M&A Market Update Looking for Potential Cracks in the Dam

M&A Market Update Looking for Potential Cracks in the Dam

The bull market has lasted for nearly a decade. How long can it go?

“No man ever steps in the same river twice, for it’s not the same river and he’s not the same man.” – Heraclitus, pre-Socratic Greek Philosopher

In June 2009, the United States officially exited the Great Recession, though most non-economists would be hard pressed to agree. The unemployment rate would not peak for another four months, the stock market would not return to pre-crisis levels for another four years, and consumer confidence would not fully rebound for another eight years.

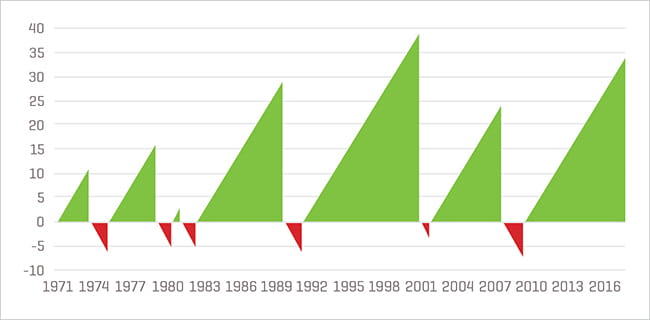

The length of the current economic cycle has been eclipsed only once in the past 50 years.

Figure 1. Count of Consecutive Quarters of Economic Expansion vs. Contraction, as Inferred by GDP

Source: Federal Reserve Bank of St. Louis

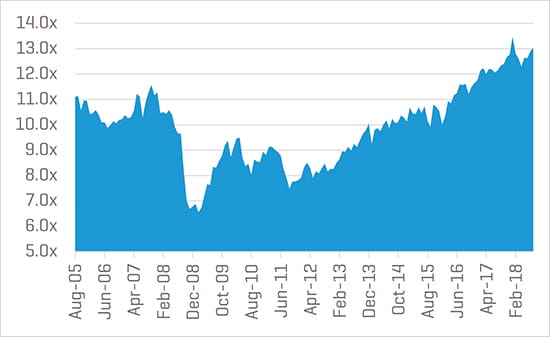

Meanwhile, the public markets, as measured by the ratio of total enterprise value to earnings before interest, taxes, depreciation, and amortization (EBITDA) remain at levels not seen in the past ten years.

Figure 2. Historical Total Enterprise Value to EBITDA for the S&P 500 Over the Past 10 Years

Source: S&P Capital IQ

How much longer can this market last?

The last recession was created, in large part, by too much leverage on both personal and corporate balance sheets. Personal balance sheets do not appear overleveraged, at least by one metric (Figure 3).

Figure 3. Household Debt Service Payments as a Percentage of Disposable Personal Income, 1980 to Present

Source: Federal Reserve Bank of St. Louis

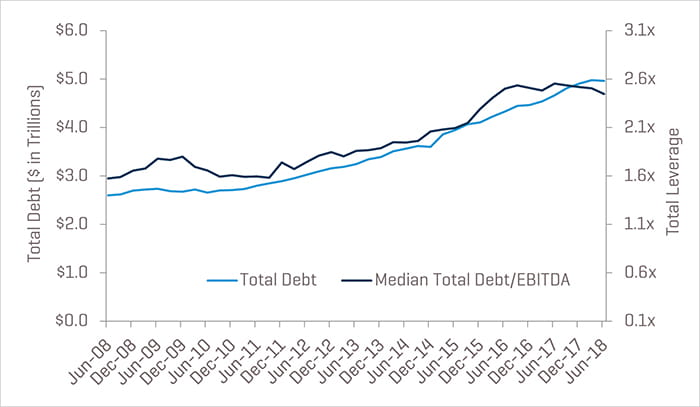

Corporate balance sheets are another matter. As we later show in Figure 11, debt and leverage (defined as debt/EBITDA) among U.S. companies are still near all-time highs relative to the previous five years. Furthermore, total leverage multiples for leveraged buyouts (LBOs) are at or above levels seen pre-recession (2005 through 2007).

Should we worry about the implications of the above for the economy, the M&A market, or business in general? It is difficult to say. Earnings remain strong, but for how long? Commodity prices are rising due to trade pressure, and the search for qualified labor has never been more difficult.

As the quote at the top of this article implies, we will never see another recession exactly like the Great Recession, if for no other reason than that we as a society have changed. Nevertheless, the recent spate of excessive leverage levels in large LBOs and covenant-lite loans might indicate otherwise.

However, one thing is clear – this is the best market to sell a company, as valuations have never been higher. Such windows of opportunity do not remain open forever.

Current State of the M&A Market

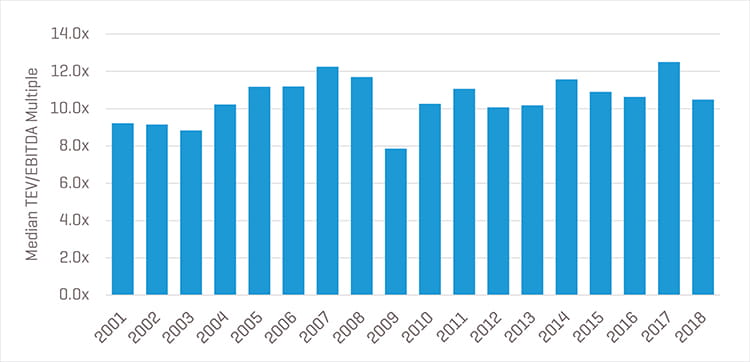

As can be clearly seen in later in Figure 7 and, subsequently in Figures 10 and 11, the overall reported transaction volume and value have decreased markedly year over year. However, the slowdown in overall M&A activity has not dampened valuations of how much buyers are willing to pay. EBITDA multiples remain near peak levels (Figure 4). Astute readers of our market updates know that we attribute such lofty valuations to a continued imbalance between the supply of high-quality acquisition opportunities and the number of potential buyers (both strategic and private equity) willing and able to deploy capital.

Figure 4. Median TEV/EBITDA Multiples, by Year, 2001 to Present

Source: S&P Capital IQ. Note: 2018 data through 7/31/2018

Such valuation premiums – relative to more typical market environments – are difficult to quantify, though they appear to average (based on our proprietary analysis of nonpublic information of multiples paid) in the 2.0x to 3.0x range. Furthermore, just as remarkable (and even more difficult to quantify) is the widespread sentiment among dealmakers that even the most storied or difficult and cyclical companies are generating interest in the current environment.

Unemployment continues its steady downward trajectory, consumer confidence continues its upward trajectory, and U.S. gross domestic product (GDP) continues to exhibit signs of longer-term stability.

Our View of the Future

The view looking forward is, as always, murky at best.

Recently enacted corporate tax reform has resulted in increased free cash flow for most companies. This increased cash flow, combined with the 100% bonus depreciation, continues to benefit a wide range of industries, including any capital equipment manufacturer or distributor.

Prices for “politically charged” commodities such as aluminum and steel have spiked (though prices for others, such as copper, corn, and soybeans, are much tamer). We do not know how much longer such pricing dislocations will last, nor if they will worsen before improving.

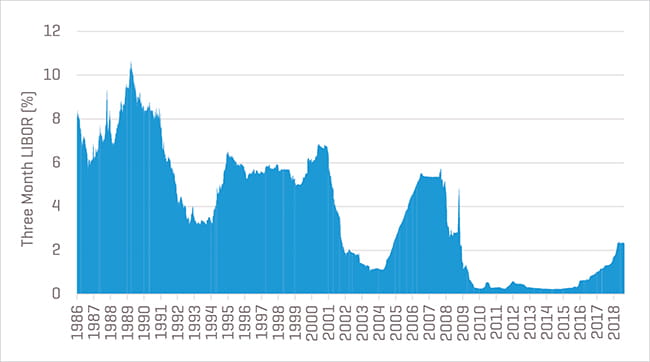

The debt markets remain open, and we cannot fathom a scenario in the next few years in which lending guidelines, capital requirements, and regulatory oversight increase under President Trump, though interest rates are a different story. If the recent run-up in the London Interbank Offered Rate (LIBOR) is any indication, interest rates (and inflation) are headed in only one direction – up – as rates begin rising from their record lows (Figure 5).

Figure 5. Three-Month U.S. Dollar LIBOR, 1996 to Present

Source: Federal Reserve Bank of St. Louis

Fortunately, as discussed in prior articles, LBO returns are far more sensitive to decreases in debt availability than to increases in borrowing costs.

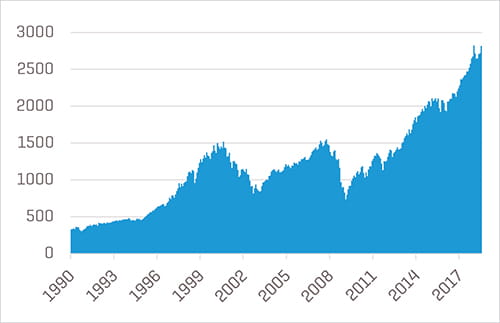

As discussed above, the public equity markets remain near an all-time high in spite of volatility seen in early February (Figure 6), but we do not know when another correction will occur, and if such a correction will negatively influence M&A multiples.

Figure 6. Historical Price Performance of the S&P 500, January 1990 to Present

Source: S&P Capital IQ. Note: 2018 data through 7/31/2018

We do not know if a major external shock to the system (geopolitical or otherwise) is on the horizon nor how the U.S. economy would react to such an event.

Finally, we do not know how buyers will react in the face of continued pressure on top-line growth prospects. Will such buyers take a long-term view, or will they (as has typically been the case) begin to lower bid prices to better align with long-term average multiples?

In summary, as we pause to reflect upon where we are in the cycle, we see that the fundamental forces driving M&A activity and valuation multiples are no longer as perfectly aligned as they once were. This is not to say that a major pullback in prices is imminent; though we no longer expect continued multiple expansion, we do view multiple normalization as an ever-increasing possibility.

M&A Market Activity

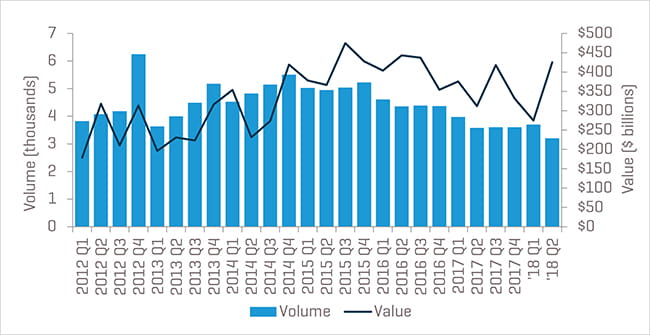

Improved availability of capital, better and sustained company performance, and narrower valuation gaps have powered U.S. M&A transaction activity since 2010. The past 12 months continue a slow but consistent downward trend, though the overall value has been a bit more volatile. Such volatility has been driven by front-page grabbing, multi-billion dollar deals such as AT&T’s $107 billion takeover of Time Warner and Bayer’s $65 billion acquisition of Monsanto (Figure 7).

Figure 7. Total U.S. M&A Deal Volume and Value by Quarter

Source: S&P Capital IQ

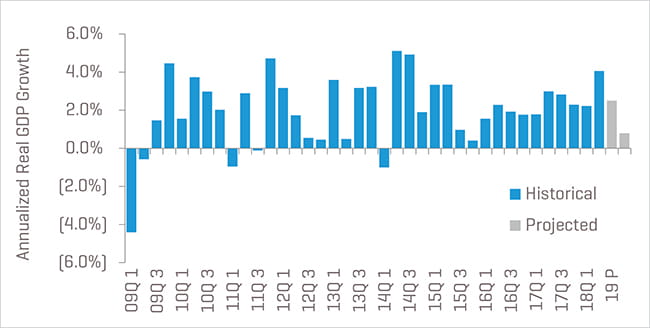

The U.S. GDP, often viewed as a proxy for the overall health of the economy, has recovered from the contraction experienced during the recession in late 2008 and early 2009. Few economists are predicting another recession in the near future; tax reform ensured at least 12 months of continued expansion (Figure 8).

Figure 8. Change in U.S. GDP, 2009 to Present

Source: U.S. Bureau of Economic Analysis, EIU

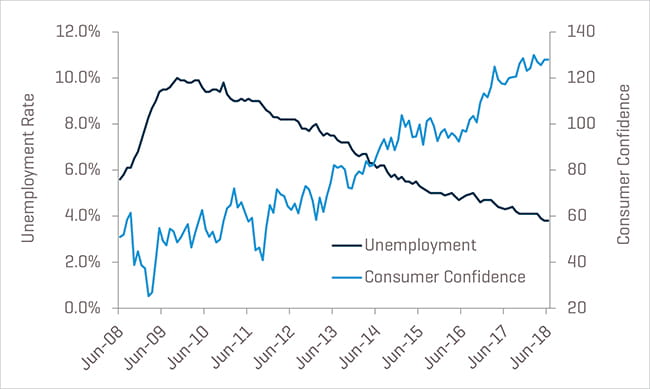

Consumer confidence generally improves as the unemployment situation improves. Fortunately, unemployment has maintained its steady march downward and sits at levels not seen since mid-2000 (Figure 9). Such favorable tailwinds are expected to continue throughout 2018, though there are signs that the tightening of the labor force is finally beginning to exert upward pressure on inflation.

Figure 9. Unemployment and Consumer Confidence

Source: U.S. Bureau of Economic Analysis, University of Michigan Consumer Confidence Report

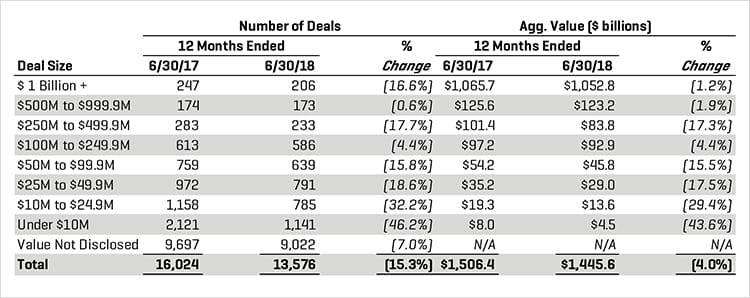

As mentioned in previous articles, data on lower middle market transactions are notoriously difficult to come by, but year-over-year comparisons can prove illustrative. Deals falling within the lower middle market (in this context defined as transactions less than $250 million in total value) were subdued relative to the prior 12-month period, as both volume and value were down, reflecting overall trends in M&A markets. A similar pattern emerged for larger deals, which also decreased in both number and value; this pattern was noticeable despite the fact the average size increased due to the aforementioned mega-deals (there were five transactions, each with a total value over $10 billion, completed during the second quarter of 2018, alone).

Figure 10. Recent U.S. M&A Activity by Deal Size

Source: S&P Capital IQ

Strategic buyers were active in the first half of 2018, though less so than in the recent past.

The continued (albeit softer) stimulus for strategically led deals is a combination of lower organic growth prospects absent acquisitions, accommodative senior debt markets (for most of the past 12 months), and a record amount of cash and other liquid assets held by nonfinancial companies. Evidence of the accommodative debt markets is clearly visible in the continued rise in total debt levels. Both the median total debt/EBITDA and the total debt levels remain elevated (Figure 11).

Figure 11. Debt Holdings and Leverage Levels of Strategic Buyers

Source: S&P Capital IQ

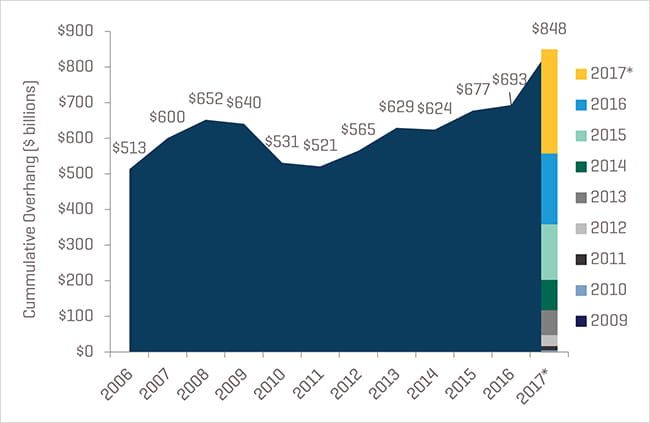

Complementing (from a seller’s perspective) strategic buyer interest is private equity, which remains a potent force in deal flow. Favorable credit markets and a record $848 billion capital overhang will continue to provide an impetus for investors to stay competitive in transactions (Figure 12). Furthermore, it should be kept in mind that the capital overhang actually translates into nearly $2 trillion in purchasing power, given the leverage available in today’s marketplace.

Figure 12. U.S. Private Equity Capital Overhang by Vintage Year and Fund, 2006 to Present

Source: PitchBook. *As of 3/31/2018

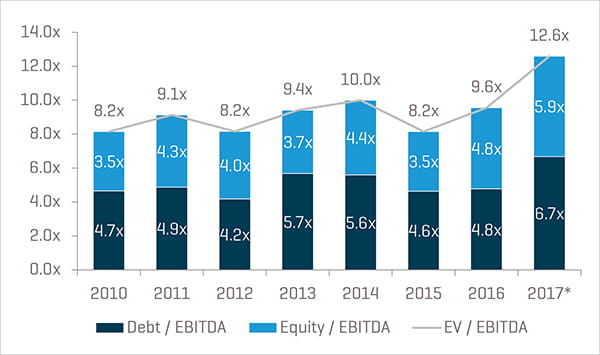

Nowhere is the increase in current valuation multiples due to the aforementioned factors more evident than in the prices paid by private equity during the past five years. Such prices are a function of debt providers’ willingness to lend and sponsors’ willingness, for the first time in history, to lower their required return thresholds. Historically, financial sponsors promised their limited partners an expected compounded annual return of 20% to 30%; however, recent feedback from many in the private equity community (all of whom wish to remain nameless) is that returns are now being modeled in the high teens. Such a reduction in required returns has the same effect as a reduction in yields on bonds – when rates fall, the prices that buyers pay for new investments rise. The continued increase in multiples for 2017 (among the highest in recent memory) is a direct result of a decrease in quality targets available to be acquired (Figures 13 and 14).

We do not expect a material negative impact from the new limitation on the deductibility of interest payment to 30% of EBITDA; for all but the most highly leveraged companies, this limitation will not apply. Even in those cases where it does, the net impact on after-tax free cash flow will not be very meaningful.

Figure 13. Median EBITDA Multiples for Leveraged Buyouts, 2010 to Present

Source: PitchBook. *Through 12/31/17

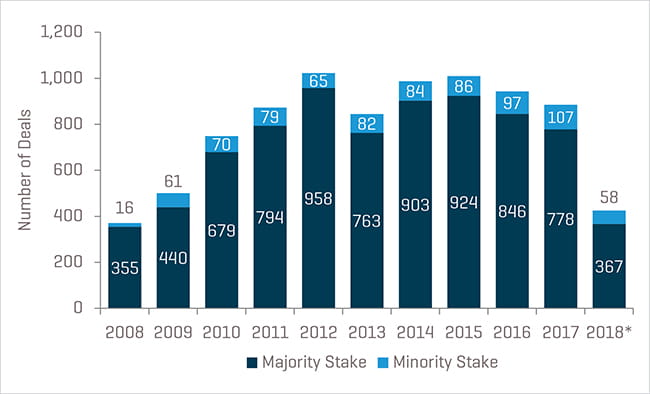

Figure 14. U.S. LBO Volume, 2008 to Present

Source: PitchBook. *Through 6/30/2018

Outlook for the Remainder of 2018 and Beyond

Our view for the foreseeable future remains cautiously optimistic. Buyer appetites and resulting valuation multiples are still at or near historical levels. How long this will last is anyone’s guess; that being said, for those business owners who are on the fence about selling their companies, it may be prudent to accelerate such decisions rather than waiting to see what the road ahead has in store.

Related Professionals

Related Insights

-

Article

Getting the Letter of Intent Right

-

Industry Update

Metals Industry Update - 1H 2018

-

Industry Update

Behavioral Health Industry Update - September 2018

-

Industry Update

Tire Distribution & Manufacturing Industry Update Q2 2018

-

Industry Update

Industrial Services Industry Update - Q2 2018

-

Industry Update

Healthcare & Life Sciences Industry Update - Q2 2018