How to Calculate the Balance Sheet Impact of ASC 842 Adoption

How to Calculate the Balance Sheet Impact of ASC 842 Adoption

As discussed in the first article of this series, the adoption of ASC 842 results in the recognition of both a lease liability and a right-of-use (ROU ) asset. The initial and subsequent calculations of lease liability and ROU asset values are discussed below.

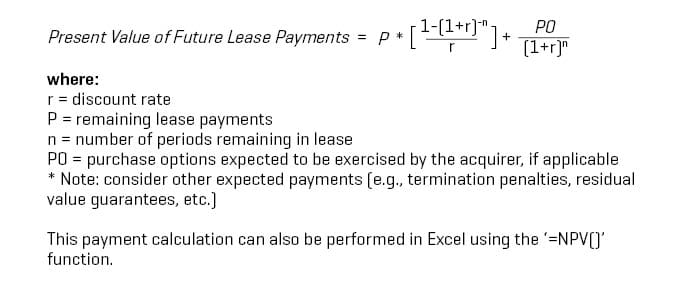

Lease Liability

The lease liability is calculated by taking the present value of the remaining lease payments over the remaining lease term. The discount rate used to calculate the lease liability is either the rate implicit in the lease, or the company's incremental borrowing rate (IBR), which is the rate the company would pay to borrow funds equal to the rent payments over the same term as the lease . Because the implicit rate considers lessor costs that are typically not disclosed or visible to the lessee, the IBR is more commonly used. Private companies may also elect to use the risk-free rate to discount remaining lease payments; however, the use of the risk-free rate rather than the IBR results in higher lease liability and ROU asset values and an increased risk of future impairment, which will be discussed in the next article in this series.

Additionally, the lease term includes any renewal options (or termination options) that the company is reasonably certain it would exercise as of the lease inception date. When evaluating renewal options, the company should consider whether the agreed-upon lease payments are above or below the market, as well as future operational needs. Similarly, a purchase option the company is reasonably certain (again, as of the lease inception date) that it will exercise should also be included in the lease liability calculation. The company's evaluation of purchase options should consider the price relative to the market, potential expense(s) incurred if the option is not exercised, and future operational plans when determining whether it is reasonably certain that a purchase option will be exercised.

Below is the lease liability formula:

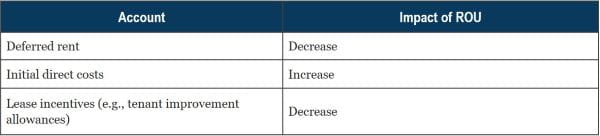

ROU Asset

The ROU asset is equal to the lease liability computed above and is adjusted for the following:

As of the initial adoption, the ROU asset generally equals the lease liability, except in situations where rent has been prepaid.

Adoption Exception: Finance Lease

One notable exception to the calculations outlined above is that finance leases (formerly called capital leases) carry over at pre-adoption values. This exception is applicable only at adoption. After adoption, the lease liability and ROU asset calculations for any new finance leases should follow the formula outlined above.