we model future cash flows associated with each loan based on the contractual terms and the key assumptions described above. Our preference is to perform the analysis on an asset-by-asset basis as opposed to “bucketing” or consolidating cash flows for pools of loans. Our view is that these procedures lend additional accuracy to the analysis since prepayment rates, default rates, and present value factors are generally not linear functions of the variables used to derive them (e.g., default rates increase at a faster rate as credit profile deteriorates), such that a bucketing or pooling approach might distort the inputs and resulting cash flows. Commonly used tools, such as Excel, would likely not have the calculation power to efficiently perform the analysis for large portfolios, in which case we prefer to employ statistical computing languages (as exemplified in Figure 4), such as Python or R.

Figure 4. Sample Bank Model Code

Discount Rate Assumptions

Once we have the expected cash flows, we need to apply appropriate discount rates to each loan, which are typically expressed as a base rate (e.g., U.S. Treasury curve or swaps curve consistent with timing of payments) plus a credit spread. When determining credit spread, we have a couple of options: (i) look to the market for independent data related to appropriate pricing on comparable assets, or (ii) assume that the subject bank transacts at fair value and “extract” the appropriate credit spreads from contemporaneous loan originations or loan sales by the bank to third parties. Since market data can be difficult to appropriately compare and adjust to the specific assets originated by a bank, the second method, calibration to the subject bank’s observed transactions, is often preferred.

When employing method (ii), we undertake the following steps.

- Select a group of assets for which we have a known fair price (usually either a very recent origination assumed to be fairly priced at par, or a third-party sale price).

- Develop expected cash flows for each asset using the same process and inputs for all the other loans in the portfolio.

- Solve for the appropriate credit spread that results in a net present value equal to the observed price of the asset.

This technique is commonly referred to as a calibration process, where we are back-solving the net present value equation for the (recently originated or sold) comparable asset to derive the credit spread that produces the observed loan dollar price. Importantly, since the cash flows of all loans are already adjusted for credit risk and the risk of prepayment via the CDR/CPR assumptions, the resulting (adjusted) spreads from the calibration exercise can be fairly applied to all other assets. An additional factor, which we might need to incorporate into the model, relates to the term structure of credit risk for debt instruments. For instance, if the assets in the calibration pool have a different time to maturity relative to the subject assets we are repricing, then a term structure modification to the spread might be warranted. Once the applicable credit spread is determined for each loan, the final step is to calculate the price given the expected cash flows and derived discount rate.

Presentation of Results

While we perform these calculations for each asset separately in our programming code, the results are usually presented by aggregating loans into common pools (fixed versus floating, collateral type, origination program, etc.). Loan level detail including performance assumptions, cash flows and values are available as needed by the stakeholders. Figure 5 provides an example of this analysis.

Figure 5. Portfolio Summary

Embracing Advanced Loan Modeling for the Information Age

We have demonstrated an enhanced approach to bank loan portfolio valuation that is grounded in a level analysis driven by a flexible and scalable programming environment. We recommend that in this time of enhanced financial information, computing power and data analytics, leading financial institutions will be expected to deliver high-quality valuations of their loan portfolios. Banks are increasingly facing competition from non-bank lenders for assets and from technology firms and other fin-tech companies for deposit liabilities. Although the bank industry and its lobbying organizations have traditionally resisted calls for fair value accounting and related risk measures (CECL, model validation, and stress testing), we argue that embracing the data and modeling discipline required for a best-in-class fair value process will produce tangible competitive benefits. By developing a best-in-class framework for loan valuations (using internally developed models or by leveraging third-party specialists), leading banks will be well positioned to succeed in a dynamic transaction marketplace (whole bank M&A, bulk loan sales and purchases, securitization, and credit risk transfer) and to respond to expected external market and regulatory changes.

Stout Analyst Prasanthkumar Chunduru contributed to the development of this article.

- Financial Accounting Standards Board Accounting Standards Update No. 2016-01, Financial Instruments- Overall (Subtopic 825-10), Recognition and Measurement of Financial Assets and Financial Liabilities (Norwalk, CT: Financial Accounting Standards Board, approved January 2016).

- Standards Codification, Topic 820, Fair Value Measurements (Norwalk, CT: Financial Accounting Standards Board, approved January 2016).

- “Data Dispatch: U.S. bank Q2 M&A scorecard,” S&P Global Market Intelligence, July 30, 2019.

- Business Combinations (Topic 805) (Norwalk, CT: Financial Accounting Standards Board, approved January 2017).

- Financial Instruments – Credit Losses (Topic 326) (Norwalk, CT: Financial Accounting Standards Board, approved January 2016).

- Second Report of the Alternatives Reference Rates Committee (New York, NY, Alternative Reference Rates Committee, March 2018).

- Valuation of Portfolio Company Investments of Venture Capital and Private Equity Funds and Other Investment Companies (working paper, American Institute of Certified Public Accountants, Durham, NC, August 19, 2019).